Structured products can be powerful tools for delivering clearly defined, outcome-based investment exposures. Their effectiveness, however, depends on selecting a structure that aligns with the client’s objectives, risk appetite and required outcomes. Financial advisers play a key role in translating a complex toolkit into solutions clients can understand, compare and implement with discipline.

A structured product typically combines a debt or money-market component with a derivative overlay. In South Africa, the debt portion is often a zero-coupon bond that provides full or partial capital protection, influenced by interest rates, issuer credit spreads and the investment term. The derivative component – built from call options, and in some cases puts or barrier features – determines how investors participate in market movements through participation rates, caps, knock-ins and knock-outs. More protection generally means lower upside, while higher gearing usually comes with tighter caps or reduced protection.

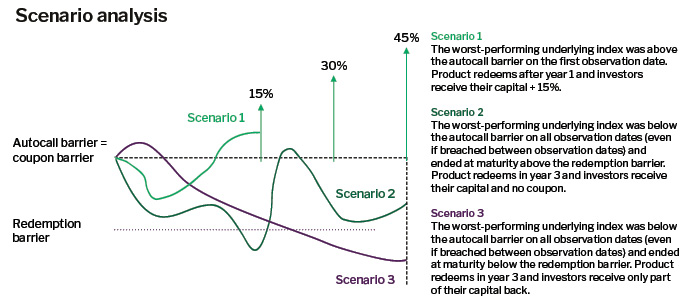

One advantage for advisers is the clarity of the risk/return trade-off: outcomes can be modelled and illustrated across downside, base-case and upside scenarios.

Matching the investor to the structure

In South Africa, commonly used structures include capital-protected notes, autocallables and geared strategies. Some providers, including Nedbank, also offer structured credit and monetised solutions for more sophisticated investors.

Capital-protected notes suit cautious clients seeking measured market participation while safeguarding some or all of their capital. Typical investors include retirees, trustees with preservation mandates or individuals prioritising stability after periods of volatility. The trade-off is typically lower potential upside.

Autocallable notes are suited to markets expected to be stable or moderately stronger. These structures include observation dates and trigger conditions that may result in early maturity with a predefined coupon. Coupons can accumulate (snowball), and downside barriers help determine capital outcomes at maturity. Advisers must clearly communicate stress scenarios, particularly markets drifting lower without breaching barriers or meeting call triggers.

Geared products sit at the higher-risk end of the spectrum. They offer multiples of underlying performance (for example, 1.5x or 2x) in exchange for reduced or conditional protection. Digital or contingent notes follow similar principles, paying coupons if certain conditions are met; otherwise, capital may be at risk. These structures suit aggressive investors or tactical allocations where higher volatility is acceptable.

Institutional applications

At institutional scale, structured credit and bespoke strategies broaden the opportunity set. Structured credit tranches loans or bonds into layers with different risk-return profiles, typically appropriate only for institutions with the ability to assess default risk, recovery assumptions and regulatory capital implications. As demonstrated during the 2008 global financial crisis,

issuer credit risk remains central – even “protected” notes rely on issuer solvency.

Monetised collars, offered by some providers including Nedbank, combine lending with option strategies for clients holding concentrated share positions who require liquidity without disposing of assets. By pairing a loan with a collar (selling a call and buying a put), investors can unlock liquidity while maintaining constrained exposure. These are highly tailored, sophisticated solutions suited to clients who understand the associated payoff dynamics and trade-offs.

Where structured products fit locally

For retail investors, structured products can provide offshore-linked exposure in rand-denominated, JSE-listed form – useful for those nearing foreign-allowance limits. For retirement funds and institutional investors, structured products can refine risk exposure, access new markets and introduce defined payoff profiles within Regulation 28 constraints.

Ultimately, structured products are tools within a broader portfolio rather than standalone strategies. The discipline lies in matching the structure to client objectives – preservation vs growth, income vs accumulation, domestic vs offshore exposure, and the client’s comfort with complexity. With proper due diligence and suitability assessment, structured products can form a clear, measurable component of a well-constructed investment strategy.