The private credit market* has almost doubled in the past six years. In recent months, and against a backdrop of AI disruption, rising inflationary pressures and other headwinds, the sector has generated alarming headlines.

In this research we set out the basis for our view of the scale of the risk posed to public markets, which is as follows:

- While there will be areas that are adversely affected, this is not a systemic risk, either to public markets or the economy.

- Public investment grade and high yield bond markets have hardly any direct exposure to software, the sector at the epicentre of concerns, and that exposure is higher quality and in relatively liquid securities.

- Leveraged loans are more exposed to software than bond markets but, even then, it’s manageable. Risks are greater in the USD loan market than EUR.

- At a broader level, private credit is exposed to the same macroeconomic forces as other credit investments. As with high yield bonds and leveraged loans, there will be defaults. Investors should view this as inevitable rather than shocking.

- Spillover risks (to the economy and the public markets) would be greatest via the banking sector but this is not 2008. Banks are in better shape and you need to make implausibly bad assumptions for defaults and recovery rates to put the banking sector in difficulty.

*Throughout the remainder of this document we use the term “private credit” to refer to direct lending, as this is the area that is currently the centre of attention. The broader private credit space is many times larger, estimated to be between $25- and $50-trillion in size, depending on how it is defined. It includes real estate, infrastructure, consumer, and asset-backed finance, among others.

What’s happening in private credit – a recap

Private credit funds aim to deliver consistent income to investors at a yield pickup over public markets. The rationale for this pickup is often put down to their illiquidity – the loans are private so can’t be easily bought and sold, which means investors demand a higher yield to compensate them.

In reality, the magnitude of the additional return is not solely down to illiquidity but also to other factors like transaction size, complexity and the deal sourcing ability of the lender. In most cases, it is impossible to disentangle these different drivers, but it is important to be aware of their existence. “Complexity premium” is a more appropriate description than “illiquidity premium”.

Investors like private debt for the predictable cashflows, borrowers like it for speed and reliability of execution, and flexibility in repayment/contract terms.

The software dimension and AI

Private credit funds have historically liked lending to software companies. Their recurring-fee revenue model led to steady and predictable cashflows, making them a good fit. Historically, sectoral default rates have also been low. Many funds also raised significant amounts of money from institutional investors like insurance companies and, in some structures, retail investors. They needed to deploy this ever-expanding flow of capital quickly, to start earning returns for their investors and fees for themselves (management fees, origination fees etc) with a bias towards what they assumed were the most resilient sectors.

Software companies were keen to borrow and private credit funds were keen to lend. The result is that exposure to software at some of the larger private credit funds is estimated to be as high as 40%, with average exposure across the industry nearer to 20%.

This was all fine until this year, when AI raised concerns about the durability of future cashflows from many software companies. This led to questions over the quality of the assets in these funds, highlighting the possibility that some of these loans had been priced with little provision for downside. It is unlikely this facet is limited to the software sector.

Software is best seen not as the sole source of risk but as a stress‑test for the market. The tensions it has caused have highlighted differences in liquidity and pricing of different kinds of private credit vehicle which invest in the same or similar underlying assets. While traditional private credit funds are closed-ended with a specified life, e.g. seven years, many asset managers also run vehicles which offer greater liquidity.

Business Development Companies (BDCs) in the US are the most well-known. Some of these are listed on the stock market, allowing investors to buy and sell shares in them on a daily basis at the prevailing share price. Partly because of concerns over the software sector, these share prices have fallen to 15-20% discounts to their reported net asset value (NAV) of the funds. NAVs are only updated infrequently and one interpretation is that investors think these NAVs are too high and are likely to be cut.

Other vehicles, such as non-traded BDCs and interval funds, often invest in similar assets but offer periodic liquidity, e.g. quarterly, at the NAV. There are limits on how much of the fund can be sold every quarter, typically 5%.

It is easy to see the potential for problems.

Investors can put in a request to get their money out of the non-traded vehicle at the NAV or sell the traded vehicle at a 10-20% discount to NAV. Similar assets, different liquidity, different pricing, but all resulting in an entirely predictable outcome: mass redemption requests and “gating” of redemptions from the non-traded vehicles. This gating, where investors are told they have to wait until a future quarter to get their money out, is a design feature of these vehicles, not a flaw. It does not mean that the loans inside them are suffering losses, just that there is too much simultaneous demand from sellers. Without gating, funds would be forced to sell assets quickly to raise money to cover redemptions.

If you tried to sell your house in the space of a week, you’d get a poorer price than in an orderly sale process. The same principle applies here. If otherwise sound assets had to be sold quickly at a poor price, the remaining investors in the fund would suffer. The gating is designed to protect those remaining investors.

An important point here is about expectations management. Investors in technology or software-focused venture capital funds would not be surprised if performance suffered due to threats to the software sector (although they’d be hoping to be exposed to the disruptors rather than the disrupted). It is intentional exposure.

The difference with private credit is that many investors in these vehicles thought they were buying exposure to a diversified pool of loans to mid-market companies when, in reality, they have been taking a big sector bet. This is unintentional exposure. Many investors may not have fully understood the portfolio construction risks embedded in these vehicles.

How much exposure do public bond and loan investors have to what’s happening in private credit?

On the assumption that this is contained as a liquidity risk, not a solvency/default risk for software companies, it will have a fleeting impact on financial markets and public markets in particular have nothing to worry about.

What is more interesting is to ask “what if?” it morphed into genuine credit risk for software companies. This can be considered along two main lines: direct exposure to the software sector and/or to BDCs, and indirect exposure via the banking sector. Banks are lenders to software companies and private credit vehicles.

Financials are a large part of investment grade corporate bond markets (much less of a feature of high yield and loans), while the Great Financial Crisis (GFC) demonstrated the economy-wide risks which can emerge when banks suffer a wave of defaults.

Thankfully, on both counts, the risk is low.

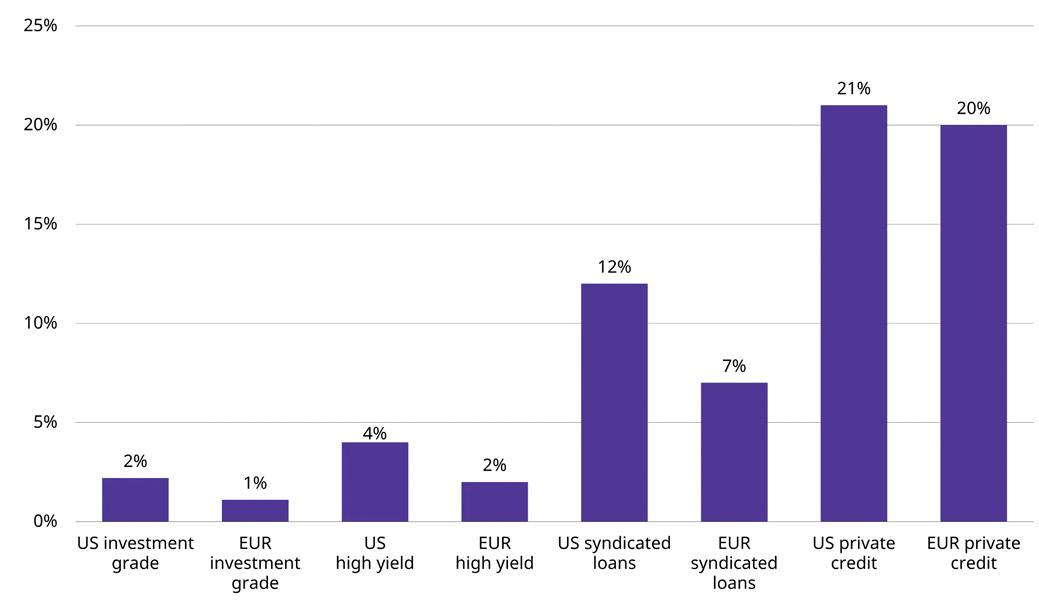

Software makes up only 1-2% of investment grade bond markets and 2-4% of high yield, a fraction of the 20%+ held by private credit industry. The leveraged loan market has more exposure than the bond market, especially in the US, but even here the figures are low relative to private credit.

Public corporate bond and loan markets have limited exposure to the software sector

Source: Schroders, OpenAI, ICE BoAML Global Index System, LCD Pitchbook, JP Morgan, February 2026

Source: Schroders, OpenAI, ICE BoAML Global Index System, LCD Pitchbook, JP Morgan, February 2026

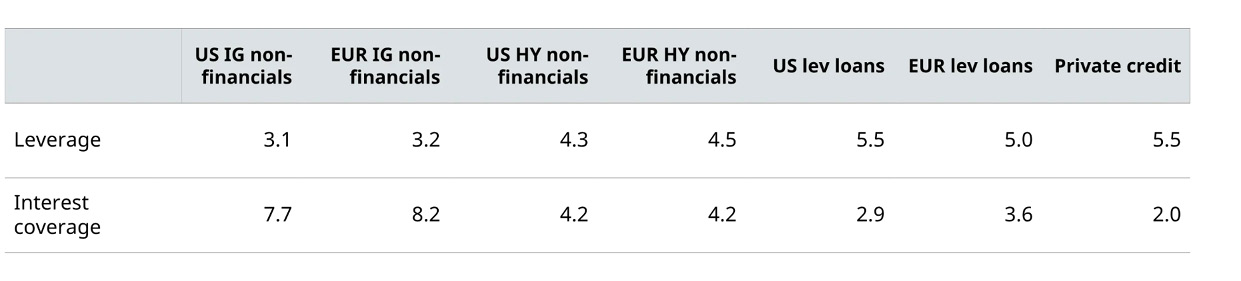

It’s not just that exposure is lower, it’s also higher quality. Credit fundamentals in public markets are stronger than in private credit: leverage is lower and interest cover higher. The risk of default in investment grade bonds is negligible (the median yearly default rate since 1920 has been 0% and the average less than 0.1%, meaning 99.9% of borrowers did not default each year, on average). In high yield bonds, interest cover is roughly double what it is in private credit. Investors in these areas have a far bigger margin of safety than in private credit.

Leverage multiples in private credit also potentially flatter borrowers. EBITDA-adjustments are common e.g. assumed cost reductions/synergies on an M&A deal. While these may materialise there is also risk that they don’t. Estimates suggest that true leverage multiples for private credit are nearer 7x than 5x if these are excluded. This practice is also commonplace in leveraged loans but not to the same extent.

Borrowers in public markets have stronger fundamentals than those using private credit

Source: Bloomberg, Financial Times, Fitch, Moody’s, Pitchbook, JP Morgan. Private credit figures are estimates, based on analysis of a range of sources.

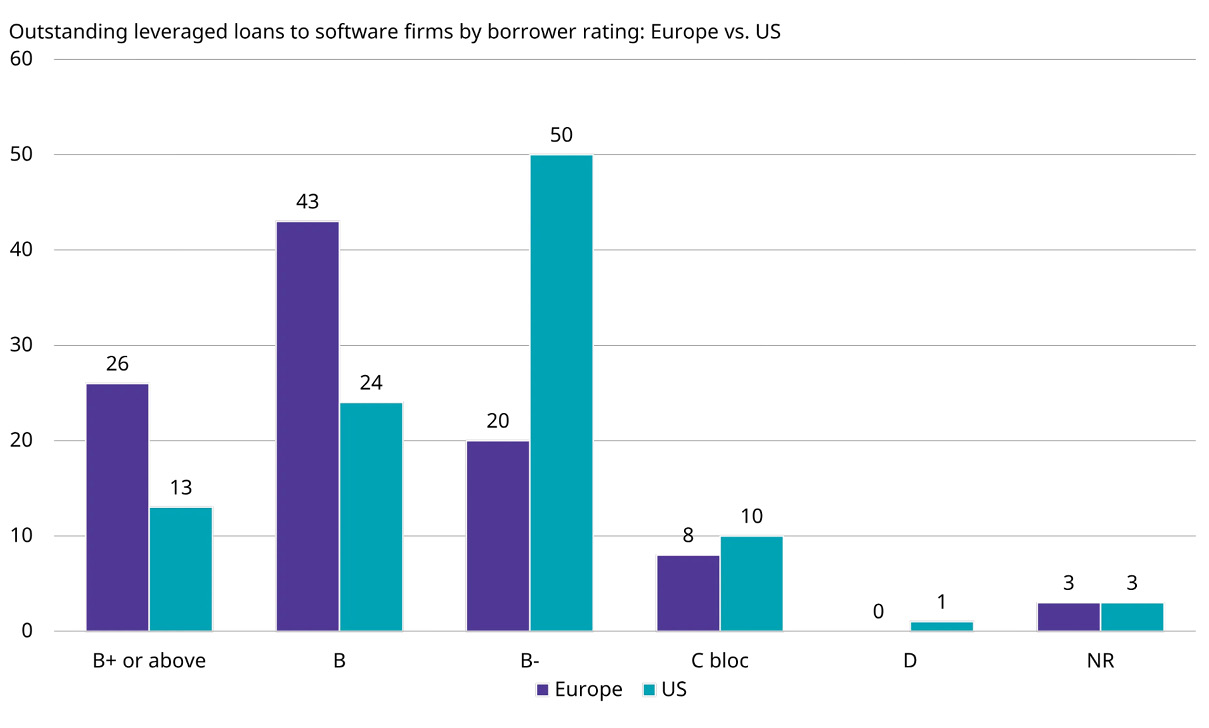

Of these, the only which causes genuine concern is the US loan market. It has much higher software exposure than other public markets and that exposure is notably lower quality than the EUR loan market in particular. 64% of the US software loan market is rated B- or lower (including not-rated bonds), more than double the 31% in Europe.

Not all software loans are equal: Europe skews towards higher-rated, the US lower

Sources: PitchBook | LCD; Morningstar LSTA US Leveraged Loan Index • Data through Jan. 31, 2026

In addition, nearly a third of the software sector of the US loan market is due to mature by 2028 and approximately 14% of those loans (by par value) are currently trading at distressed levels. Assuming the declines in value of stock market listed software companies this year do not reverse i.e. the sector turns out to be genuinely impaired, many risk repricing at notably worse loan-to-value ratios (LTVs), or suffering defaults. Even those avoiding default would face increased borrowing costs, increasing the financial strain they are under and their future default risk.

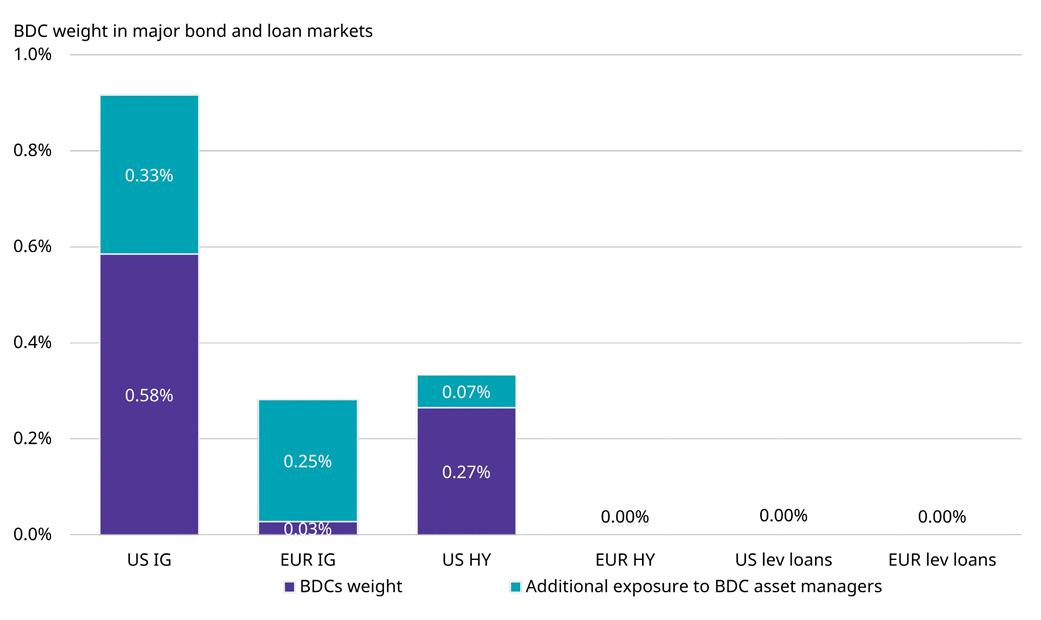

BDCs themselves also borrow in bond and loan markets but public market exposure is near-zero. Even if you include additional debt issued by BDC asset managers then aggregate exposure is still negligible.

Public bond markets have negligible exposure to the debt of BDCs

Source: Schroders, ICE BoAML Global Index System, LCD Pitchbook, March 2026

Source: Schroders, ICE BoAML Global Index System, LCD Pitchbook, March 2026

What about the banks?

Some of the banking issues in 2008 arose from outright fraud (dodgy loans), high exposure to the real estate market, amplified by leverage, in a world where no one knew who was exposed to what (a lack of transparency). That leverage was present both within the banking system (loose regulation) and also through complex derivatives (CDO-squared etc).

To emphasise that latter point, there was around $1.2-trillion of subprime mortgages outstanding, but multiples of that amount of exposure were created via synthetic structures. Synthetic CDOs – funded not by actual loans but referencing mortgage-backed securities through credit default swaps – allowed investors to take repeated long and short positions on the same underlying bonds, greatly amplifying effective exposure across the financial system.

None of these banking sector risks are comparable in private credit today. Amplification via derivatives is minimal – private credit involves direct loans between two parties.

And leverage on the whole is lower. BDCs borrow at around 50% LTV (c.1x debt to equity ratio) so, using this as an example, $500 billion of industry assets would equate to around $500billion of debt. In comparison, real estate LTVs were significantly higher in the run up the GFC, once mezzanine loans and other financing are accounted for.

In addition, of today’s 50%, around half is “super-senior” with a maximum LTV of 25-30%. This is where the banks lend (the remainder comes from the bond market, as outlined above). Super-senior lenders are also allowed to swap underperforming assets in their collateral pool for others, which limits LTV and collateral dilution. There will always be individual cases where borrowers default and/or where lending standards have been less rigorous but it would take an implausibly severe outcome for defaults and recoveries (across the entire private credit loan book, not just the software sector) before the banks would be exposed to problematic losses. In other words, bank lending to private credit is on a conservative basis, posing no systemic risk to the economy.

Broader credit risks outside of software

Being loans to companies, often small and mid-market ones at that, private credit is exposed to the same macroeconomic risks of other credit asset classes. In an economic downturn, defaults would be expected to rise. This is a risk with any credit investment, not one specific to private credit. As the private credit industry grows in scale, some of these will be larger loans that will default, so will be more headline grabbing than in the past. Investors should view this as inevitable rather than shocking.

Higher interest rates also increase the financial burden on borrowers. Similar to leveraged loans, most private credit loans are floating rate so the pass-through from higher rates is immediate. In contrast, higher rates only impact borrowers in investment grade and high yield corporate bonds with a lag, when existing fixed rate debt needs to be refinanced.

For now, the US economy is doing well but the cuts to rates which had been expected before the Iran situation flared up look less likely. The more pressing question is whether policy simply stays on hold in 2026 or whether persistent inflation forces the Fed into tightening. Our base case is that they will refrain from hikes before returning to easing policy in 2027.

Against this backdrop, pressure on refinancing and recoveries can be ok but, if and when outlook weakens, default rates could rise materially.

But this is no different to what happens with high yield bonds or leveraged loans.

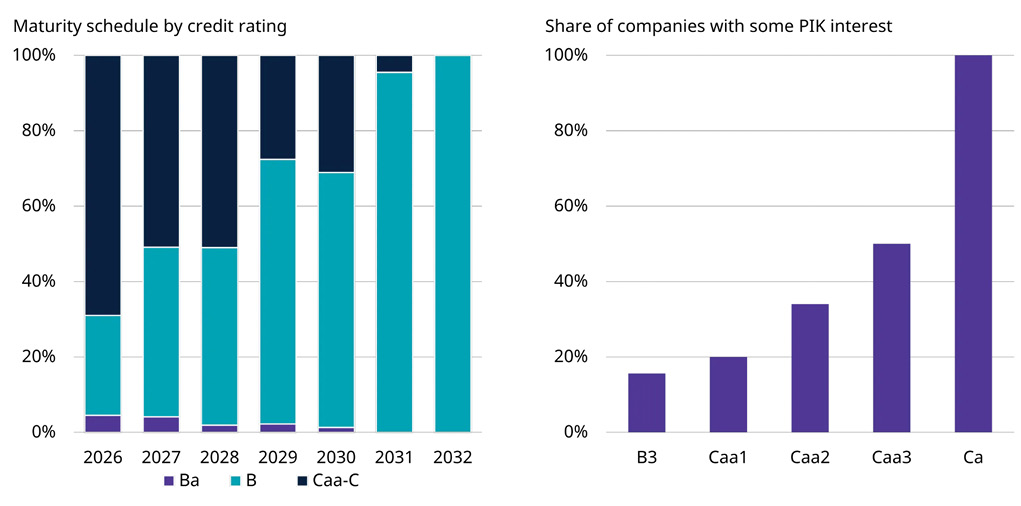

What is a particular stress point for the private debt market is that a large share of near-term mid-market refinancing requirements sits with the weakest borrowers – those Moody’s estimates would be rated as Caa or weaker.

Many of these borrowers have also been avoiding technical defaults by switching to payment-in-kind (PIK) loans. Here, borrowers have effectively “switched off” cash interest payments, with that interest rolled up as additional capital to be repaid at maturity.

That defers immediate default risk, but it does not eliminate it, as ultimately the larger repayment amount will become due.

The flexible and bilateral nature of private credit means some of these loans may be amended and extended further. However, this pushes risk out in time rather than resolving it. As a result, default risk remains elevated, even outside of the software sector.

Even so this does not mean it is a problem for investors in public market fixed income markets, where credit fundamentals are much stronger.

The maturity schedule is dominated by distressed companies, many of which rely on “Payment In Kind” loans

Source: Moody’s, April 2026

The insurance channel

A further potential spillover channel is via end‑investors in private credit funds, notably insurance companies. While insurers have increased allocations to private credit in recent years, these exposures typically sit in long‑term, hold‑to‑maturity portfolios and are not subject to daily liquidity demands or margin requirements. As a result, valuation pressure in private credit is unlikely to trigger forced selling of public market assets.

A recent S&P report also stress tested the US life insurance market, for a private credit downturn:

“In all the scenarios, except for the most extreme one, we believe the impact on nearly all the rated insurers would be manageable with likely no effect on ratings. In the most extreme scenario (which we think is highly unlikely), roughly half of insurers might experience modest ratings pressure”

The more plausible impact would be on future allocation decisions from insurance companies and underwriting standards, rather than near‑term financial market spillovers.

Big enough to be a risk?

Direct lending is now of a similar size to the high yield and leveraged loan markets. If it were to seize up then this could remove an important source of financing to the corporate sector, with broader economic implications. But, realistically, this is a bit of a strawman.

Many private credit loans back private equity transactions. Private equity is sitting on record levels of dry powder (money raised but not yet deployed) which will need debt finance to complete deals. Post-Great Financial Crisis banking regulation means the banks are unwilling/unable to provide finance at the higher levels of leverage typical in these transactions. Unless that changes in a meaningful way, there will be a need for other lenders to fill the void. Private credit and leveraged loans play an important role.

A more likely transmission mechanism than a full-blown seizing-up is a repricing. If investors pull back, financing would be more constrained and spreads on new loans would increase, which would then attract more investors back to the space.

Conclusion

The systemic risks from private credit are low. Direct and indirect exposure in public markets is also low, and the exposure that exists is higher quality than in the private credit space. It is not a systemic problem for public markets – though it presents a meaningful stress event within private markets themselves.

The financial market spillovers from stresses in the private credit market and worries about AI’s impact on software, including relatively indiscriminate selling of software bonds, are also leading to opportunities. While the AI disruption narrative is real and warrants careful credit selection, we believe the market has, in several cases, overcorrected — pricing in levels of disruption risk not yet supported by underlying fundamentals. There are opportunities for active investors.

Paradoxically, the tensions faced by private credit funds could be seen as a much-needed learning opportunity for both regulators and funds, leading to innovation in strategy design i.e. in valuations and more flexibility to manage liquidity and cyclical swings better.

A shakeout should also mean private market lending loses some of its ‘frothiness’ – spreads have been low for the quality of companies they have been lending to and underwriting standards have loosened a lot. A correction in these should be healthy for the market going forward.

Source: Schroders

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Investment involves risk.

This information is a marketing communication. The information contained herein is believed to be reliable. Where third-party data is referenced, it remains subject to the rights of the respective provider and must not be reproduced or used without prior consent.

Any data has been sourced by us and is provided without any warranties of any kind. It should be independently verified before further publication or use. Third party data is owned or licenced by the data provider and may not be reproduced, extracted or used for any other purpose without the data provider’s consent. Neither we, nor the data provider, will have any liability in connection with the third party data.

The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Any references to securities, sectors, regions and/or countries are for illustrative purposes only.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any investments to rise or fall. Schroders has expressed its own views and opinions in this document, and these may change.

This document may contain “forward-looking” information, such as forecasts or projections. Any forecasts stated in this document are not guaranteed and are provided for information purposes only.

Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at https://www.schroders.com/en-za/za/intermediary/footer/privacy-policy/ or on request should you not have access to this webpage.

For your security, communications may be recorded or monitored.

Issued in June 2026 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998.