Structured products combine traditional assets, typically a bond or deposit, with derivatives such as options and swaps. This combination is designed to create payoffs that can preserve capital, enhance yield or tailor risk according to investor outlook.

In South Africa, the market has matured rapidly since the early 2000s, supported by strong local banks, an active stock exchange (JSE) futures complex and a conduct-focused regulator, the Financial Sector Conduct Authority (FSCA).

Why index selection matters

“If you don’t know what’s inside the index, you don’t know the real bet you’re making.” – Howard Marks.

In structured products, the underlying index determines the payoff potential. Choosing the right index can lead to better alignment with an investor’s risk-return objectives.

In South Africa, many structured products reference the JSE or hybrid indices that include international equities or commodities. FSCA guidelines require issuers to explain how they choose or design these indices, promoting transparency.

Criteria for selecting indices

- Market relevance. An assessment of whether the index represents a sufficiently liquid market to ensure accurate pricing and minimal tracking error.

- Investor familiarity. Clients often prefer well-known benchmarks like the S&P 500 and Euro Stoxx for reference purposes.

- Risk profile and volatility. Indices with historically high volatility may require more expensive option structures. Certain structured products prefer volatility-controlled indices for stable, predictable pricing.

- Dividend or financing considerations. In cases of uncertain or variable dividend policies, decrement or excess return indices can help standardise outcomes. If the product aims to reflect net returns above a benchmark rate, an excess return methodology might be preferred.

- Regulatory and methodological transparency. Considerations include index governance and whether the index provider publishes rules and methodologies. For cross-border offerings, the consideration is whether the index meets the EU benchmark or local FSCA disclosure standards.

- Product design goals: capital protection vs growth. A capital-protected product might opt for a lower-volatile index or a decrement approach. If the aim is to achieve higher coupons through yield enhancement, issuers might opt for excess return or sector-focused indices with higher upside potential.

Performance asset composition analysis ?

Equity selection involves considering sector exposure, such as financial, resource and consumer goods sectors, which can drastically alter risk and return. Geographic spread is another critical factor, with choices between purely local indices, such as the JSE and global baskets.

Weighting methodologies also play a significant role. Market-cap weighting assigns a larger slice to larger companies, equal weighting gives each company the same weight to reduce concentration risk, and factor- or thematic-based weighting tilts towards specific criteria, such as “value”, “momentum” or themes like green energy, for example.

Dividend policy is another consideration, where the impact of price return versus total return or any decrement mechanism on the expected yield must be evaluated.

Protection asset composition analysis ?

Bond or deposit selection

Credit quality is of paramount importance, with government bonds or top-tier local banks typically providing capital protection. The duration of the bond or deposit should align with the term of the structured product to ensure the principal remains secure. The creditworthiness of the issuer is essential; even for “protection” assets, there is a risk of default if the issuer is not financially stable.

In South Africa, advisors meticulously review the bank’s credit rating and track record to assess its reliability. There is frequently a cost-protection trade-off; allocating more capital to risk-free or lower-risk assets leaves less available for the option or derivative portion, which can limit potential upside.

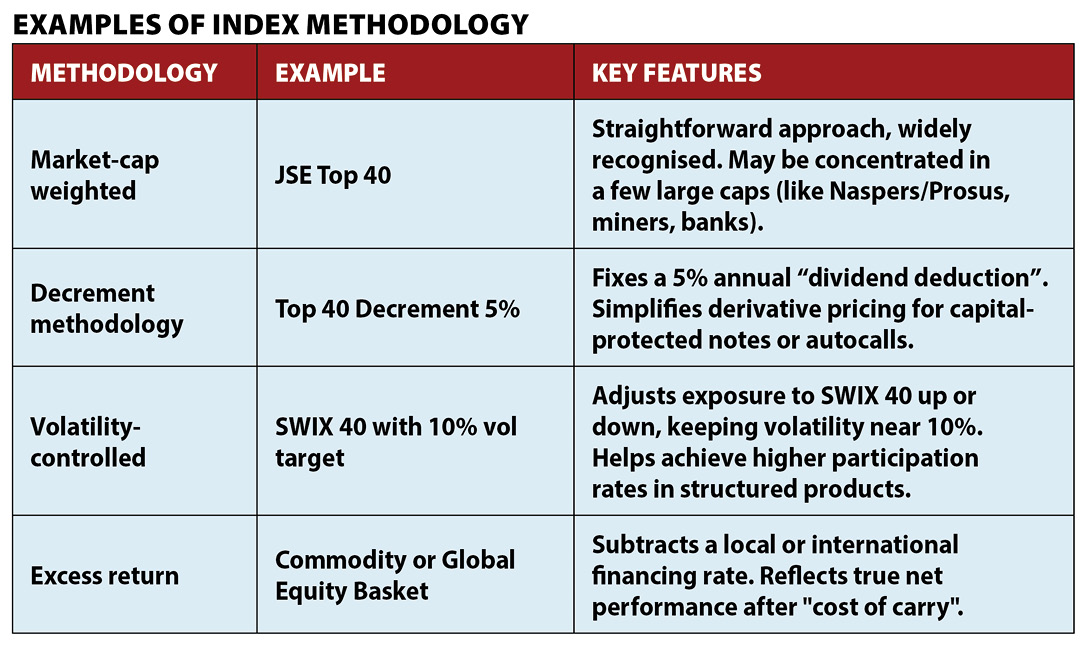

Index methodologies?

Five equity-index constructions drive most South African notes: market cap, equally weighted, decrement, excess return and volatility-controlled.

Different indices offer unique pros and cons, and understanding each helps ensure suitability.

A market-cap index, such as the JSE Top 40, assigns larger weights to bigger companies, making it easy to hedge as futures trade continuously. However, a dominant company like Naspers can influence the entire basket.

An equally weighted index, on the other hand, ensures that each share has the same weight, thereby enhancing diversification and reducing sector biases; however, it requires more frequent rebalancing.

A decrement index deducts a fixed dividend, for instance 5% before showing performance, which reduces the bank’s need to predict future dividends, thereby lowering option costs and increasing participation rates.

An excess-return index factors in a financing rate that typically reflects the carrying costs of futures contracts, making it particularly useful for hedgers as it accurately represents their actual costs within the payoff structure.

Lastly, a volatility-controlled index functions like an automated system with built-in speed limits, reducing equity exposure during periods of high market volatility to maintain a risk level of around 10%. This reduction in option costs allows the bank to offer complete capital protection with a higher potential upside.

Comparative narrative in the local context?

Market-cap options offer the best liquidity and provide a straightforward story, but they also pose concentration risk, making them the primary choice for first-wave capital-protected notes.

Equal-weight strategies offer greater diversification, though they come with higher turnover and slightly lower coupons and are typically used in “balanced exposure” barrier auto calls.

Decrement structures enable higher participation but may underperform if dividend increases occur, so they are commonly found in five-year growth notes.

Excess return products allow for precise hedging, although they generally yield lower headline returns, making them preferable for commodity-themed investments.

Volatility control (vol-control) offers the lowest-cost protection and strong multipliers but tends to lag during periods of rapid market gains. It is considered essential in fully protected global tech products.

In conclusion, the careful selection of an equity index methodology is pivotal in determining the success of capital protected notes and other structured products within the South African market. Each index type offers distinct advantages and considerations, from liquidity and diversification to cost and risk management.

By understanding and strategically leveraging these methodologies, issuers can optimise their offerings to meet the diverse needs of investors while adhering to regulatory requirements. As the FSCA mandates clear explanations for synthetic adjustments, transparency remains crucial in ensuring investor confidence and the efficacy of products.