They found that, on average, asset allocation explained more than 90% of a portfolio’s return variability. Furthermore, they found that active management (security selection and market timing) cost the average plan 1.1% per annum when compared to a passive policy benchmark. They confirmed their research in a follow-up study titled Determinants of Portfolio Performance II: An Update (1991).

Their research is often misquoted as confirming that asset allocation contributes more than 90% of a portfolio’s returns whereas it aimed to determine the variability of returns. In other words, their research found that asset allocation accounted for more than 90% of the dispersion in active returns of the sample (the range of active returns) and not the absolute contribution thereof.

Their results are often used as an indictment against active management. Both interpretations are misguided as it ignores the hypothesis tested and limitations to the study.

Nevertheless, their research remains groundbreaking as it was the first to highlight the importance of asset allocation. But how relevant is it in a South African context?

To answer this question, we analysed the quarterly returns and asset allocation of four major multi-asset categories as defined by the Association for Savings and Investment South Africa (ASISA) for the period 1 January 2020 to 31 December 2025. We adjusted the net return series of each category by the median total investment charge to arrive at a comparable gross return. In decomposing the returns, we applied the total return of the headline index for each asset class to the average exposure weight of the category during the period.

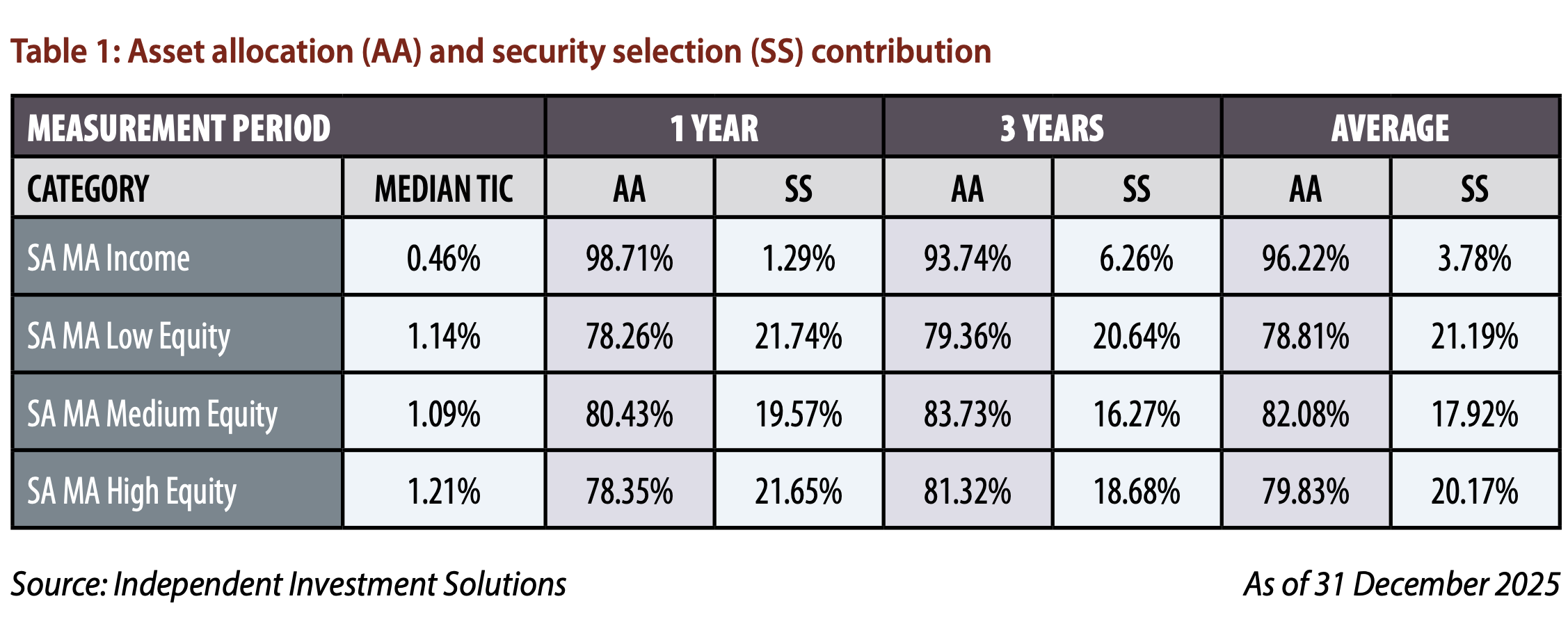

The results are summarised in Table 1, which presents the average of the rolling average asset allocation and security selection contribution to the category’s total gross return. In other words, what was the average contribution to the category’s total return from asset allocation and security selection over a rolling one- and three-year measurement period?

The results confirm the overall premise of the research presented by Brinson, Hood and Beebower (1986, 1991) in that asset allocation accounts for the majority of portfolio return variance for the categories measured. Our study differs in that it quantifies the average percentage contribution from each category.

Apart from the South African multi-asset income category, the contribution from asset allocation was roughly 80% and 20% from security selection. The deviation in the income category is non- surprising as the category derives its returns primarily from fixed income assets. The nature of the category (what it is used for) also means that maximum exposure to growth assets is unlikely.

In conclusion, our study has confirmed that asset allocation remains the most important decision in portfolio construction. Although there were quarters where the contribution from security selection outweighed that of asset allocation, these instances were sporadic and inconsistent. Furthermore, as the measurement period was extended, the greater the impact of asset allocation became. There was not a single three- year datapoint where the contribution of security selection outweighed that of asset allocation. So, ignore asset allocation at your peril.