Economic forecasting can be a thankless task, and the latest round of revisions to our expectations for China came with a large portion of humble pie. We previously expected GDP growth of 6.5% this year to beat consensus expectations. A marked deterioration in the recent incoming data, and lack of urgency from the government to stimulate activity has subsequently forced us to cut our projection to just 4.8%.

The premise of our relatively upbeat view had been that China’s economy would enjoy a “sugar high” of stronger growth, as the relaxation of the zero-Covid policy led to a burst of activity in transport related services. While the absence of large, excess household savings meant we did not expect this to last more than two or three quarters, we nonetheless expected it to be sufficient to drive solid full-year growth.

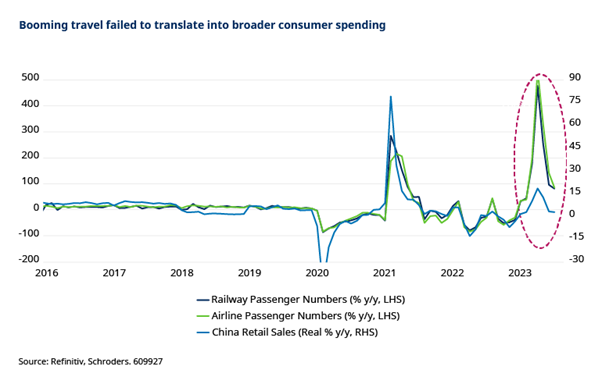

Transport-related services did see an astonishing pick-up in activity. For example, railway and airline passenger numbers, which had previously been a decent guide to consumer spending, were up by 500% year-on-year in April. But as the chart below shows, the acceleration in retail sales was nowhere near the scale implied by passenger numbers.

One reason for the apparent reluctance to spend appears to be weak consumer confidence. While the zero-Covid policy has been removed, it appears to have left its mark on the economy through scarring that has had a negative impact on the labour market. Lingering concerns about further, unexpected disruptions or lockdown may have also dented confidence. Consumer confidence ought to improve over time, but it may not happen quickly.

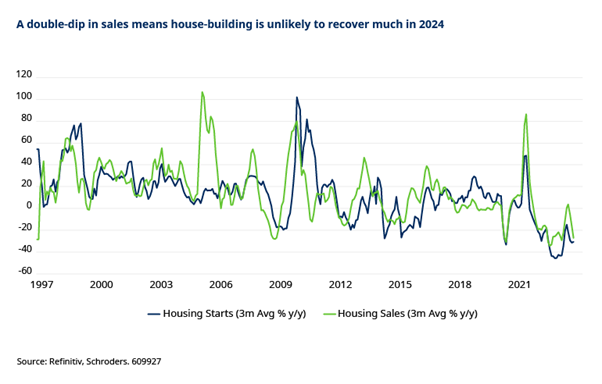

A major dampener for confidence is the ongoing problems in the real estate market. Our base case earlier this year was that a stabilisation in house purchases would set the scene for a slight recovery in construction activity as we headed in 2024. As the chart below shows, while our view had initially appeared to be on track, there was also a renewed slump in house sales from April onwards.

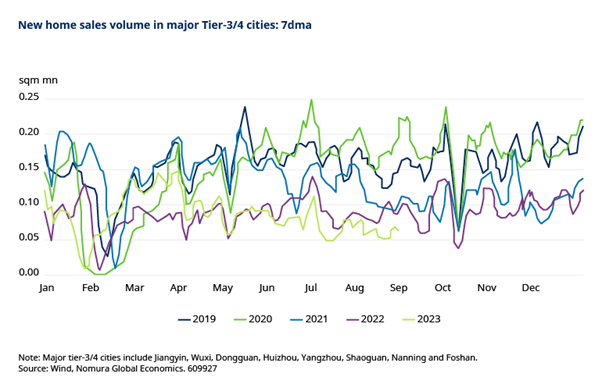

Part of the problems in the housing market are likely to be a manifestation of the generally poor consumer confidence noted above. However, it is clear that the housing market is also undergoing a structural shift away from speculative demand that had threatened to create systemic financial risks in the economy. Data on the housing market are patchy. By piecing together various sources, however, it becomes clear that a significant portion of strong house sales in lower tier cities in recent years were driven by speculative demand.

Population growth was largely stagnant, there was an increasing prevalence of purchases by individuals with at least one property and a growing number of empty units. After a burst of sales as the economy reopened, transactions have settled back to similar levels seen in 2022.

These are around a quarter of volumes seen prior to the housing clampdown and might suggest that about three quarters of past demand for housing in lower tier cities was speculative and unlikely to return.

Problems in the housing market are likely to have several consequences for the broader economy. First, depressed sales revenues will continue to add to the liquidity crunch amongst real estate developers. Pressure on top lines is occurring at a time when firms have less access to capital markets and are expected to complete pre-sold projects. Country Garden is the latest major developer to run into trouble. Regardless of whether default is averted, negative headlines about housebuilders are likely to be the norm going forward with knock-on effect to wealth management firms. This is likely to reinforce negative sentiment.

Second, with at least some of the speculate demand that drove real estate sales likely to be permanently lost housing will contribute less to economic growth. Remember, this driver of demand is being removed just at a time when the population is set to decline. Many estimates put housing at around 25% of GDP, meaning that weaker activity could knock a substantial amount off trend growth, perhaps lowering it to 3-4%. It can be argued that moving away from meeting lofty growth targets with unsustainable growth drivers is a positive development for the long term outlook. It is, however, clearly not helpful for top-line growth in the meantime.

Third, and more immediately, all of this weakens a key transmission mechanism for policy support to boost activity. Historically, looser policy has led to households taking out loans to purchase property, stimulating construction activity while also following through with purchases of white goods, furniture and other related items. But with interbank rates way below policy rates and falling again, due to the financial system being awash with liquidity, there is clearly a plumbing problem with getting money out into the real economy. The authorities have in recent days finally announced concrete support measures for housing demand, with the size of deposits and mortgage rates lowered including for purchases of second homes in higher tier cities. This will have some positive impact, but is unlikely to be as potent as in the past.

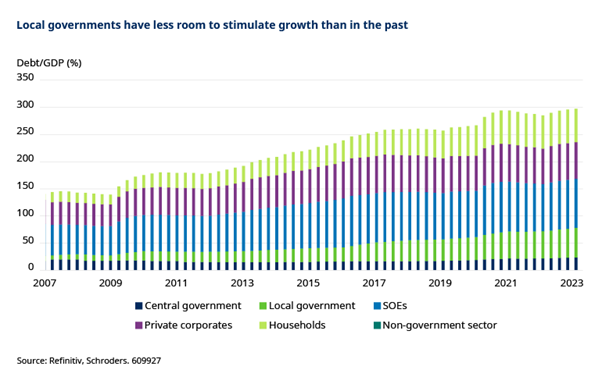

Some impetus should come from local government infrastructure projects, but this transmission mechanism of policy support to the real economy is also likely to have weakened. Local government debt has risen over the past decade as its roll in delivering counter-cyclical stimulus through infrastructure spending has increased in the face of a structural slowdown in growth. Some reports indicate that debt is much higher (perhaps double) once off-balance sheet obligations are taken into account.

Like real estate developers, local governments have felt the pinch in recent years. This has occurred as they have faced high bills from Covid policies at a time when problems in the housing market have caused crucial revenues from land sales have dried up. Bond issuance is being front-loaded to finance infrastructure projects. However, at least some of the proceeds are likely to disappear into servicing other obligations. And with the central government showing no urgency to intervene or deliver major stimulus itself, such fiscal stimulus may be less effective in the near term.

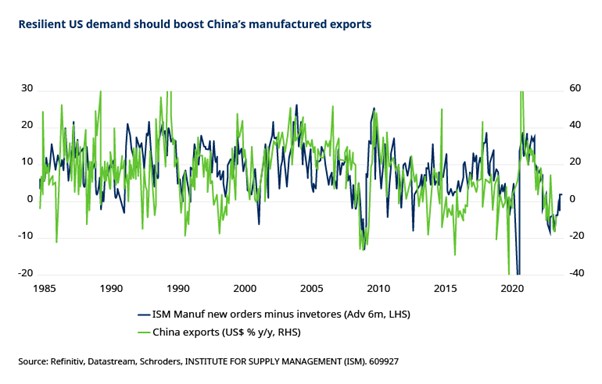

We continue to think that China’s manufacturing and export sectors will benefit from some upturn in the global goods cycle in the months ahead. Leading indicators show tentative signs that the global manufacturing PMI will rise into expansion territory later this year. Meanwhile, upgrades to our US growth projections imply resilient demand and some restocking even if decoupling may weaken the pass-through to some degree.

Nonetheless, it seems that China will be driving with the handbrake on and we do not anticipate a strong rebound in growth next year. Indeed, while we have cut our forecast for growth this year from 6.5% to 4.8%, we have only marginally increased our projection for 2024 to 4.5% from 4.3% previously.

Softer growth, weak demand for credit due to the structural change in the housing market and a negative CPI have done nothing to dispel concerns about a debt/deflation spiral. We have lowered our inflation forecasts, but the current decline in prices is deflation in name only and due in large part to commodity prices. These effects should fade in the months ahead and see headline inflation return to positive territory in 2024, averaging in the region of 1.8%.

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy.

Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of investments to fall as well as rise.

The views and opinions contained herein are those of the individuals to whom they are attributed and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy.

Issued in August 2023 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998