Most investors prepare for the risks they’ve already seen, market drawdowns, bad years, volatile headlines. What we struggle to prepare for are the risks we can’t easily imagine – the things that catch us all off guard. That challenge feels especially relevant today. Markets have delivered strong returns, leadership has become increasingly concentrated, and it’s tempting to believe that “what’s worked” will simply keep working.

Morningstar’s latest research highlights a growing concern: the risk of putting too much capital into too few places, whether that’s a single market, sector, or small group of dominant companies.

Risk isn’t just volatility: Traditionally, risk is measured as how much returns move around volatility. But volatility doesn’t tell the full story. It treats upside and downside as the same, and it doesn’t capture the risks that matter most to investors’ real lives and long-term goals.

Three risks tend to matter far more than just volatility.

- The Risk of Opportunity Cost:

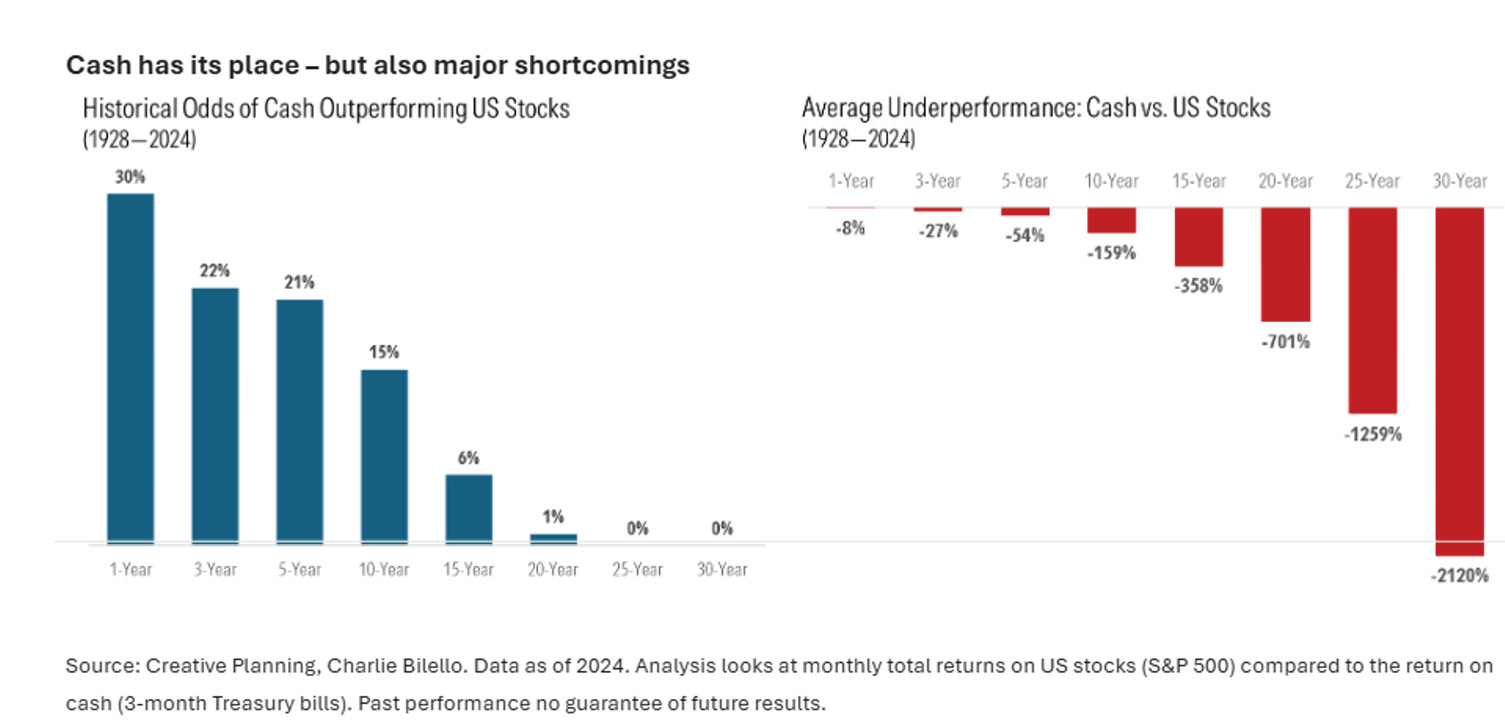

Being too cautious can be just as damaging as being too aggressive. Over time, portfolios that avoid growth assets altogether often struggle to keep up with inflation and long-term return targets. While equities bring short-term volatility, they also provide the return engine needed to grow purchasing power over decades. The risk isn’t just losing money; it’s not earning enough to meet future goals.

.

Cash has its place – but also major shortcomings

Source: Creative Planning, Charlie Bilello. Data as of 2024. Analysis looks at monthly total returns on US stocks (S&P 500) compared to the return on cash (3-month Treasury bills). Past performance no guarantee of future results.

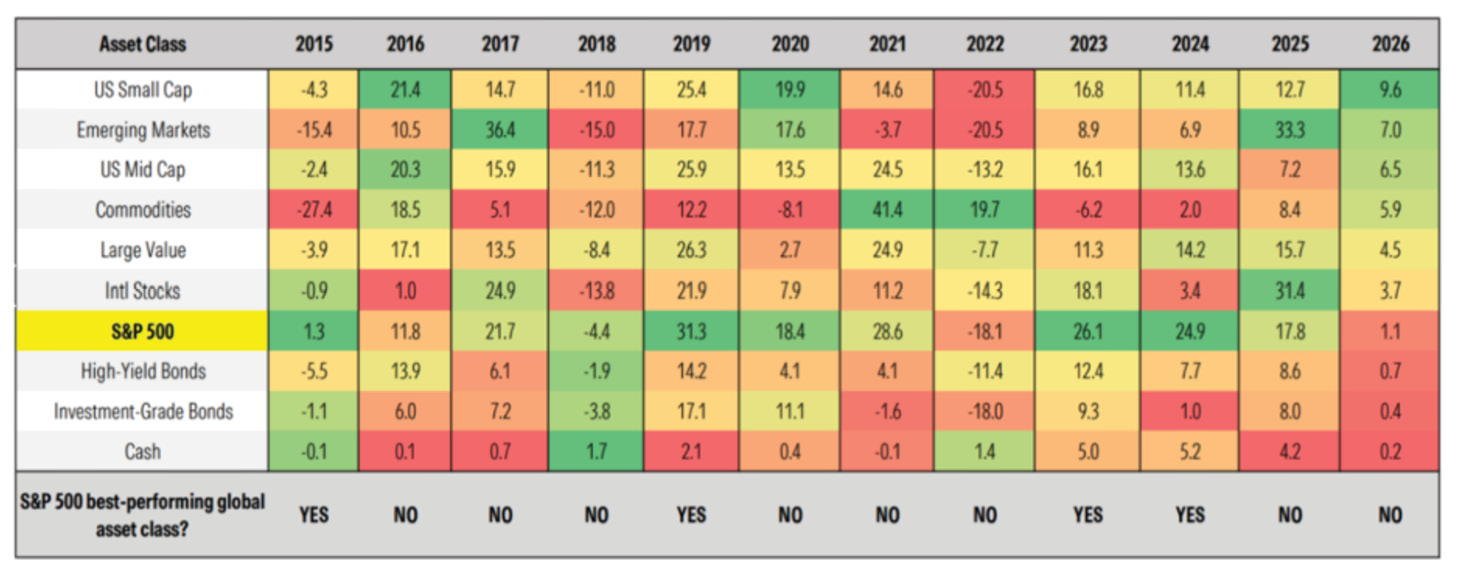

- Concentration Risk

This is where today’s market environment becomes especially relevant. When returns become driven by a narrow part of the market, whether a handful of mega-cap stocks, one country, or one investment style, portfolios can quietly become riskier. No asset class, market, or manager outperforms all the time. History shows that leadership rotates, often when investors least expect it.

Diversification across regions, asset classes, and investment styles isn’t about smoothing every bump, it’s about reducing dependence on a single outcome going right. As Morningstar’s latest research points out, putting “too much in one place” can feel comfortable when it’s working, but it can quickly become the dominant source of risk when conditions change.

No asset class wins all the time

Source: Morningstar Direct as at 20 January 2026. ETFs used for performance analysis. References to individual securities not an offer to buy or sell. Past performance is not a guarantee of future results.

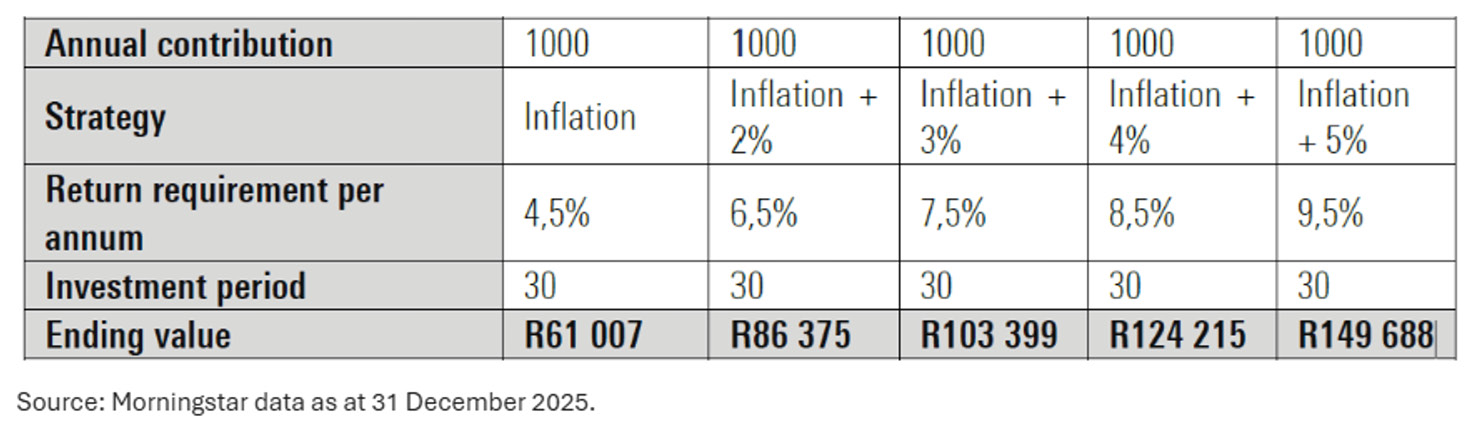

- The Risk of Falling Short

This is the risk that ultimately matters most. Small differences in long-term returns can translate into large differences in outcomes. Being in the wrong strategy for too long, often driven by fear or recent performance, can leave investors meaningfully behind where they need to be. Avoiding short-term discomfort at the cost of long-term progress can be one of the most expensive decisions an investor makes.

Active asset allocation: Risk isn’t something to eliminate. It’s something to understand, diversify, and align with purpose. Markets will always be uncertain. Volatility will always show up. But over time, the biggest risks tend to come from being too concentrated, too cautious, or too reactive to what just happened.

That’s why disciplined diversification matters – and why partnering with active, experienced managers can be so powerful. Skilled managers don’t just spread risk across assets, regions, and styles; they interpret risk. They apply research, judgement, and real-world experience to identify opportunities, avoid pitfalls, and rebalance thoughtfully as conditions evolve. The goal isn’t to predict what will win next, but to build resilience – so portfolios are not dependent on any single story, trend, or assumption being right.

Risk Warnings

This commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar Investment Management South Africa (Pty) Ltd makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this commentary. Except as otherwise required by law, Morningstar Investment Management South Africa (Pty) Ltd shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use.

This document may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking state/ments. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

Morningstar Investment Management South Africa Disclosure

The Morningstar Investment Management group comprises Morningstar Inc.’s registered entities worldwide, including South Africa. Morningstar Investment Management South Africa (Pty) Ltd is an authorised financial services provider (FSP 45679) regulated by the Financial Sector Conduct Authority and is the entity providing the advisory/discretionary management services.