What is the backdrop?

Following a sustained period of underperformance, MSCI Emerging Markets began to outperform MSCI World from January 2025. While performance was initially broad-based and supported by US dollar depreciation, performance has become increasingly driven by one factor: AI. EM IT is dominated by the tech supply chain, which is a direct beneficiary of rising AI capex.

Hyperscaler capex is flowing to EM, driving strong absolute and relative performance in return on equity (ROE) and US-dollar earnings. Earnings growth is sufficiently powerful in Korea to suppress multiple expansion, despite very strong stock performance.

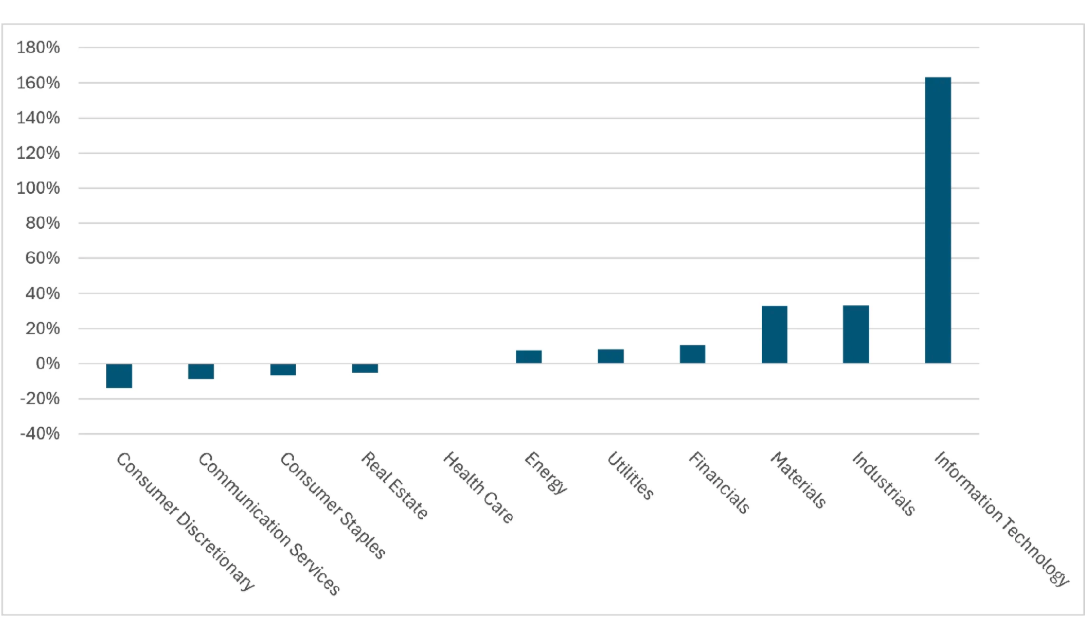

Market leadership has become increasingly narrow, with significant dispersion between sectors. The AI thematic has driven tech hardware, along with associated industries such as electrification and commodities. Many other parts of the market have lagged.

Figure 1: The outperformance has been driven by a few sectors benefiting from AI

MSCI EM sector performance for 12 months through the end of June 2026

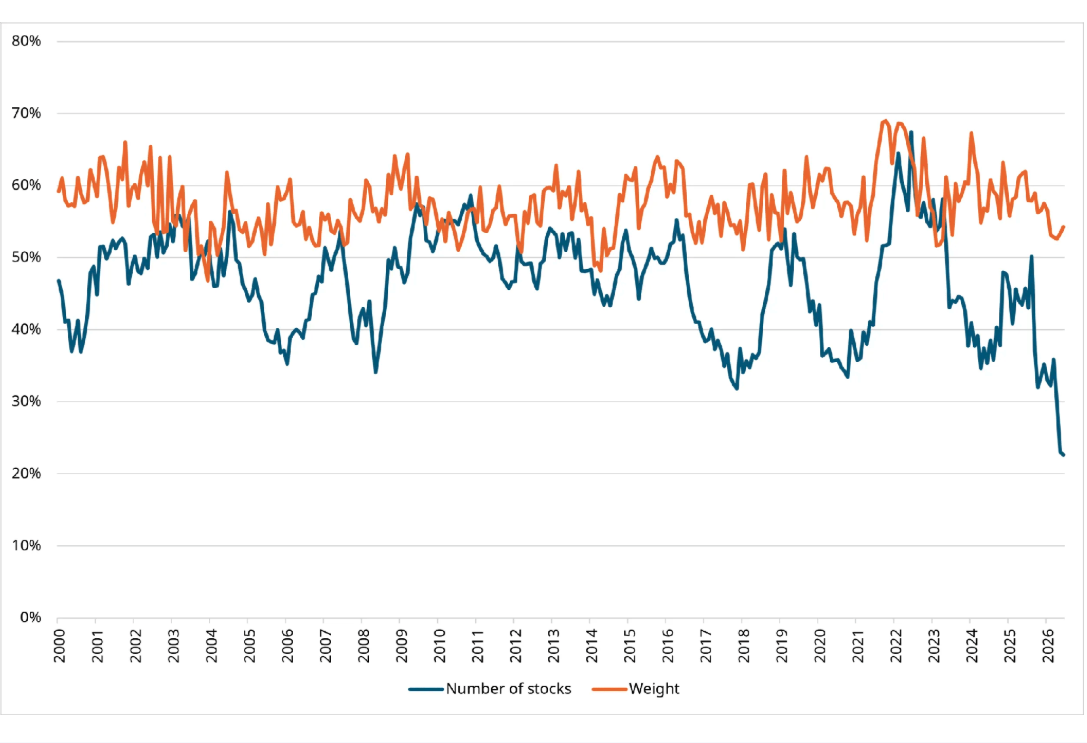

Meanwhile, the percentage of stocks outperforming the benchmark has fallen to a record low.

Figure 2: The percentage of EM stocks outperforming the index has fallen to a record low

% of stocks and % weight of stocks in MSCI EM Index outperforming on a 12-month rolling basis

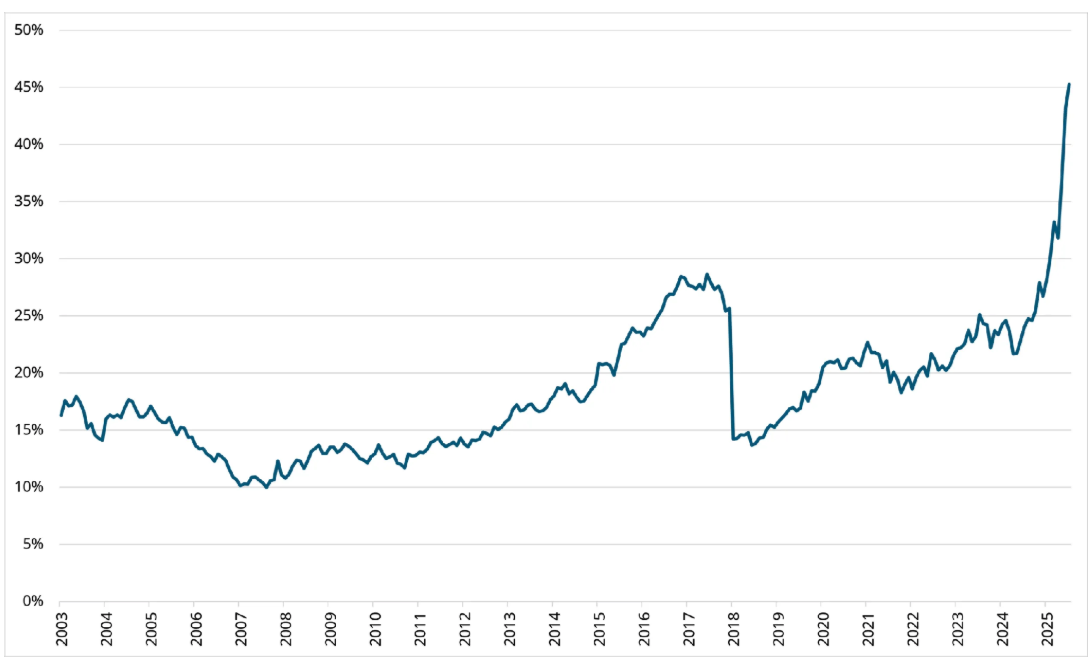

IT is now over 40% of the MSCI EM benchmark. This is markedly higher than in other regional benchmarks. The top three stocks — TSMC, Samsung Electronics and SK Hynix — are now over 30% of the benchmark. The weights of tech-heavy markets Taiwan and Korea have risen to surpass China. EM beta has become increasingly linked to the performance of the AI thematic.

Figure 3: Weight of information technology in the MSCI EM Index

To what extent is EM vulnerable to an AI-led correction?

Current IT sector profitability is very strong. A dramatic expansion in demand has met capacity limitations across the supply chain. Suppliers have seen a combination of expansion in their addressable market, revenue growth, a positive mix shift to higher-margin products, pricing power and operating leverage, all of which are driving ROE and earnings expansion.

However, while this current cycle is very strong, there is little reason to believe that the AI investment cycle will ultimately behave differently from previous capital-intensive industry cycles. High returns incentivise capacity expansion, supply catches up with demand, returns normalise and valuations come under pressure. And the margin of safety has diminished. While IT is currently seeing very powerful earnings momentum, valuations and expectations have lifted markedly.

This makes future performance dependent on cycle duration and strength. If the cycle extends, we see potential for ongoing positive earnings revisions, especially if demand growth continues to outstrip supply. But cycle duration is likely to be heavily influenced by the path of future demand, which, in a period of significant structural change, carries high forecast risk.

This makes it important to regularly reconfirm the top-down view and to stay disciplined, managing exposure to sector, sub-industry and stock.

How has our top-down view evolved?

Over the course of 2026, our top-down conviction has grown. We believe that AI is in the early stage of S-curve adoption and that the productivity opportunity will be sufficient to cover a significant increase in enterprise spend on compute.

Model capability has surprised positively, enhancing commercial use cases. Businesses are pushing on integration and automation and evaluating how AI can be used to improve productivity and outcomes. This is driving surging inference demand, leading to a shortage of compute.

Hyperscalers have recently seen pricing power and revenue is growing rapidly, which should reinforce funding and capex commitments. We believe that fundamentals point to a further increase in capex through 2028.

We see ongoing tightness across the tech supply chain. We think investors stand to benefit from having exposure to foundries, packaging and testing, CCLs (copper clad laminates), Ajinomoto Build-up Film (ABF) substrates, power supply and thermal cooling, memory, memory interface, printed circuit boards (PCBs) and original design manufacturers (ODMs).

Consumer monetisation may take longer than enterprise. However, we can envisage scenarios in which consumers may ultimately pay to access superior models, while model companies may control traffic and user engagement, leading to a reallocation of margin away from incumbent platform and software companies.

Hyperscaler and cloud profitability matters to the extent that it impacts funding for capex. While hyperscalers may not yet deliver returns above cost of capital on their cloud capex, cloud revenue growth is accelerating off a high base. Furthermore, AI’s growing capabilities should bring enormous power to those that control it, while its ability to disrupt existing business models and to cannibalise parts of the labour market may bring huge economic opportunity.

We don’t find it surprising that CEOs would sacrifice returns and short-term stock performance to avoid falling out of the pack.

What is required to justify the level of spend?

Estimates vary, but AI capex could run around $1 trillion in 2026 with significant growth expected in 2027 and 2028. Nvidia’s Jensen Huang has guided to $3-4 trillion of annual AI infrastructure capex by 2030, the low end of which would be very supportive of tech hardware revenue growth.

Cumulative capex by 2030 might require over $5 trillion in annual customer value to satisfy corporate return hurdles across the chain. These figures may be seen in the context of 2026 global GDP projected at $126 trillion (IMF World Economic Outlook, April 2026) and estimated all-corporate operating profit of around $30 trillion in 2026.

AI has the potential to substitute labour and disrupt existing business models – the addressable market could be vast. AI should also, in theory, increase economic capacity. However, the required revenue that would deliver a fair return on all capex is commensurately large.

It would be naïve not to anticipate over-investment and value destruction in parts of the AI value chain at some point, given the scale of investment, the motivations for investment, the difficulty in forecasting demand, unproven business models, and varying supply responses across different sub-industries.

Industry cycles by their nature involve periods of supply / demand disequilibrium. However, while investors need to consider the cycle in its totality, expectations regarding cycle duration and the scope for further positive revisions will continue to shape allocation and risk management decisions as the cycle proceeds.

xposure to supply chain companies, with medium-term global opportunity.

What could drive a correction?

We are already seeing volatility, and any bull market will face periods of consolidation. It is more important to gauge whether we will see a more marked and sustained drawdown, whose risk or occurrence might drive us to change our views more markedly. We are most conscious of the following risks:

- A period of digestion on corporate AI integration. Productivity may lag rising spend on compute.

- Funding becomes a problem. This could be driven by broader market issues, or by concerns regarding the timing and extent of monetisation, which could contribute to the failure of certain IPOs. This issue is more likely to relate to frontier labs given that hyperscalers’ balance sheets are robust with significant ongoing cash flow generation.

- Bottlenecks such as power availability constrain capex irrespective of funding or intent.

- AI may significantly increase economic capacity. But we may see political reaction, regulation and the introduction of excess profit taxes, especially if AI is highly disruptive to labour markets, driving greater job insecurity, higher precautionary savings and weaker consumption.

- Momentum fails. Markets trade on expectations as much as outcomes. Capex could sustain at a high level, but capex growth could slow or cease to surprise positively, and earnings revisions get harder or even move negative. Supply has room to catch up. The sector de-rates.

- Rapid growth in model efficiency and model commoditisation. Model companies monetise at the frontier. Frontier model advances may slow, model distillation will cheapen access, lagging models may be sufficient to serve many tasks. We do not expect an end to model scaling laws in the near term and there is no diminution of effort on frontier model development, whose training is relevant to compute (model companies have even noted the potential for self-solving models to accelerate improvements). We believe in Jevons paradox. Lower token cost will drive usage, which drives inference, which will support hardware demand. Ongoing rapid growth in compute or component efficiency may similarly be disruptive at certain times (e.g. significant gains in efficiency of memory usage as memory supply comes online). But for hyperscalers, hardware efficiency gains can offset price hikes, while lower compute costs can support demand.

- Chinese model and cloud pricing undercuts Western companies. Chinese industrial policy when allied to geostrategic considerations typically crushes returns in that industry. But security may be a concern for certain Western companies even if Chinese companies are providing open-source models. Open source may move to open weight, which would lift security considerations. Western governments may seek to ringfence against Chinese models if their growing capability or use is considered a risk to national security.

What about the bottom up?

Both allocation and selection are important sources of alpha generation. At this stage of the cycle, understanding relative tightness across different parts of the supply chain, barriers to entry, and competitive positioning within sub-industries becomes increasingly important. Investors typically need to be increasingly selective.

Taiwanese forward earnings multiples are above historic peaks at a time when earnings are cyclically advanced. Korean memory multiples remain low, but this reflects a very strong earnings cycle heavily led by price increases. Forecast risk is high. Demand remains very strong, but capacity is responding, and some parts of the supply chain are more fragmented and commoditised. Slowing earnings growth may be a headwind for momentum. Performance from here relies on confirmation that 2028 will be another year of growth. If companies are over-earning, the expected duration of that over-earning is also highly relevant.

Meanwhile there are emerging signs of speculative behaviour: retail participation has risen, partly driven by margin financing and levered exchange-traded funds (ETFs), both of which amplify volatility.

How do we approach tech allocations?

Technology has always been a cyclical sector, and underlying technologies can evolve rapidly. We are in an unusually powerful cycle with high forecast risk, and cycle strength and duration can have a marked impact on earnings expectations and valuations.

Valuations have appeared demanding for some time, yet earnings have continued to surprise positively. Investors who relied solely on valuation metrics would likely have reduced exposure much earlier in the cycle, potentially at a significant opportunity cost. In our view, successful technology investing requires a more holistic framework.

Accordingly, we recommend that investors:

- Regularly revalidate their top-down conviction in the AI and digital infrastructure investment cycle.

- Actively refine sub-industry exposure, recognising that different parts of the supply chain can experience very different fundamentals.

- Maintain stock-level discipline, evaluating valuation, positioning within the supply chain, competitive advantage, and the potential for earnings delivery and positive surprise.

At the same time, investors should consider technology allocations within the broader context of emerging markets. Strong sector-driven bull markets often absorb a disproportionate share of market attention and capital, which can create compelling opportunities elsewhere. We believe a gradual increase in exposure to select non-technology areas of EM may be warranted where investors can access attractive combinations of growth, quality and valuation. While EM earnings remain heavily influenced by technology, opportunities outside the sector are becoming increasingly interesting.

Conclusion: AI remains a key driver, but it is important to be disciplined and selective

Valuations and expectations for 2027 appear demanding, while aspects of market behaviour exhibit characteristics often associated with bubbles. Yet demand growth and earnings momentum remain exceptionally strong. The cycle may continue to surprise positively, supporting earnings growth into 2028 off an already high base.

Nonetheless, investors should recognise that supply is responding, forecast risk remains elevated, and certain market indicators point to rising speculative behaviour.

We believe investors can benefit from actively managing exposure to the technology sector, sub-industry and stocks, while selectively adding to overlooked parts of non-technology EM. If AI adoption evolves broadly in line with current expectations and associated revenues ultimately justify today’s capital expenditure, it could imply a significant transfer of value from labour to capital and disrupt a range of existing business models.

The resulting economic and corporate impacts could be substantial and will require ongoing consideration.

For now, we continue to believe that exposure to the AI theme remains justified. While periods of consolidation and volatility should be expected, we view AI as a generational technology that remains in the early stages of an S-curve adoption cycle.

We expect capital expenditure growth to remain strong into 2028, and we believe there is further potential for positive earnings surprise. However, we recommend that investors remain disciplined, closely monitor valuation expansion, and remain alert to the risks associated with a maturing cycle.

Source: Schroders

Disclaimers:

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Investment involves risk.

This information is a marketing communication. The information contained herein is believed to be reliable. Where third-party data is referenced, it remains subject to the rights of the respective provider and must not be reproduced or used without prior consent.

Any data has been sourced by us and is provided without any warranties of any kind. It should be independently verified before further publication or use. Third party data is owned or licenced by the data provider and may not be reproduced, extracted or used for any other purpose without the data provider’s consent. Neither we, nor the data provider, will have any liability in connection with the third party data.

The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Any references to securities, sectors, regions and/or countries are for illustrative purposes only.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any investments to rise or fall. Schroders has expressed its own views and opinions in this document, and these may change.

This document may contain “forward-looking” information, such as forecasts or projections. Any forecasts stated in this document are not guaranteed and are provided for information purposes only.

Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at https://www.schroders.com/en-za/za/intermediary/footer/privacy-policy/ or on request should you not have access to this webpage.

For your security, communications may be recorded or monitored.

Issued in July 2026 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998.