Every individual’s investment journey is unique, but broadly speaking we can split each journey into three phases: wealth accumulation, wealth growth and preservation, and wealth distribution.

The journey typically goes a little something like this – at the start of their career there is a greater risk appetite, so a traditional portfolio will include a predominantly equity bias with very little room for the likes of bonds and cash. The goal here is to capture as much upside as possible, with a higher tolerance for drawdowns, which, given the long runway to wealth distribution, can be seen as more of an opportunity to invest capital at cheaper prices. As they approach peak earnings, investors will throttle back on the equity allocation and begin the transition towards a more balanced portfolio, including the likes of bonds and cash to act as a ballast against market drawdowns and volatility. As investors approach retirement, their priorities should change: low volatility, a smooth return profile and capital preservation are the name of the game.

Historically, this approach has worked, but as we have observed over the last decade or so, markets have become a lot more volatile, leading to large market drawdowns and lumpy returns. Over the last 5 years, investors have had to stomach record global debt levels, a US-China trade war, a Russian invasion of Ukraine, and most notably the pandemic and subsequent resurgence of inflation.

Portfolio longevity and sequencing risk during this volatile period have certainly been front of mind for many investors, and volatile market conditions have had a detrimental impact on many portfolios – in particular for those investors in the latter part of their investment journey, with a large allocation to fixed income instruments.

Why this time is different for fixed income investors

The resurgence of inflation has seen an end to the great bond bull market of the last 40 years. Consequently, this has been a drag on many fixed income instruments. Using the iShares 20+ Year Treasury Bond ETF (“TLT”) as a proxy for developed market fixed income performance, we can clearly demonstrate that one of the cornerstone asset classes for decades has produced an annualised return of -13% over the last 3 years. Losses of this magnitude have highlighted that fixed income investments have not necessarily functioned as the portfolio ballast they were supposed to be.

In the South African context, balanced funds are a popular choice to add stability to a portfolio and generate the smooth return profile investors are looking for. The fact sheets and marketing material of many brand name balanced funds flaunt what looks like impressive real returns. However, in light of the recent drag on performance of fixed income on these portfolios, not to mention the equity performance, it will be worthwhile to broaden the scope of investor allocations to include alternatives such as hedge funds. By doing this, investors are likely to achieve greater absolute and risk-adjusted returns with little to no correlation to the market.

Digging into the data

Over the last 14 years (the inception date of the hedge fund referred to below), an equal weighted index of the largest balanced funds in South Africa has returned 8.83% per annum, with a 76% correlation to the JSE ALSI and a Sharpe ratio (risk-adjusted return) of 0.31. The JSE ALSI has achieved 12.78% per annum, at a Sharpe ratio of 0.44.

Interestingly, this implies that the JSE ALSI provides better risk-adjusted returns than an equal weighted composite index of some of South Africa’s largest balanced funds. The Steyn Capital SNN QI Hedge Fund, on the other hand, has returned 16.98% per annum (net of fees) with a 13% correlation to the JSE ALSI, and a Sharpe ratio of 0.97. In other words, the Steyn Capital SNN QI Hedge Fund has achieved better absolute and risk-adjusted returns, with little to no correlation to the JSE ALSI.

Now it would be disingenuous to suggest that one should abandon balanced funds entirely in favour of hedge funds when that is practically not possible. However, recent changes to Reg 28 allow for a 10% allocation to hedge funds, and our analysis indicates that maximising this allocation is likely to generate greater absolute and risk-adjusted returns. Given the low correlation to the market, it also allows for higher beta allocations in the rest of the portfolio, affording the individual and advisor greater flexibility when it comes to portfolio construction.

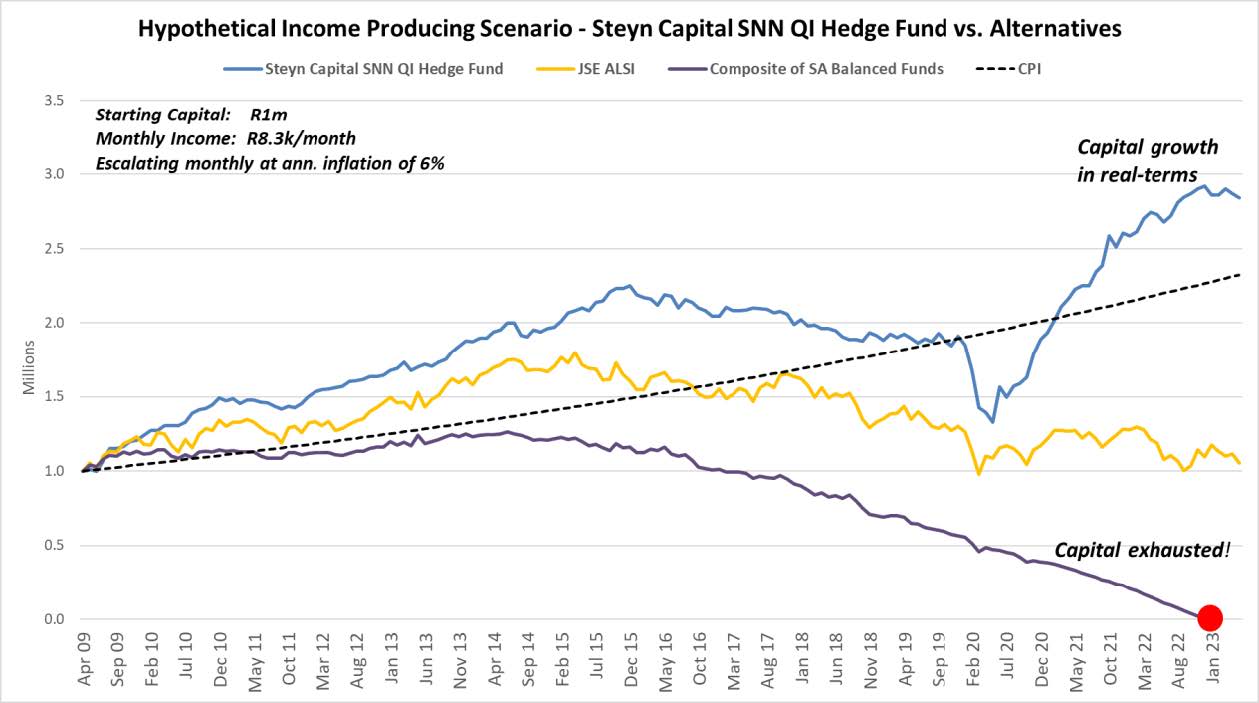

An allocation to hedge funds can also be beneficial at the end of the investment journey

Let’s look at a practical example. Three individuals retire in May 2009, with a million rand each: one invests exclusively in the JSE ALSI, one in an equal weighted composite index of the largest balanced funds, and one into the Steyn Capital SNN QI Hedge Fund. All three investors draw R8,333 (10% of starting capital annually) per month, increasing the withdrawals monthly at a CPI rate of 6% per annum. The results from analysing these three scenarios for the period to May 2023 are both interesting and concerning. The investor in the JSE ALSI has drawn on more than half of their capital in real terms. The balanced fund investor would have exhausted all of their capital at the start of this year. The hedge fund investor, on the other hand, would have grown their entire capital base in both real and absolute terms.

Globally, market gyrations continue. The China reopening has been slow to get out of first gear, as the market continues to beg for more stimulus; US market valuations are becoming stretched (again); and the full impact of Fed tightening is yet to be felt. Hedge funds are more than just a bridge over troubled water. They are a fantastic diversification tool that can generate uncorrelated and consistent returns under most market conditions. Lower volatility and correlation allow for a smoother return profile, and importantly provides greater flexibility for the rest of the portfolio construction process. As they say, diversification is the only free lunch in investing.

Due to investor demand for a daily traded retail version of the Steyn Capital SNN QI Hedge Fund, we launched the Steyn Capital SNN Daily-Liquidity Retail Hedge Fund on October 18, 2022. This fund offers daily liquidity and a modest minimum investment amount of R10,000, and is currently available on the Momentum Wealth, Glacier, Allan Gray and Ninety One Platforms.

If you’d like to learn more, or request access on specific platforms, please contact us at www.steyncapitalmanagement.com or jamie@steyncapitalmanagement.com, or on 021 001 4682.