Some criticise financial planners for using a DFM because they argue that the financial planner is outsourcing a primary function of financial planning. This critique can be easily countered by using the medical analogy of a general practitioner who, like a financial planner, has the role of diagnosing the overall health of a client, determining what specific needs they have and then accessing specialists to address those needs.

The financial planner is there to guide the client on their lifetime financial journey and to oversee the use of specialists as and when needed such as DFMs, insurance brokers, medical aid specialists, accountants, fiduciary and tax practitioners. However, one critique that can be more difficult to counter is that of cost, particularly if the use of the DFM leads to additional costs to the client. There is the debate about whether the client should actually be paying for the DFM, as opposed to the financial planner paying the DFM out of their fee, in the way that they might pay another service provider that they use.

Either way, as Warren Buffett says, “price is only an issue in the absence of value”, so it is important that the benefit to the client is clear if they are paying more for the service. There is no doubt that using a DFM is of significant benefit to a financial planner.

When it comes to investments, their operational, compliance, communication and administrative processes should be simpler and more efficient. The financial planner will then have time freed up that otherwise would have been spent on researching and selecting investments, thus enabling them to add more value in other aspects of financial planning, particularly time spent engaging with their clients.

Naturally if the financial planner is experiencing these benefits, there should be a knock-on benefit to the client and, perhaps most importantly, there will be greater consistency in the process and outcome of the client’s investments. Given the direct impact that costs can have on a client’s investments, it is important to consider key aspects of cost when a financial planner uses a DFM.

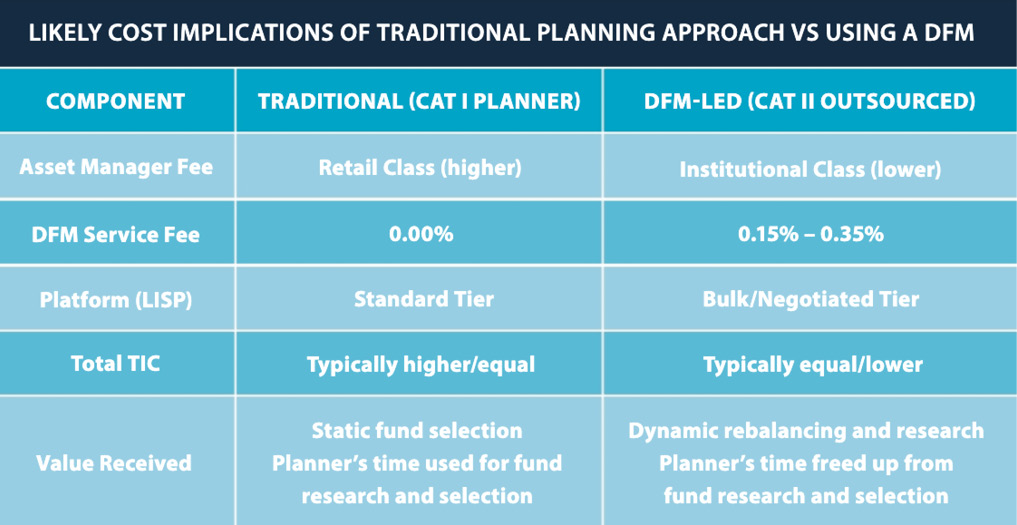

A. Do clients pay more or less if a financial planner uses a DFM?

There is no doubt that using a DFM adds a new fee layer to a client’s costs. However, this does not necessarily mean that the client’s overall costs are higher; in fact they are often neutral or even lower. A DFM typically charges between 0.15% and 0.35% on assets invested in a model portfolio, but a key value add of a DFM is their ability to switch clients from retail fee classes to institutional fee classes.

This switch can materially lower the cost of funds that a financial planner may previously have invested into on behalf of their clients. In some cases the fee reduction could be as much as half.

Another way that DFMs that have their own funds can reduce investment fees is by offsetting a portion of the DFM fee when using the DFM’s own funds. The DFM obviously has to balance this cost saving with the risk of a perceived or real conflict of interest by including one or more of their own funds in a model portfolio.

Given that DFMs are dedicated investment specialists and in effect are “active” managers of model portfolios, they have tended to be more open to using passive funds in model portfolios than financial planners may historically have been in the portfolios they previously “managed” for clients.

Hence DFMs are also able to reduce costs by including low-cost passive funds in model portfolios. By blending active and passive managers in a model portfolio, DFMs are able to offer financial planners an “actively” managed portfolio but at much lower cost.

Arguably the use of DFMs provides clients with the opportunity to get the best of both worlds. They continue to get their financial advice at the same advice fee – but ideally getting more attention and better service from the financial planner, while their investment fee is lower thanks to the DFM’s ability to use their investment expertise and scale to reduce the cost of investment management.

So while a DFM adds a new fee layer, the net result for the client can at the very least be neutral or even lower.

B. What sort of scale benefits do (or should) DFMs offer?

Scale is probably the primary lever a DFM uses to justify its existence beyond just “picking funds” or helping financial planners improve the operational efficiency and compliance obligations of their investment process. Scale manifests itself in various forms:

- Aggregated buying power: A DFM with R10-billion in assets has far more negotiating leverage with a tier-1 asset manager than a single financial planning practice with R100-million. This leverage is not only with respect to fund price negotiations but can also lead to access to exclusive mandates.

- Operational alpha: Use of a Category II licence allows for “bulk switching”. This means all clients are moved simultaneously at the touch of a button, ensuring no client is disadvantaged by adminis- trative delays – a key TCF (Treating Customers Fairly) benefit.

- Reduced “drag”: DFMs can optimise the use of cash and passive “building blocks” (ETFs/index trackers) within a portfolio to lower the weighted average cost without sacrificing the tactical house view.

- Investment research: Given their asset buying power, DFMs have far more access to asset managers to conduct research than financial planners who are managing their clients’ money. This access means that those DFMs that value the importance of qualitative fund manager research are able to do this to a depth which they determine, rather than relying on the asset manager’s discretion about information that they deem important.

One disadvantage of the scale that DFMs have achieved is that the relationship between asset managers and financial planners has been at least disrupted, and at worst, disintermediated. DFMs have overhauled the investment landscape to the extent that they are now seen as an important distribution channel for asset managers. Naturally the bigger the DFM, the more likely they will be feted by asset managers. This has forced asset managers to rethink their approach to servicing financial planners.

C. How transparent are all the costs in the DFM value chain?

Transparency is no longer optional and is a regulatory requirement under ASISA standards.

In 2016 ASISA introduced the Effective Annual Cost (EAC) Standard as the “gold standard” for cost disclosure. It breaks down the costs of an investment into four clear buckets:

- Investment management – reflects all costs and charges for underlying investments, including the annual investment management fee, any initial charges, ongoing charges like performance fees and transaction costs (such as for trading). Here the DFM fee should be reflected as a separate fee from the underlying investment manager fees.

- Advice – reflects the fee that the financial planner and client have agreed, for initial and/or ongoing advice.

- Administration – reflects all costs an investor incurs related to the administration of the product by the product provider – in the case of model portfolios managed by a DFM, this fee is often simply the LISP fee.

- Other – includes any other costs, such as termination charges, penalties, costs of guarantees, smoothing or risk benefit costs, loyalty bonuses, etc. It is meant as a “catch-all” for any remaining costs and each of these costs must be explained in notes accompanying the EAC table.

Why transparency is such an issue

The evolution of DFMs has led to the risk of “double dipping” – a practice of taking two fees on the same asset, which often happens without clients being aware of it, never mind consenting to it. “Double dipping” can happen in various ways – the three key methods are outlined below:

- Level 1 – the fund fee: When a DFM uses its own proprietary funds within a model portfolio it creates a potential conflict of interest – it is effectively earning two fees on the same asset: a DFM fee and a fund fee. Ideally a transparent DFM would either rebate the DFM service fee or ensure the underlying fund fee is discounted to avoid charging the client twice for the same expertise.

- Level 2 – the DFM fee: There is potentially a second level of double dipping where a financial planner benefits from the DFM fee. Some DFMs incentivise financial planners by sharing a portion of the DFM fee with the financial planner. While this may be justified because the financial planner potentially does some investment work – be it sitting on a Joint Investment Committee or preparing investment communications to their clients – being transparent would mean disclosing this fee or “rebate” to the client.

- Level 3 – model portfolio fee: Some financial planning businesses who use DFMs may have their own Cat II licence and “own” the funds or model portfolios in which clients invest. With this level of ownership comes an asset-based fee, some or all of which may be rebated to the financial planner from the DFM fee or the investment management fee. Again, transparency means disclosing this arrangement to the client.

Whatever the arrangement that a financial planner has with a DFM, an approach that is aligned with TCF would ensure that the “look-through” principle applies and that on the fund fact sheet of every model portfolio managed by the DFM, all four levels of the investment EAC are disclosed, including any rebate arrangement with the financial planner.