What is the industry telling us?

According to a Moonstone article posted by Mark Bechard in March 2026, Eugene du Toit, FSCA divisional executive for regulatory policy, said at the FSCA Industry Conference that he was “fairly certain” the Conduct of Financial Institutions (COFI) Bill would probably be tabled in parliament in 2026.

FAnews reported on some of the conference keynote presentations on 18 March 2026 in an article by Gareth Stokes. According to Stokes, FSCA commissioner Unathi Kamlana said, “The real question for the industry is not when COFI will arrive, but how prepared institutions are for the regulatory model that COFI represents.”

For leading financial service providers (FSPs) this is a significant clue. It is not surprising that Du Toit specifically cautioned financial institutions against delaying preparation for this substantial shift in conduct regulation. The transition from FAIS to the COFI represents one of the most significant shifts in the history of South Africa’s financial services industry. Beyond regulatory commentary and industry speculation, a critical question remains:

How prepared are FSPs for the transition?

To explore this, I conducted a series of three full-day strategic planning workshops with financial advisory businesses, engaging with key individuals responsible for steering their firms through this transition. These sessions, attended predominantly by members of the governing body of FSPs offering advice on long-term insurance and investment products, created a unique opportunity to capture the current sentiment and COFI-readiness across the industry.

Through structured poll questions, a clear “state of the nation” began to emerge, revealing not only awareness and preparedness levels, but also the underlying attitudes, uncertainties and strategic gaps that will determine how firms will navigate the shift from compliance to conduct. The key responses of all three events were combined for purposes of this article, which I hope you find insightful.

Leadership. Between 74% and 92% of respondents opine that leadership will matter significantly when it comes to the effective transition from FAIS to COFI. A total of 87.2% of delegates agree governing bodies will have to lead at a higher level under COFI than with FAIS.

Mindset. Between 71% and 96.4% of respondents believe that a growth mindset, not a groan mindset, will be required for an effectual switch. A growth-oriented governing body will view COFI as an opportunity to build a stronger, more client-centred business. A groan-mindset governing body will see it as an additional compliance burden to manage reactively.

Culture and governance. Delegates were asked whether, during everyday business, the importance of culture and effectiveness of governance play a critical role in leading firms.

- 91.9% of respondents rated culture as extremely important.

- 92.4% rated governance as extremely important.

- 80.8% of delegates believe that members of governing bodies will need COFI training.

- 89.5% confirmed that failure to implement a proactive COFI strategy poses a risk to FSPs.

Capacity. The lack of capacity to meet FSP responsibilities due to the complexity and onerous nature of the regulatory environment is concerning. A total of 94.1% of respondents are at or beyond capacity. This is not a temporary condition. It reflects a structural industry problem where the administrative and compliance burden under FAIS has outpaced the human capital available in most FSPs.

COFI will increase this burden in the short term before it becomes manageable. FSPs that do not address the capacity constraint proactively through visionary leadership, team development, simplification, optimisation of systems, enhancement of business efficiencies and outsourcing won’t have the capacity to implement COFI properly.

What do industry stakeholders, like product providers and compliance officers, tell advisors?

Our poll results show that 88% of delegates are currently being guided as follows:

- Just carry on doing what you are doing.

- Wait for promulgation before acting.

- We do not know what COFI will require yet.

- There will be a long time to prepare.

Observations

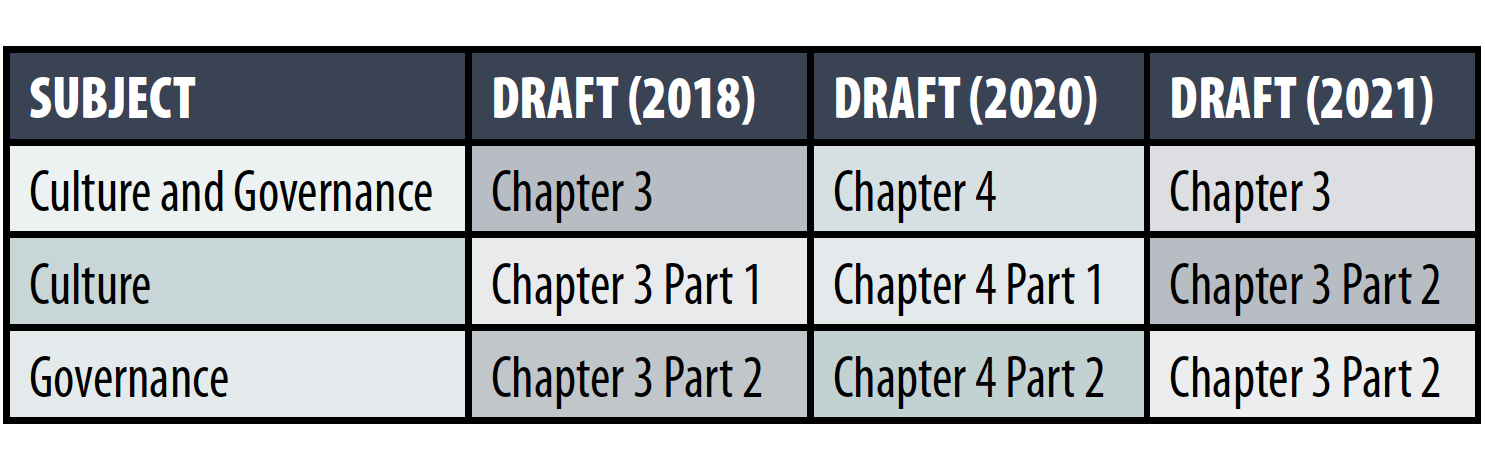

Respectfully, this advice flies in the face of what FSCA has been communicating. I disagree that we don’t know what will be included in the Act and its conduct standards. As a student of market conduct legislation and an FPI-approved CPD provider, I have studied three drafts of the COFI Bill (2018, 2020 and 2021), the FAIS Act, its subordinate legislation with specific reference to Board Notice 194 of 2017 (Fit-and-Proper requirements), the FAIS General Code of Conduct and Conduct Standard 3 for Banks. This is what I found:

All three versions of the COFI Bill have included the same market conduct themes and principles. My analysis shows that between 90% and 95% of the principles have remained the same. The only material changes were the order they appeared in when they were published with immaterial changes in the wording.

For example:

- The preamble and objective of all three Bills fundamentally remained the same.

- The chapter on Culture and Governance contain the same fundamentals but were moved around in the various versions of the Bill as illustrated below:

- Reference to the contractual relationship between FSPs and financial customers has been constant in the various versions of the Bill. The principle that financial services rest on contract law extends the core FAIS Act principles upheld for over 21 years and reaffirmed in Conduct Standard 3 for Banks.

With absolute certainty, the principles pertaining to the application of the contractual relationship between FSPs, their representatives and financial customers will be incorporated in COFI. We know with 99% certainty that the principles highlighted above will be included in the COFI Act, and we know with equal certainty that the Conduct Standards pertaining to client engagement will include most of the principles that have been included in the General Code of Conduct and as part of the Retail Distribution Review deliberations.

These principles promote trust and confidence in the financial sector. I believe that if they are not included in the COFI Act, it will demonstrate an inconsistent message from the legislator, which will contradict the sound principles demonstrated since the introduction of the FAIS Act. Hundreds of FAIS Ombud determinations have been published where market conduct principles were deliberated and stress-tested, and in some cases, subject to intense legal battles in the High Court and in the Supreme Court of Appeal. There is no way that the legislator will introduce different principles that have been part of our law for over 21 years.

From a COFI perspective, the foundation for FSPs has been firmly established by the FAIS Act, the Fit-and-Proper requirements and the General Code of Conduct. COFI will require FSPs to undergo a 10% to 15% facelift, but the foundation has been laid firmly.

Conclusion

The COFI Bill offers enough certainty to prepare now. Those who wait until promulgation of the Act before preparing to implement a sound FAIS-to-COFI transition plan will lag the innovators. I agree with Du Toit’s caution against delaying preparation for this significant shift in regulation. There are many FSPs who have started preparing for their FAIS-to-COFI passage. If you want to prepare, the following weblinks will give you complimentary access to the first edition of Solving the COFI Puzzle and a comprehensive COFI Readiness Assessment.

CLICK here Solving the COFI Puzzle CLICK here COFI Readiness Assessment