When we make decisions, we would all like to think that we are more like Mr Spock from Star Trek (who uses relentless, emotionless logic) than Homer from The Simpsons (who doesn’t). Unfortunately, it is sad, but true, that the opposite is usually correct. Multiple studies have demonstrated that investors’ decision-making is dominated by their emotions and these emotions are usually counterproductive from the point of view of their investment returns.

These studies all clearly show that there is a “behaviour tax” across the world that makes investors’ experiences of their investments far worse (from a returns perspective) than they could have been if they had simply sat on their hands. A recent study¹ of the South African experience confirmed these results over the period 2006 – 2018.

To help understand what behaviour lies behind this self-destructive behaviour and thus what we can do to help ourselves (and our clients), a study of 44 815 switches conducted by 23 390 clients on the Momentum Wealth Linked Investment Services Platform (LISP) was recently conducted for the period January 2006 – December 2017.

The theoretical basis for this study started with Cumulative Prospect Theory (CPT) – the theory of decision-making under risk that Nobel Laureate Daniel Kahneman developed with Amos Tversky². CPT highlights firstly, the importance of a reference point for individuals when they make decisions – they hate losses more than they like gains; and secondly, decision-makers’ inability to correctly assess probabilities – they overweight extreme outcomes.

Sitkin and Pablo³ extend this work by proposing that while investors each have a “risk preference” or character trait of being attracted or repelled by risk, this preference is mediated by our “risk perceptions” or assessment of risk in any given situation and our “risk propensity” to take risk, which is a function of recent experience in this space.

In short, humans are particularly poor at assessing risks and can easily be fooled by something as simple as the way a given situation is framed. Investors typically underestimate risk when experiencing losses and often look for excess risk at the opportunity of negating such painful losses. Moreover, our propensity to assume risk is significantly affected by prior outcomes (recent successes or failures).

Humans are particularly poor at assessing risks and can easily be fooled by something as simple as the way a given situation is framed.

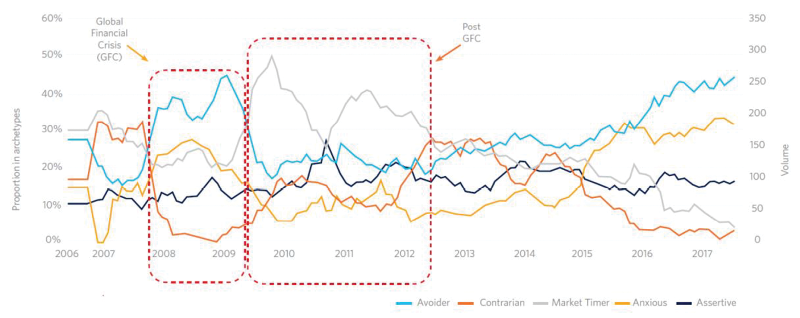

These insights guided our choice of the explanatory variable for what is a first for South Africa: a segmentation of South African investors based on a risk-based analysis of the switching of their holdings in discretionary unit trusts. Switches were grouped based on the relative historical performance of the funds being switched out of and those being switched into; the relative risk profiles of these funds and finally, the average number of switches and their frequency.

The use of the Hierarchical Clustering technique showed that there are five clearly defined groups (or archetypes) of switching behaviour inside this large sample of investors:

1) Risk Avoiders. These switches are made by investors who tend to have a low-risk appetite and rather avoid risk altogether. They therefore stick to a more conservative asset allocation and do not switch often. Keeping with avoiding risk and avoiding change, they are likely to remain in funds with similar (low) risk. They are relatively likely to chase past performance when current performance is below inflection. This behaviour seems to be more common in older investors and slightly more common with females compared to other archetypes.

2) Contrarians. As the name suggests, these switches are made by investors who are seemingly showing the opposite behaviour than that of the other archetypes. They have a seemingly high risk preference and a high tolerance for downside risk. Whether performance is high or low, these investors rarely chase past performance: they are more likely to switch to funds with worse past performance. Keeping with the title of this archetype, this was the only cluster which realised a positive behaviour tax.

3) Market Timers. The main driver here is switch frequency since market timers constantly move between funds in an attempt to beat the market and maximise returns. These investors show a mix of fear and greed driving switches. We see that such behaviour leads to high behaviour tax during periods of crisis and periods of fluctuating markets.

4) Anxious. Investors with this type of switching behaviour seem to have a low risk appetite; however, they do not avoid risk altogether. These investors are very sensitive to downside risk and are likely to act out of fear when underperformance looms. They are very likely to down-risk and chase past performance when current funds are performing below inflection. Such behaviour led to high behaviour tax, especially during periods of growth where they would be “missing out” on performance.

5) Assertives. Investors with this type of switching behaviour are more risk-tolerant and set on chasing past performance. When chasing past performance, it is mostly between funds with similar risk profiles. We expect these investors to be overconfident and to follow their ways and not be influenced as much by advisors.

The distribution of the occurrence of these switches through time is presented in the graph (above). As expected, the “Anxious” and “Risk Avoiders” switches dominate in times of crisis and poor market returns. The “Market Timer” switches peak after the crisis period.

Why is this segmentation important?

A better understanding of the compromising nature of myopic risk behaviour (which places too much emphasis on the transient present and its related emotions) is key to understanding your behaviour, and, if you’re an advisor, your clients’ behaviour. More importantly, it can provide a proper basis for intervening at the right time to avoid the associated negative implications of these behaviours.

Ultimately, the point is to help all investors avoid the harmful outcomes of them “being Homer”. These empirical insights are key to achieving this outcome.

* This article is a summary of a white paper: “Understanding the great forces that rule the world. A study on South African investor behaviour” written by Paul Nixon, Evan Gilbert and Dirk Louw of Momentum Investments in October 2020.

1 – Nixon, P.P., Barnard, M., Bornman, R., and Louw, D.J.D. 2019. The South African investor behaviour tax and helping investors count what counts. Momentum Investments.

2 – See Kahneman and Tversky, 1979, and Tversky and Kahneman, 1992.

3 – Sitkin, S.B. and Pablo, A.L. 1992. Reconceptualizing the determinants of risk behavior. Academy Of Management Review, 17(1), pp.9-38.