The rise of Artificial Intelligence in the world of financial planning and investment management is often portrayed as a binary choice: either it replaces the human professional, or it empowers them. In reality, AI is becoming the “silent partner” of professionals across the board, and the question is to what extent has, and will, AI impact DFMs.

A. How will DFMs use AI to make their services more efficient?

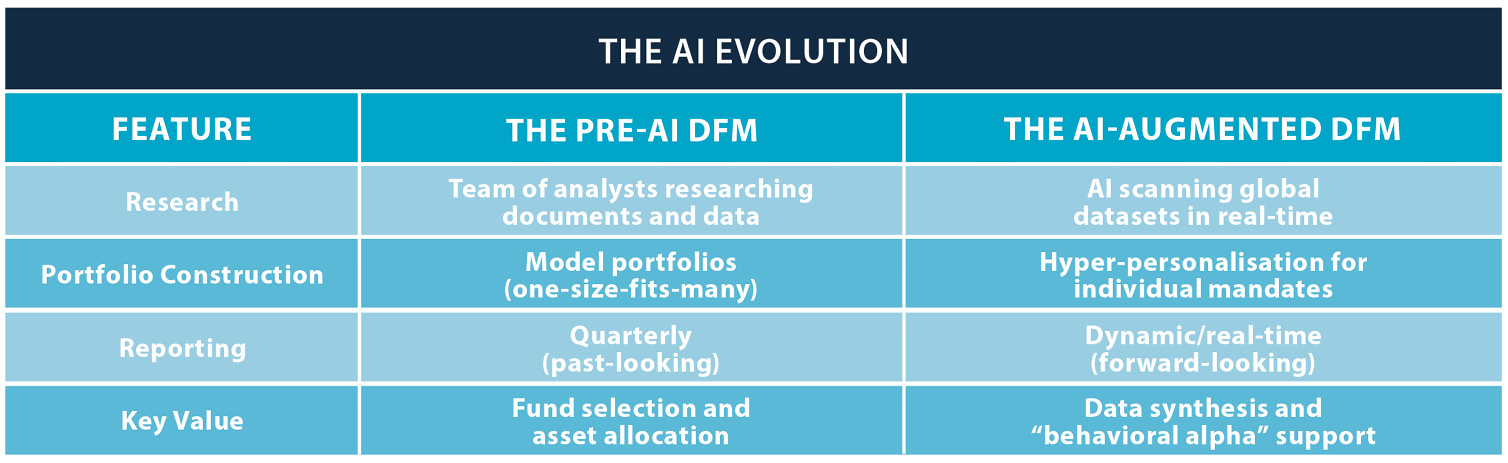

The scope for DFMs to use AI to improve their efficiency and service offering is significant. The range of applications covers a broad spectrum from – on the simpler end – AI assisting with mundane operational and administrative tasks, to the more complex use of “Agentic AI” to perform complex tasks like in-depth research or customised reporting.

The FSCA has identified four areas in which AI will impact businesses in the financial services sector. This provides a useful framework to consider the ability of AI to enhance a DFM’s efficiency.

1) Operational efficiency

The operational efficiency of a DFM could be enhanced in a number of key ways. Most immediately, through “intelligent automation”, AI can automate routine tasks, reduce manual intervention and minimise errors. For a DFM this is likely to apply to administrative tasks such as managing cash flows in and out of portfolios, as well as fulfilling portfolio reporting obligations, whether daily, monthly or quarterly. Automation invariably leads to quicker processing of transactions and applications, enhancing overall efficiency. In addition to this, AI can help with Operational Straight-Through Processing (STP) and could be used to reconcile trades across different LISP platforms, flagging errors or pricing discrepancies instantly, which significantly reduces the potential for “platform drag”.

2) Personalised client experience

AI-powered tools like chatbots and virtual assistants can provide quick and accurate responses, enhancing customer service and satisfaction. For example, DFMs could use chatbots to engage with administrators and/or financial planners to enhance the response time to queries.

AI provides the potential for hyper-personalised services, for example offering individual bespoke portfolios per client depending on their personal needs. This offering would be supported by hyper-personalised reporting as AI would allow DFMs to generate thousands of bespoke client reports in seconds. Even if the DFM doesn’t offer individual bespoke portfolios, but “buckets” of bespoke portfolios, AI would enable the DFM to deliver more than a generic market update so that a client could receive a report that explains how recent volatility impacted their specific portfolio, depending on their current asset allocation and time invested in the portfolio.

Whether using a chatbot or another tool, AI tools can handle a wide range of client interactions, from basic queries to complex transactions. This means DFMs will be able in real-time to help financial planners on any aspect of a portfolio and/or a client’s position/balance, ensuring that a personalised experience is consistently delivered.

3) Risk management and compliance

AI tools can help DFMs manage risk and ensure compliance both from an operational and investment perspective. AI systems can monitor operational processes in real-time, identifying inefficiencies and potential risks. This helps DFMs improve their operational resilience and the fact that AI-powered tools can automate repetitive tasks means the human members of a DFM team may be freed up to focus on more strategic activities.

Real-time and continuous monitoring of portfolios means that DFMs are quickly, and at an early stage, able to detect and prevent any risks that portfolios may be subjected to, whether based on macro-economic factors or market upheavals, or more micro-problems such as an issue with any underlying fund managers.

4) Data-driven decision-making

Given that AI systems enable the rapid processing and analysis of large, complex datasets to identify trends, correlations and anomalies, they can support evidence-based decision-making in model portfolios and can also inform the development of new portfolios that clients may need.

The ability of AI to scan and analyse vast datasets means DFMs can use this to scan economic and market data, as well as fund manager performance data. This not only reduces research and analysis time dramatically, but also enables potentially more informed decisions to be made by DFMs, whether it be in adjusting asset allocations or hiring and firing fund managers.

B. How will the use of AI impact the costs of service delivery and fees to clients?

The “AI dividend” has the potential to be a double-edged sword. On the one hand it has the potential to reduce operational costs, but on the other it will require investment from DFMs to ensure that they are able to use AI effectively and efficiently, with the necessary governance and ethical structures in place.

Lowering the costs of “production”

As AI increasingly takes on “responsibilities” for activities like fund research, portfolio construction and administrative rebalancing, the operational cost for a DFM will inevitably decrease. This should help keep DFM fees stable (or even push them slightly lower) even as regulatory and compliance costs may rise.

Enhancing investment strategies

AI-driven tools will allow DFMs to offer more sophisticated strategies – like Active ETFs or Direct Indexing – at a fraction of the cost of traditional active funds. They will also allow the development of personalised model portfolios, with each client potentially getting a unique asset allocation to meet their direct needs, with “personalised” management of the portfolio as AI facilitates individual adjustments to portfolios rather than the need for “global” switches across portfolios to be made.

The “advice alpha” premium

While AI lowers the cost of the investment component, it increases the value of the advice component. Not only are planners freed up to focus more fully on the client and their advice and behavioural needs, but those planners who use DFMs powered by AI are likely to be able service more clients without necessarily increasing headcount or operational costs.

AI requires investment

While the benefits of AI like automation and seamless scanning of data will reduce costs, the initial investment in AI systems (eg training, integration, vendor solutions) can be significant. In addition to this, the regulator is very clear that AI always needs human oversight, so the need to have skilled humans both in DFMs and financial planning businesses is not going to disappear.

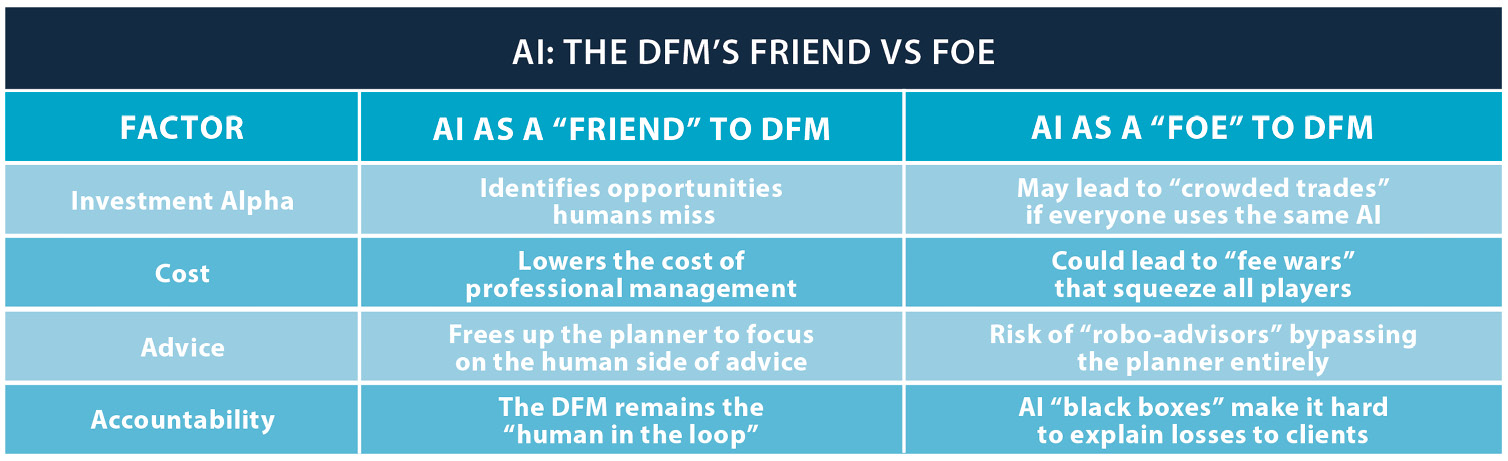

C. As the sophistication of AI develops, how much of a threat is it that financial planners will use AI to replace DFMs?

As AI becomes more sophisticated, a critical question arises:

Will planners eventually use AI to cut out the DFM? Or vice versa? No doubt there are financial planners using DFMs who are calculating the cost savings that this would bring, both to their clients and themselves. And financial planners who don’t use DFMs may be thinking that they won’t ever need to go down that route thanks to AI.

The extent to which AI poses a threat to the DFM/planner relationship will be informed by some key considerations.

Investment accountability is human

While a planner could use an AI tool to pick funds and construct portfolios, they cannot use AI to carry the Category II legal liability. The FSCA’s stance is clear that there must be human oversight for all discretionary decisions. A DFM provides the regulated human oversight that an AI tool cannot. Whether financial planners see this as an opportunity to get a Cat II licence themselves so that they can be the human oversight remains to be seen.

The “black box” risk

The risks of blindly using AI are well documented. AI tools are known to “hallucinate”, to simply get things wrong and are often at the mercy of the instructions they are given. If something goes wrong with an internal “DFM” that is purely an AI tool, for example an algorithm fails, a planner using their own AI has no-one to hold accountable. By using a DFM, the planner has a professional entity to hold responsible for the investment process and outcomes.

The “cyborg” advantage

The future is unlikely to be simply AI vs human. At this stage it seems likely that the most powerful combination will be the human plus their AI team. Until AI has proven itself to be on a par with or better than humans in all aspects of financial planning and investment management, it is likely that the most effective partnership will be between a DFM that uses AI for the heavy data lifting, automation of processes, robust implementation of portfolios and potential generation of insights about client behaviour; and a financial planner who uses those insights and is freed up by the DFM’s automation to focus on having empathetic holistic financial planning conversations with clients.