and Sandeep Jaggi (Analyst Emerging Markets Debt & Commodities, Schroders)")

The climatic effect known as El Niño – a natural periodic warming of the Pacific Ocean – is threatening to increase global temperatures in coming months and drive extreme weather.

It is predicted to arrive between June and August, according to estimates by the World Meteorological Organisation, with a 90% probability of persisting to November. “We need to prepare for a potentially strong El Niño event which will exacerbate drought and heavy rainfall and increase the risk of heatwaves,” the WMO warned*.

El Niño can impact the global economy in many ways, with past episodes disrupting water levels in the Panama Canal, curbing hydroelectric power generation, and triggering unseasonal floods and droughts around the world. Such effects would impact food production.

Rolling waves of commodity price-driven inflation raise the risk of price pressures becoming ingrained, and would coincide with other adverse economic and geopolitical factors. It could result in a further populist lurch, particularly in Europe, ahead of key elections across the continent.

The link between El Niño and food price inflation

Our previous research shows that there is not a strong, direct link between measures of El Niño (and La Niña, which is the name given to the opposite cooling phenomenon) and agricultural prices.

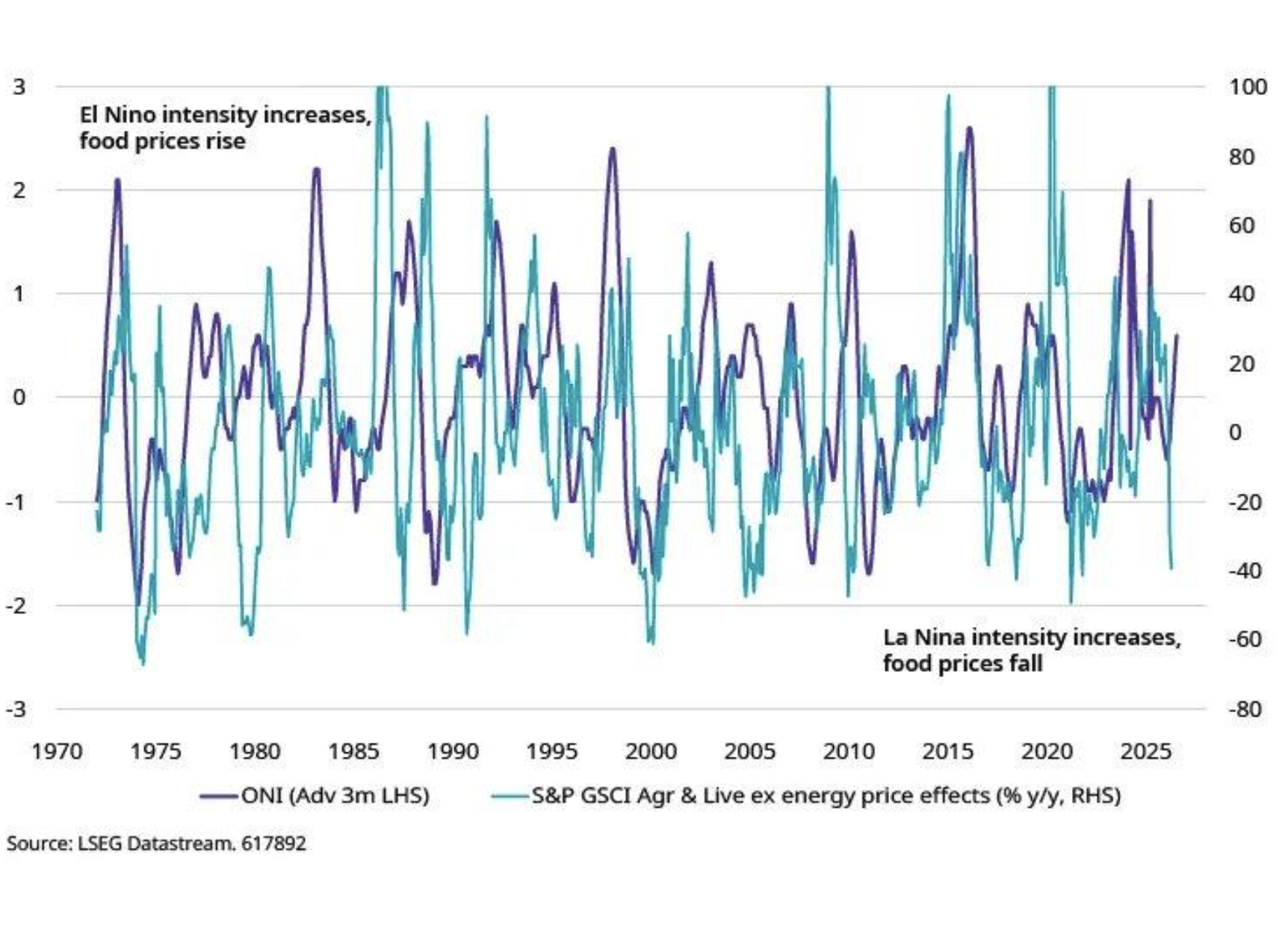

The Oceanic Niño Index (ONI) tracks deviations in Pacific sea surface temperatures from average levels and is the main benchmark for gauging the strength of El Niño and La Niña events. However, our work also shows that the correlation is improved markedly if the effects of energy prices are stripped out of global food indices. After all, there has historically been a close relationship between food and energy prices due to the impact of transportation costs and the energy-intensive production of fertilisers.

Figure 1: A rising Oceanic Niño Index usually results in higher global food prices

If past correlations were to hold, then a very strong El Niño would imply a doubling of global food prices from current levels over the next year or so.

Of course, none of these relationships are ever perfect. Indeed, our analysis of ONI ultimately overstated the impact of El Niño on food prices in 2023, highlighting the difficulty in forecasting both the weather and crop yields.

Fertiliser shortages and demand for biofuel adds to El Niño’s likely impact on food production

This time around, the threat of a powerful El Niño comes on top of other factors that already suggest that food prices ought to rise in the months ahead.

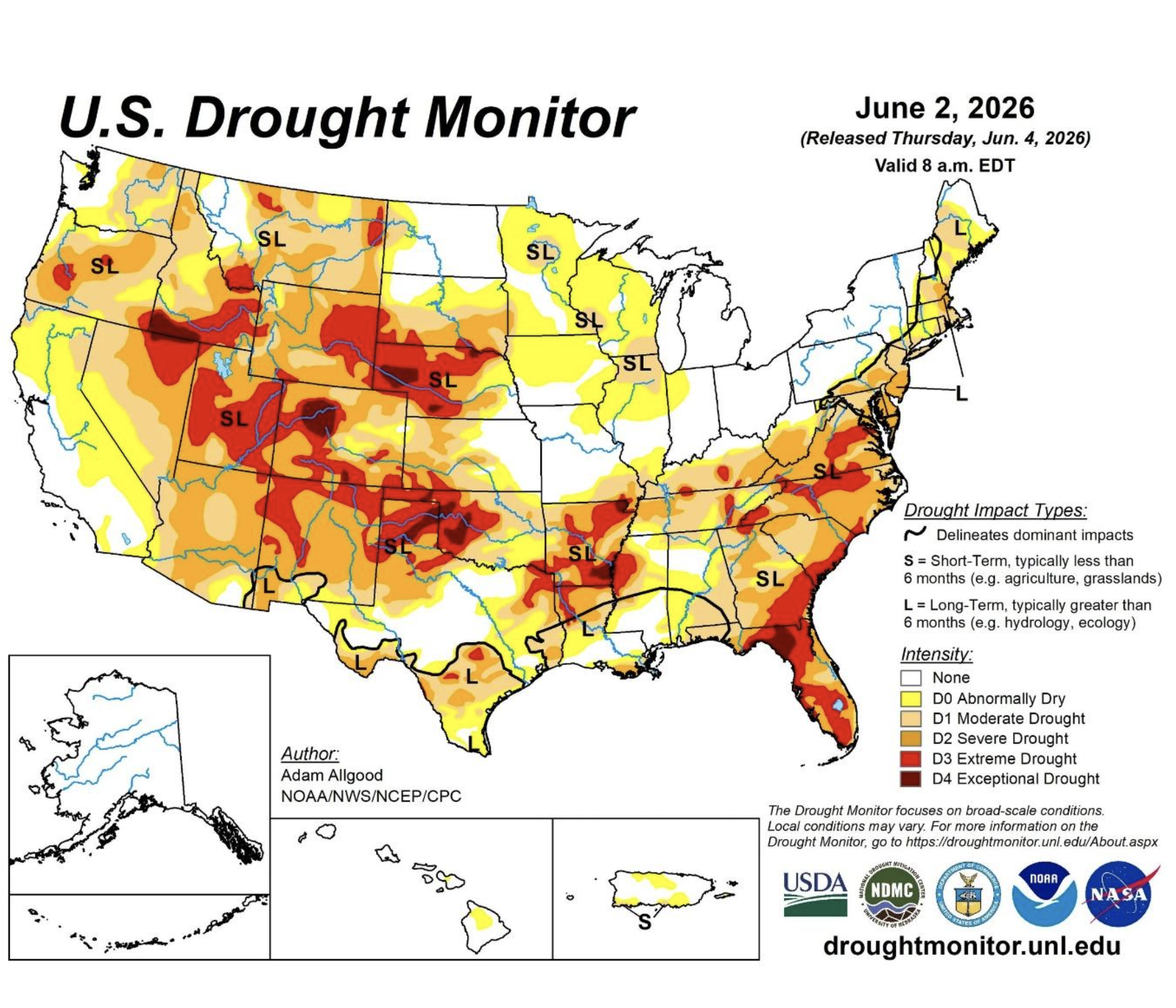

First, we are already seeing extreme global temperatures this year. As of early June, over 50% of the US was in drought, with around 250 million acres of crops affected. And extreme temperatures are not confined to the US. A record-busting heatwave swept across the European continent in May, while parts of India have seen temperatures soar above 40°C.

Figure 2: The US suffered severe drought during spring 2026

The US Drought Monitor is jointly produced by the National Drought Mitigation Center at the University of Nebraska-Lincoln, the United States Department of Agriculture, the National Oceanic and Atmospheric Administration and the National Aeronautics and Space Administration. Map courtesy of NDMC.

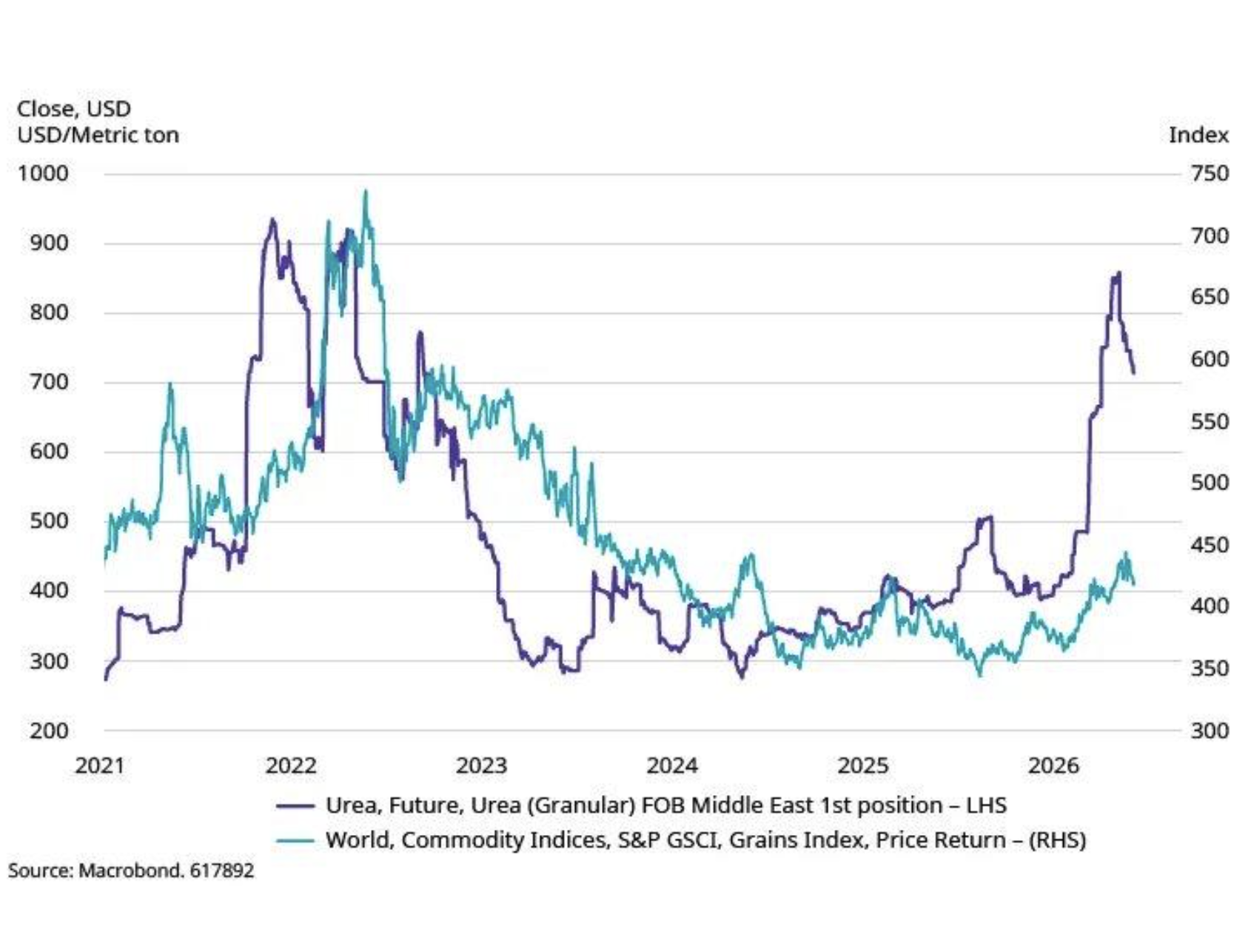

Second, while much of the attention has been on the disruption to energy supplies, the closure of the Strait of Hormuz has also had a devastating impact on the global supply of fertilisers. About a third of global urea originates from the region and is shipped through the Strait. Urea prices have doubled since the conflict began and imply a sharp increase in the price of some food groups.

Figure 3: Spike in fertiliser prices points to much higher prices for grains

The risk to agriculture production is most acute where fertiliser stocks were not secured ahead of the conflict, and for crops with high nutrient requirements that enter their key crop development phases when El Niño intensity peaks. The confluence of these risk factors is most clearly visible for rice, wheat, sugar and cocoa.

El Niño typically brings weaker monsoon rains and above-normal heat to South Asia growing areas, while West Africa faces the risk of drier conditions and stronger Harmattan winds, impacting cocoa production. In wheat, Australian planted area is expected to fall sharply, with production potentially down by around 9 million tonnes in 2026/27.

Sugar looks especially exposed. Previous El Niño events have seen production in India and Thailand fall by 20-30%, pushing major producers towards net imports and driving prices much higher. The impact could be more pronounced this time because a greater share of sugar stockpiles is being diverted into ethanol production. Biofuel demand is being reinforced by the Middle East oil shock, increasing usage of sugar, corn and soybean oils. Food prices have begun to rise, suggesting the squeeze on fertiliser supplies is starting to trickle down to prices, and the impact could be compounded by more difficult growing conditions.

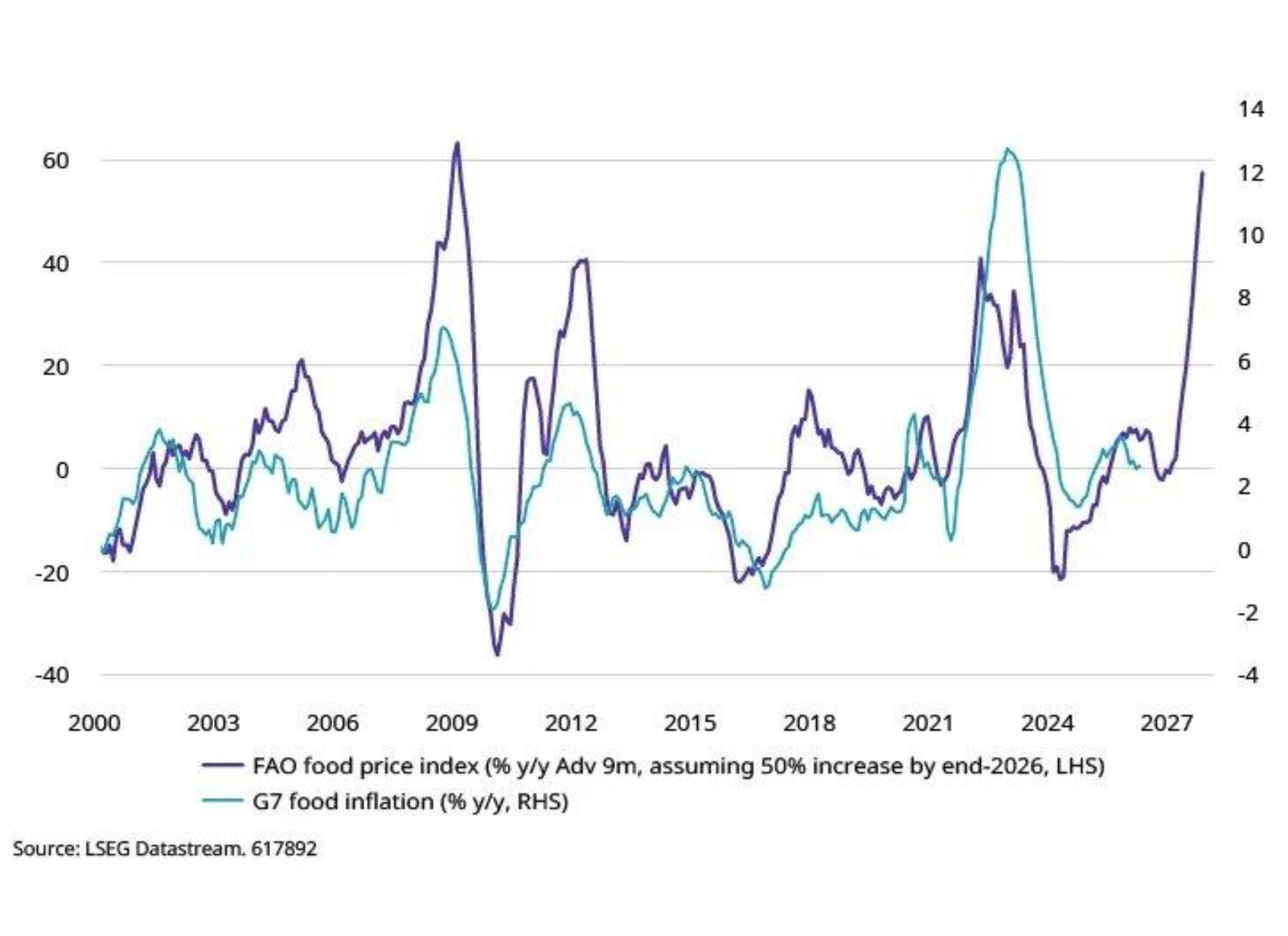

All of this could add to the stagflationary tilt that we are already seeing in the global economy as higher energy prices pass through to consumers. For example, if this confluence of factors caused the UN FAO food price index to rise 50% by year-end, the usual lags mean G7 food inflation would probably hit double digits in 2027 – enough to add over a percentage point to headline inflation.

Figure 4: A wave of food inflation could hit the global economy just as the energy price shock subsides

While the importance of food to consumer price baskets varies across different markets – ranging from only 10-15% in developed markets to 25% and more in emerging markets – a wave of food inflation, coming just as the current energy inflation shock subsides, would keep pressure on real incomes and dampen consumption for longer.

Rolling waves of inflation, rather than a more immediate, one-off shock increase the risk of adverse outcomes. One is that the longer inflation remains elevated, the greater the chance of second-round effects on wages that could see price pressures become ingrained.

*Source: WMO, Prepare for El Niño 2026

Credit: Schroders

![]() Important Information

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Investment involves risk.

This information is a marketing communication. The information contained herein is believed to be reliable. Where third-party data is referenced, it remains subject to the rights of the respective provider and must not be reproduced or used without prior consent.

Any data has been sourced by us and is provided without any warranties of any kind. It should be independently verified before further publication or use. Third party data is owned or licenced by the data provider and may not be reproduced, extracted or used for any other purpose without the data provider’s consent. Neither we, nor the data provider, will have any liability in connection with the third party data.

The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Any references to securities, sectors, regions and/or countries are for illustrative purposes only.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any investments to rise or fall. Schroders has expressed its own views and opinions in this document, and these may change.

This document may contain “forward-looking” information, such as forecasts or projections. Any forecasts stated in this document are not guaranteed and are provided for information purposes only.

Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at https://www.schroders.com/en-za/za/intermediary/footer/privacy-policy/ or on request should you not have access to this webpage.

For your security, communications may be recorded or monitored.

Issued in June 2026 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998.