The issue of investment performance is a vexed one when it comes to DFMs. By taking over the responsibility of managing client investments on a discretionary basis, DFMs are hanging their hat on the hook of investment performance. This “frees up” financial planners from direct responsibility for their clients’ investments and enables them to pay more attention to their clients’ behaviour around their investments, arguably a more difficult and more important task.

Much research shows that ultimately the returns that clients gain from their investments has less to do with how and where the money is invested and more to do with their behaviour – left unchecked, many clients buy and sell investments at the wrong time, influenced by various factors ranging from fear to FOMO and a little bit of greed thrown in for good measure. But when we consider how to assess a DFM’s performance, it is important to clarify what we mean by performance. A mistake that most investors and unfortunately many financial planners make is the belief that investing is a competition. This belief is fed by the financial media with the publication of performance tables of asset managers and the various awards that asset managers can “win” for the performance.

The supposedly competitive nature of investing is exacerbated by social media where commentary on “investments” and their performance, by experts and non-experts alike, is a daily occurrence, if not an hourly one. One of the benefits of using a DFM is that clients and financial planners are distanced from the noise around the latest high-returning investment, be it gold, silver or crypto; as well as distanced from the incessant performance beauty parade of asset managers which invariably influences both financial planners and their clients to make the wrong decision at the wrong time.

Despite this “distancing” serving as an important role for DFMs, there are many investors, financial planners and commentators in the media who believe that DFMs should also be included in performance tables, just like asset managers.

The problem with this is twofold. Firstly, it ignores all the other benefits that financial planners and their clients derive from using a DFM such as operational, administrative and compliance efficiencies for financial planners; and very clearly defined and implemented investment strategies for clients, with all the attenuated benefits of expertise and scale that comes with a DFM service.

Secondly, the desire to compare the performance of different DFMs presumes that there are like-for-like comparisons that can be made. The reality is that most DFMs manage bespoke portfolios as well as standard portfolios. It is very difficult to compare bespoke portfolios across DFMs because mandates may be very different, meaning asset allocations and fund selections will vary widely. With respect to standard portfolios, even here there will be variation between DFMs as to what we mean by “standard”.

Some DFMs may have “outcome” focused portfolios, eg targeting particular returns above inflation; while other DFMs may have investment “input” focused portfolios, eg committing to a certain percentage allocation per asset class – some portfolios may be deemed “high-equity” because they have committed to a minimum equity exposure of 70%, while others may be “low-equity” with a maximum of 30% equity exposure. The difficulty in comparing DFM performance does not mean that investment performance is not a critical aspect of a DFM’s value proposition. The question is, what performance should a financial planner want to assess? Or to put it another way, what investment outcomes should a financial planner focus on?

Given that investing is not a competition, and is very much a means to an end, enabling clients to achieve goals for their life using their money, the only performance worth worrying about is whether the DFM is achieving the targeted outcomes for each model portfolio – standard or bespoke – within the parameters of the investment mandate. For example, if a model portfolio aims to achieve an inflation-plus-3 return over rolling three years, then those are the two key performance parameters that need to be assessed. Because any client invested in such a portfolio will have had their need or needs assessed by the financial planner to deem such a portfolio appropriate.

The real power of the DFM proposition is that financial planners are freed up to thoroughly assess a client’s needs and goals, with a ready-made solution (the relevant model portfolio) on hand to serve as the means to achieving those goals. With client outcomes as the primary investment metric to assess, financial planners can also conduct ongoing due diligence of DFMs to ensure that the investment outcomes of the model portfolios are aligned with the components of the model portfolio. In order to conduct this due diligence, financial planners may wish to consider the following questions:

A. How can you validate the performance of a DFM?

Whether you are considering using a DFM, or already do so, validating the performance of the DFM periodically is an important part of the due diligence process. But validating a DFM’s track record can be difficult because DFM models are spread across different platforms (LISPs) with potentially different cost impacts and will have different “entry points” for different clients. But financial planners can assess the constituent parts of a model portfolio – each component CIS fund’s track record can be reviewed and these can be aggregated to determine to what extent a certain model portfolio’s performance is in line with the expectations based on the performance of the underlying funds.

Another way to validate performance is where a DFM has unit trusts that it manages and which mirror its model portfolios, planners can use the fund fact sheets of these unit trusts as a proxy for the portfolio’s performance and the DFM’s investment skill.

Financial planners could also get independent third-party verification of DFM performance. This ensures the returns shown in marketing “pitches” are mathematically accurate and net of all underlying manager fees.

B. To what extent should financial planners worry about risk-adjusted returns vs absolute and relative returns?

Given that investing is not a competition, in a financial planning context, “beating the market” or “beating other investments” (relative return) is less important than “meeting the goal” (absolute return) without unnecessary volatility (risk-adjusted return).

Volatility may be necessary in some portfolios which are targeting higher returns, but financial planners may wish to assess the volatility of portfolios used in a living annuity for example, where clients are taking a regular income from the portfolio and big market or performance “drawdowns” could impact the sustainability of the portfolio.

To ensure alignment between a client’s financial plan and their investments, ideally model portfolios will target “absolute returns” such as a CPI+ targets over rolling periods, which enables the financial planning and the investments to be in sync.

While the performance of the underlying component funds of a model portfolio may be assessed on a relative basis – whether to their asset class benchmark or peers – the relative performance of a DFM should not be the focus for a financial planner who prioritises financial planning to achieve identified client outcomes through the use of model portfolios.

C. How much attribution analysis is done to assess the DFM’s impact on performance vs the underlying fund managers?

Attribution analysis can be likened to the “MRI” of investment performance – it shows exactly where the returns in a portfolio come from. It is a critical exercise that serves as part of a financial planner’s ongoing due diligence process.

There are probably three key areas in which a DFM can add value to a portfolio and that a financial planner should consider as part of an attribution analysis:

Asset allocation – Was value added by tactical asset allocation (TAA) decisions the DFM made? Ideally financial planners should ask for at least a quarterly report showing whether their TAA decisions versus the portfolio’s strategic asset allocation (SAA) added or detracted value during the quarter. If, for example, the underlying fund managers are doing all the heavy lifting and the DFM’s asset allocation is detracting from performance, the DFM fee is harder to justify.

Fund selection – To what extent did the choice of funds in the portfolio add or detract value over the period? In order to assess underlying fund performance, it is appropriate to use relative benchmarks, whether they are asset class returns or peer returns.

Cash-flow management – To what extent did the DFM’s management of inflows and outflows from investors impede or enhance the performance of the portfolio?

A robust attribution analysis process can help financial planners assess where the DFM is adding any “alpha” to the portfolios, but most importantly it is a way of assessing the process that DFM follows in selecting funds, doing asset allocation and managing the flow of money.

This focus on the DFM’s process is critical, as not only is process a key predictor of future performance, but it is also a means to assess whether the DFM actually does what it says it does.

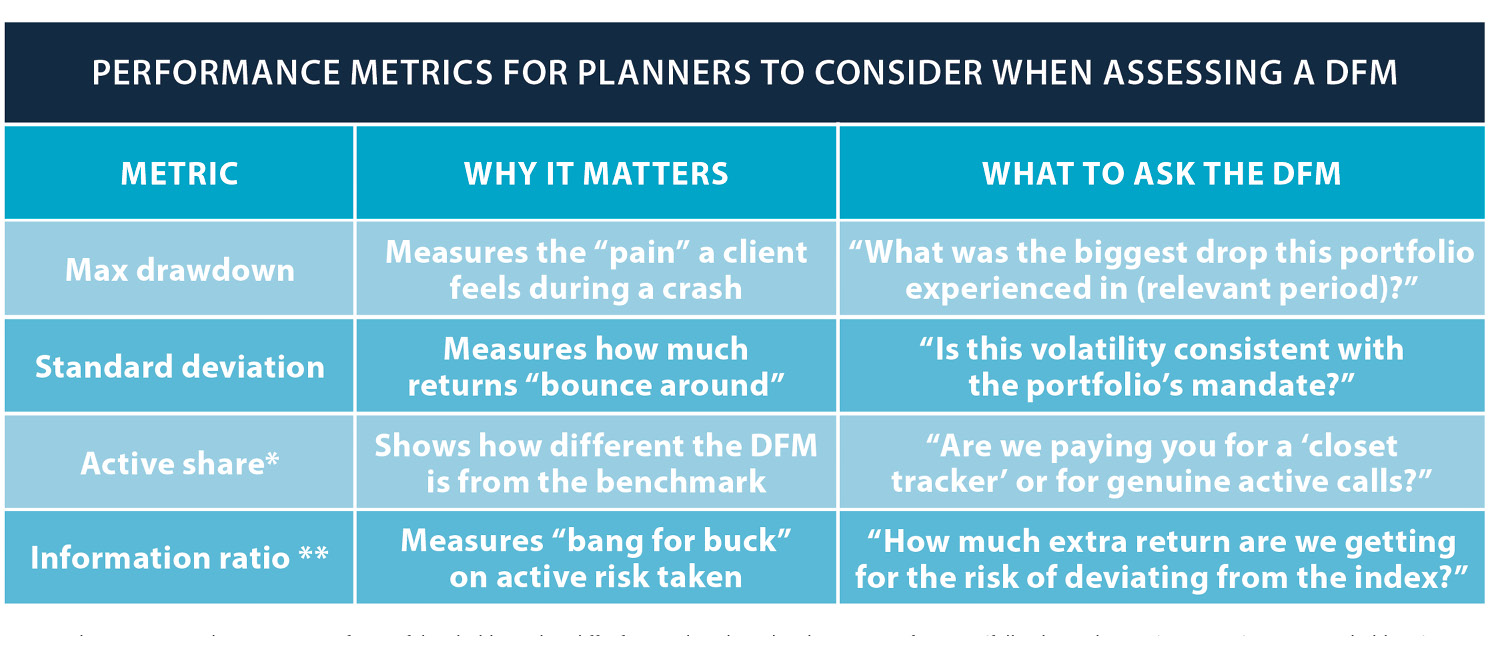

*Active share measures the percentage of a portfolio’s holdings that differ from its benchmark index, ranging from 0% (full index replication) to 100% (no common holdings).

** Information ratio (IR) is a performance metric measuring an investment manager’s ability to generate excess returns relative to a benchmark, divided by the volatility

of those returns (tracking error). It evaluates consistency in beating a benchmark, with a higher ratio indicating superior risk-adjusted active management.