It is well known that the energy transition – the shift from fossil fuel to renewable energy – needs to take place urgently in order to save the planet from the dire effects of climate change.

But what does this mean for the energy industry? In our view, it has to undergo three structural changes in order to reduce carbon emissions.

Decarbonisation of power generation

Power production needs to become less carbon-intensive.; in fact, a ‘virtually full’ decarbonisation of the power sector needs to happen by 2050 in order for the world to meet the Paris Agreement’s 2oC target, according to the Intergovernmental Panel on Climate Change (IPCC).

This means that the share of power generated from renewables has to increase. It’s estimated that it will rise from 20% to 80% by 2050 as decarbonisation efforts are undertaken. The majority of this increase will come from wind, solar and small molecular reactor energy.

But this growth doesn’t take into account that the population will grow between now and 2050, likely to 9.5 billion then. Energy consumption is also forecast to grow at around 4% per annum.

What does this mean? It means we could see renewables taking up an even greater share of electricity generation. Add to this the fact that renewables are now cheaper than coal and gas power across two-thirds of the world, and there’s a compelling case to argue that there’s going to be more and more demand for renewable energy between now and 2050.

Electrification of energy use

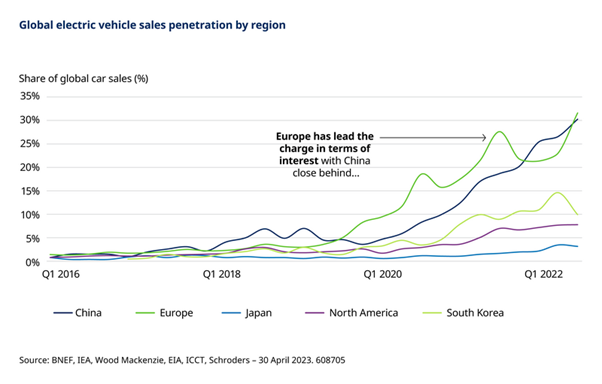

At the moment, the majority of the energy we consume is not electricity – it’s gas to heat homes (particularly in Western Europe and North America) and oil to power vehicles. However, new policies around the world are starting to prevent the use of fossil fuels in power production and transportation which means electric vehicles are going to become more prevalent. Indeed penetration rates of electric vehicles are already starting to increase. As this happens, the share of electricity in final energy consumption is going to grow from 20% to 45% by 2050.

Increased efficiency of energy consumption

Increased demand for electric vehicles, alongside higher demand for residential solar and storage, and energy efficient appliances should drive down the energy intensity of the global economy. This is a good thing because the energy intensity of the global economy must fall by nearly two-thirds by 2050 to limit the growth in overall power consumption that will necessarily arise from factors such as population growth and the ongoing industrialisation of developing economies.

What does this mean for investors?

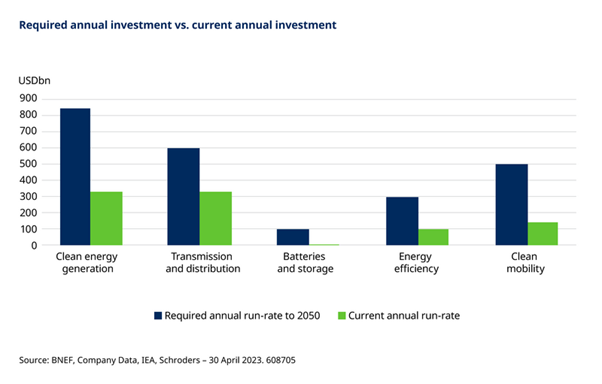

In a nutshell, it means there is going to be a significant amount invested into energy, whether that’s to produce renewable power or improve grid infrastructure to handle new sources of power. It’s estimated that $100 trillion needs to be spent across the energy industry by 2050 in order to achieve the required carbon emissions reductions. We are nowhere near that currently, so investment rates need to increase substantially.

For example, India wants to generate 450 gigawatts of renewable power between now and 2030. The entire global offshore wind market is currently about 18 gigawatts per annum. That’s a significant amount of investment into renewable power by India alone.

But investment isn’t just going to be made into renewables like wind and solar. Investment is needed across the value chain.

New transmission and distribution mechanisms are going to be needed. New renewable assets must be connected to the grid with new transmission lines, which will create new demand for cables and electrical equipment. As more and more people use clean electricity, local electrical distribution grids will also need to be upgraded to prevent blackouts.

Electric vehicles will also need charging points and buildings will need to become less energy-intensive and more efficient, whether that’s through smart meters or energy control management solutions.

Energy storage solutions across different parts of the electricity system will be critical, given the intermittent nature of renewable sources like wind and solar.

The bottom line is that we are about to enter into a period of net energy investment. While the past shouldn’t be relied upon as a predictor of the future, the good news for equity investors is that energy equities have outperformed other equities during prior such net energy investment periods.

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy.

Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of investments to fall as well as rise.

The views and opinions contained herein are those of the individuals to whom they are attributed and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy.

Issued in June 2023 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998