The growth of DFMs in South Africa over the past 10 years has led to the evolution of a range of DFMs from boutique to larger DFMs with assets well in excess of R50-billion. This growth means DFMs are now able to direct the flow of significant assets to and from asset managers, and have an increased influence on investment mandates and, very importantly, pricing.

Before the emergence of DFMs, most financial planners were effectively “fund pickers”, either choosing single or multi-managed funds for their clients and putting portfolios of these funds together in ways that they deemed appropriate for clients. There are still financial planners who operate based on this model, which has benefits. Firstly, the financial planner can justify their value to clients by saying that one of their roles is “investment expert” which justifies an ongoing asset-based fee for advice. Secondly, the financial planner can argue that they are able to provide genuine bespoke advice to clients using this approach.

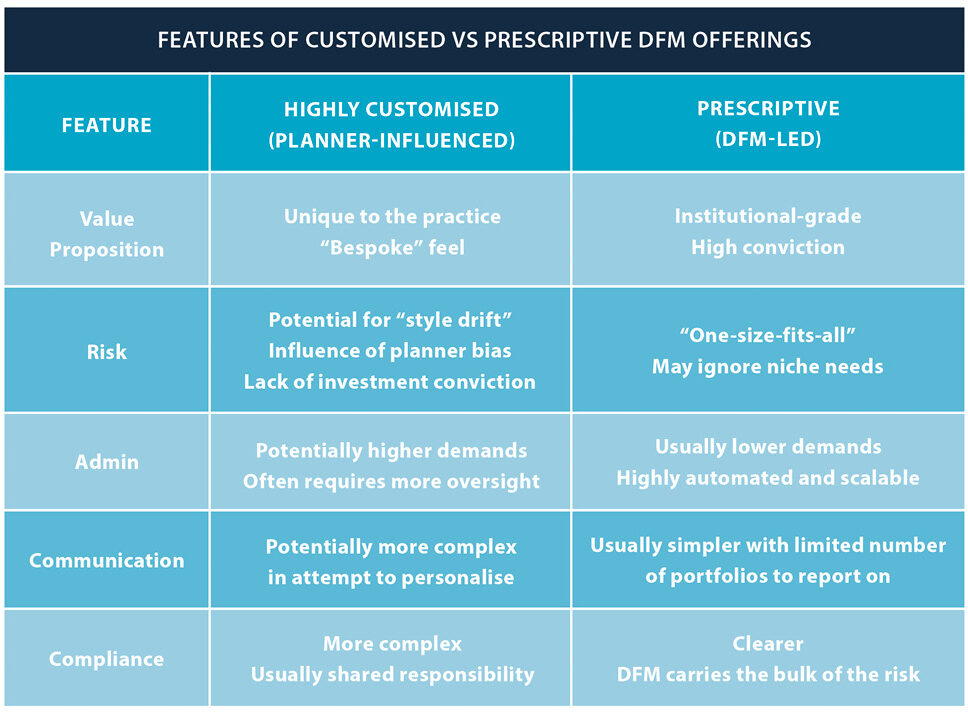

The emergence of DFMs presents financial planners with a challenge: how do they retain a unique value proposition while also wanting to enjoy the benefits of scale that DFMs offer?

Financial planners own the individual client and effectively act as a “distribution channel” for DFMs. Yet if financial planners compromise both their independence and value proposition in the process of using a DFM, it’s a case of the tail wagging the dog. The client comes to the financial planner for advice and solutions, not the DFM. This begs the question, how flexible and customisable should a DFM offering be? This question talks to the power dynamic between DFMs and financial planners. Who’s the boss? In considering this dilemma, we consider three key questions which help us look at whether or not the tail should be wagging the dog.

A. Should financial planners be able to influence the DFM investment offer?

Most DFMs will position themselves as partners of financial planners, offering a service that was historically internal to a financial planning business. In a sense it’s no different to a business outsourcing their payroll, accounting or technology functions. The question is, should a DFM service be regarded as an outsourced function where the financial planner is a passive consumer of a DFM’s products, or one in which the financial planner and DFM co-build and share the responsibility of the model portfolios that are developed?

The reality is that both models exist. Some DFMs see themselves as investment managers who are given a mandate by the financial planner and their clients to deliver agreed-upon investment outcomes. The financial planner in this model has no influence over the decision-making in the model portfolios and relies totally on the DFM’s investment expertise to make the appropriate fund choices and asset allocation decisions. The financial planner is kept in the loop on any changes that are made in the portfolios, but they have no influence over the decisions. “Take it or leave it” might be a way to describe this approach.

At the other end of the spectrum is the “Joint Investment Committee” (JIC) model, which involves the DFM and the financial planner forming an investment committee made up of members from both the DFM and the financial planning business. At the initial stage of the relationship, this committee agrees on the range of model portfolios that will be offered to the financial planner’s clients and the financial planner will be involved in the decisions around funds to be included in the portfolios as well as the asset allocation for each portfolio.

Once the portfolios are up and running, changes to the portfolios are made through joint decision-making, whether this be asset allocation or fund changes. Ultimate responsibility for the decisions depends on the licence status of the financial planning business. A Cat I financial planning business has to defer to the final decision being made by the DFM, no matter how much input they have given.

If the financial planner has a Cat II licence, then the DFM cannot make decisions autonomously and requires that the financial planning business has an appropriate level of investment expertise internally not only to be able to participate in the process effectively, but also take responsibility for any decisions that are made. Whichever model a financial planning business opts for, there are certain non-negotiables to be aware of:

- The financial planning business has a clear investment philosophy which its clients have bought into and the investment process, whether completely outsourced or co-created and co-managed, aligns with this philosophy.

- In the JIC model, where a financial planner with a Cat I licence may have influence over the investment decision-making, the key benefit of having a DFM remains that the DFM (under its Category II licence) must retain final discretion. This ensures that one of the key benefits of having a DFM is enacted, namely: enabling decisions to be implemented across all client portfolios at the same time without having to consult clients. It also means that the DFM protects the planner from the legal consequences of “failed” investment decisions.

- Whatever route a financial planner decides to go, it should be rooted in their clients’ needs – not a desire to “play fund manager”. In the same way that it may be better for a client that a financial planner gets a lawyer to draw up the client’s will, so too, the approach adopted in working with a DFM should be made bearing in mind what is better for the client.

- Whether or not the financial planner has influence over the DFM’s investment offer, that offer needs to align with the needs of the client.

- The approach a financial planner takes must align with their value proposition to clients. Are they clear whether they want to sit on the client’s side of the table or the DFM’s side? Or do they feel that they can do both?

B. Is it better for DFMs to be prescriptive and steadfast in their investment offer?

Before using a DFM, most financial planners were making investment decisions for their clients. So it is understandable that many would want to continue to have some involvement in the investment process. Yet there is an argument that the more prescriptive and steadfast a DFM is in their investment offer, the better. By being “steadfast” and “prescriptive”, a DFM ensures that there is not only a consistency of process, but a consistency of outcome. This aligns with TCF (Treating Customers Fairly) by ensuring that all clients with similar investment mandates receive the same experience and performance. This ensures that there is reduced performance dispersion within a financial planner’s client base.

Some financial planners will argue against being prescribed to by a DFM, suggesting that this impacts their ability to “personalise” their investment offer to clients. But this does raise the dilemma of what is most important for clients, what is most aligned with TCF, consistency of outcome or personalisation? The reality of investing is that there are limited outcomes that model portfolios can achieve consistently and sustainably over time.

It is possible that DFMs can meet personalisation needs for clients through prescriptive offerings. For example, all clients who are drawing down income in retirement could have a portfolio set up for this purpose. But whatever the level of income being drawn, it is likely that only one portfolio is needed to meet this need. Similarly, clients who are wanting a high-growth, high-equity portfolio likely only need one portfolio. If one considers that the highest returning local asset class (South African equities) has delivered a return of inflation plus 7% over the long term, it means that a model portfolio that is in any way diversified beyond SA equities is likely to deliver a lower return over the long term.

This suggests that “personalisation” ultimately is only going to make a difference to the inputs of the model portfolio, fund choices and asset allocation, rather than to the outcomes. The benefits of a DFM being prescriptive and steadfast in their offer include:

- Enhanced scalability of the DFM’s model portfolios as all client assets are invested into a limited set of portfolios. This boosts the DFM’s ability to negotiate and influence the asset managers they use in their portfolios. It also simplifies the DFM’s communication with the financial planner and their clients. The benefit to the financial planner is that they are not distracted by trying to communicate and manage across too many “personalised” client portfolios. Arguably, a prescriptive DFM model allows the planner to focus on where they really add value, namely in their engagements with clients, rather than on investment decision-making and at times investment administration. The greater the variety of model portfolios, the greater the personalisation of client solutions, the greater the likelihood of an increased administrative burden.

- There is a risk that a DFM that is too flexible in their offering can lose its conviction about their “house view” and possibly be not clear on what their investment “conviction” really is. A key benefit a DFM can offer a financial planner is having conviction, with a clear investment philosophy and process that they stick to. There is a risk that too much personalisation hampers their ability to do this.

- Consideration of whether being steadfast and prescriptive really does hamper the ability to offer personalised portfolios. Some DFMs will argue they do both and the reality is that with the integration of technology into the investment process it is possible to do both. There are DFMs who are able to offer bespoke portfolios for each financial planning business without compromising their philosophy and approach, and they do this primarily through the effective use of technology.

C. How realistic is it for South African DFMs to offer both offshore and local solutions?

One consideration for financial planning businesses is whether they use one or more DFM. In order to get the benefits of scale and efficiency it would make most sense to only work with one DFM. But in the South African context, the dilemma of how to handle offshore exposure and solutions arises. To gain the benefits of diversification, there is unlikely to be much debate about the importance of offshore exposure in client portfolios. But there is complexity to this.

In retirement funds, Regulation 28 constrains the extent of offshore exposure, while with discretionary funds there is the potential for full exposure, whether invested directly offshore or in rand-based feeder funds. A local DFM can integrate a rand-based feeder fund into a “local” model portfolio, but if investing money directly offshore then the need arises for currency conversion into offshore model portfolios that are domiciled in another jurisdiction. Apart from the administrative complexity that this introduces, it begs the question, can a local DFM effectively manage an offshore domiciled model portfolio?

A DFM would argue that this depends on the nature of the portfolio. An equity-only offshore model portfolio made up of index funds is likely to be easier to manage from South Africa than a balanced model portfolio in which active managers are appointed across different asset classes. DFMs that are part of larger institutions often have an association or partnership with a global research capability which takes all global investment decisions, which also feed into the offshore exposure within a local model portfolio. There are some independent DFMs with a presence offshore, in which case their international team is likely to make the global decisions on behalf of the local team.

For local-only DFMs, the question financial planners must ask is, do they have the capability to manage an offshore model, or the offshore exposure in a local model, from South Africa? This question is not only relevant at the level of fund selection, but also asset allocation. Given the complexity involved in looking after client assets in a global context, financial planners whose DFM does not have an offshore presence or partner, may need to consider using different DFMs for local and offshore assets. This decision would need to be balanced against the scale, operational and efficiency benefits of using a single DFM.