Hedge funds always report their performance net of fees, which is their defence against what are perceived as higher fees. Getting the balance right in delivering to investors while often taking very high fees is the challenge most hedge fund managers face.

Fee disclosures in South Africa are transparent

Fee models in South Africa are generally structured around a management fee and a performance fee. Management fees typically range from 1% to 2% pa, while performance fees are often set at 20% of the outperformance above a specific hurdle rate or benchmark. All fees must be disclosed in accordance with the ASISA standards. This transparency allows investors to understand the impact of costs on their net returns.

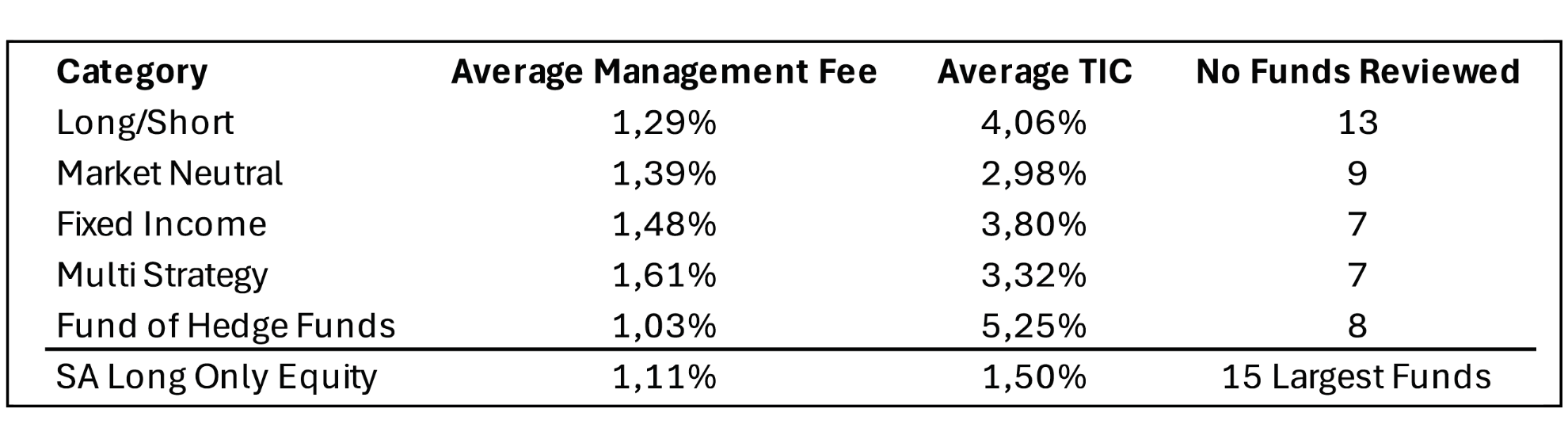

Given that almost all hedge funds have the combination of a management fee and a performance fee, it is no surprise that hedge funds have significantly higher Total Investment Costs (TICs) than their long-only fund counterparts.

In the table below, the average of a selection of hedge fund fees and their TICs are outlined per category. These are then compared to the SA Long Only Equity unit trust sector. The fees in this table and in all subsequent tables in this article are all expressed inclusive of VAT to ensure consistency. As can be seen, the long-only funds have a significantly lower average TIC (1.50%) than each of the hedge fund categories, where the average TIC ranges from 2.89% for Market Neutral funds, to 5.25% for Fund of Hedge Funds.

It is no surprise that Fund of Hedge Funds have the highest costs, because most in this category have two levels of cost, one at the top fund level and the second at the level of each fund held in the top-level fund. The challenge with assessing and comparing hedge fund fees is that often, even in the same sector, it is like comparing apples and pears.

This can be seen in a brief analysis of the funds reviewed in each sector.

Long-Short Equity Funds

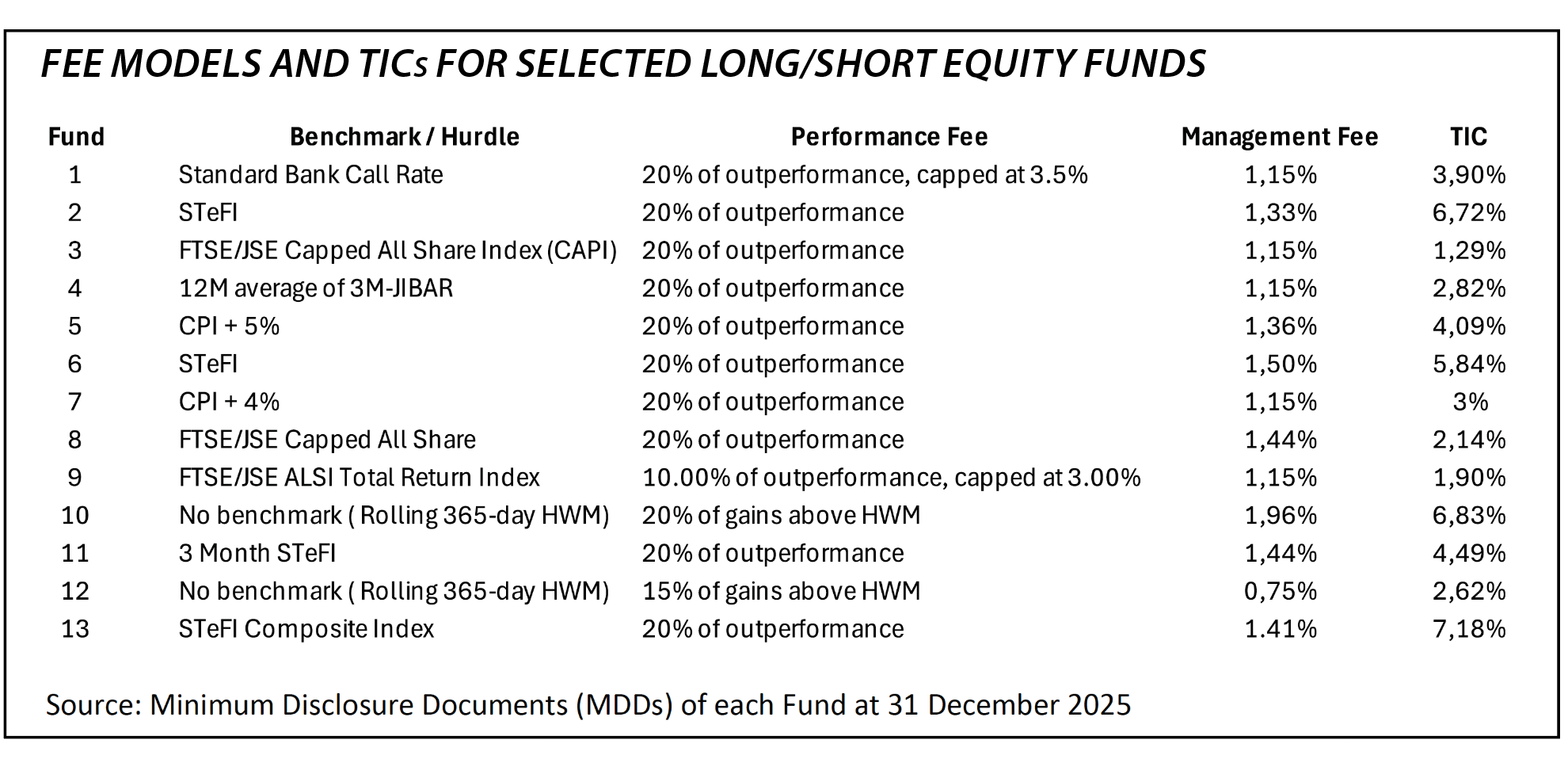

As can be seen from the table below, among the 13 long-short funds reviewed, there is some consistency at the management fee level, which is generally in the range of 1% to 1.5%, although there is one outlier with a management fee of 0.75% pa. In contrast, the TICs have a far wider range, extending from 1.29% pa to 7.18% pa, with an average of 4.06% pa.

This range of TICs is primarily a function of the performance fees charged, which are a function of three factors: firstly, the performance benchmark or hurdle which the fund must beat to earn a performance fee; secondly, the percentage of outperformance that the fund takes as a fee; and thirdly, the actual performance of the fund. Among the 13 funds there are eight different benchmarks and two funds with no benchmark, but which measure themselves against a Rolling 365-day High Water Mark (HWM).

Performance benchmarks

As can be seen, the range of benchmarks is significant, with some funds measuring themselves against cash benchmarks such as STeFI or JIBAR, others against equity indices and some against inflation plus targets. A summary of the different types of benchmarks is provided below:

- Cash 6

- CPI+ 2

- Equity Index 3

- None 2

In the case of the two funds with no benchmark, the fund managers only earn a performance fee when the current Net Asset Value (NAV) exceeds the highest NAV achieved during the immediately preceding 365 days. As a result, the performance calculation period of the fund moves forward every day and as a result the calculation ignores any performance peaks that occurred 366 days earlier.

Essentially a fee is earned every day that the current NAV is greater than the maximum NAV of the past 365 days.

There is a distinction between when a fee is accrued and when it is paid out. In most South African retail and qualified investor hedge funds, the performance fee is calculated and “set aside” (accrued) within the NAV daily. If the fund is above the 365-day high today, a portion of that day’s gain is earmarked for the manager. While the fee is earned daily based on the rolling window, the actual cash is typically paid to the manager at set intervals – usually monthly, quarterly or biannually.

There is, however, usually a claw back in the fee if the fund underperforms. For example, if the fund earns a fee on Monday because it hits a 365-day high, but the market drops on Tuesday, the accrued fee is usually reversed (reduced) before the final payout date.

Fee as a percentage of outperformance

In 10 of the funds, the performance fee is 20% of outperformance. This level harks back to the early days of hedge funds which traditionally had what was known as a “2 and 20” fee model: 2% management fee plus 20% of outperformance.

We can see in this instance that the management fees have generally come down significantly from the “2” level, but performance fees remain largely committed to the “20” level.

There are, however, two funds that cap their fees, one at 3.5% and the other at 3%. By capping their fees, the fund managers are putting a limit on the quantum of their fee and ensuring that the investor benefits fully from any outperformance thereafter.

Fees don’t always correlate with performance

Given the variety of benchmarks that hedge funds use to determine their performance fees, combined with the percentage of outperformance they take, it is inevitable that better performing funds don’t necessarily take the biggest fees.

From the sample of 13 funds reviewed in the table, fund 13 had the highest TIC at 7.18%, but its performance for the calendar year of 2025 was 24.39% while fund three with a TIC of 1.29% delivered a return of 35.26% in 2025.

The key difference was the benchmark used. Fund 13’s benchmark is the STeFI Composite Index, effectively a cash benchmark, which delivered 7.5% in 2025 versus fund three’s benchmark, which is the FTSE/JSE Capped All Share Index (CAPI) which delivered 42.61% in 2025. As a result, fund three, despite significantly outperforming fund 13 in 2025, was unable to charge a performance fee for its efforts.

Market Neutral Funds

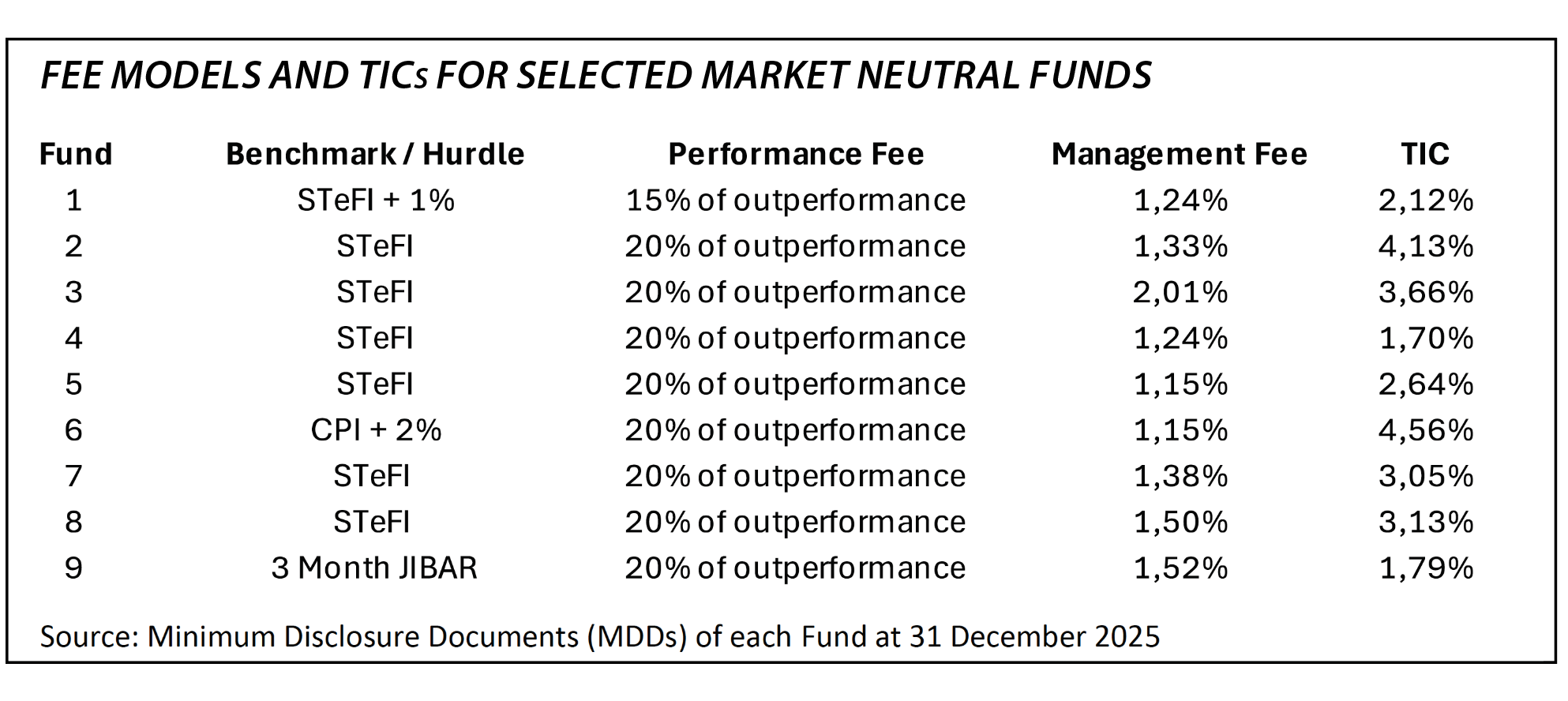

As can be seen from the table below, Market Neutral Funds have annual management fees ranging from 1% to 1.75% pa. Unlike the Long-short Equity Funds, the performance fee is more consistent across the funds, with all except one (at 15%) having a performance fee of 20% of outperformance.

There is also less variation in the Benchmark/Hurdle rates with STeFI most common (seven funds) and the remaining two funds having JIBAR and an inflation plus hurdle respectively. The average management fee is 1.39% pa while the TICs range from 1.79% to 4.56%, and the average TIC came in at 2.89%. (The TIC for fund three was not disclosed.)

Fixed Income Funds

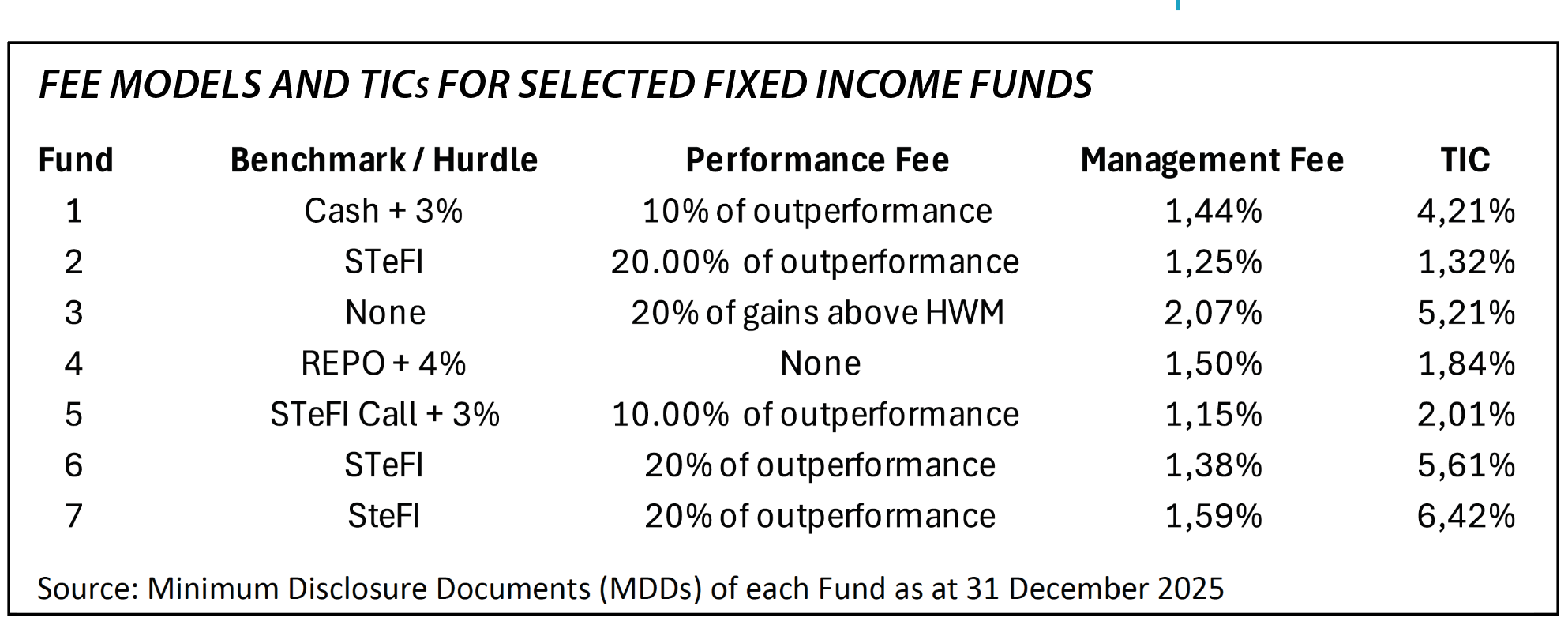

As can be seen from the table below, the annual management fee ranges from 1% pa to over 2% pa with the average management fee being 1.48% pa.

The Benchmark/Hurdle rates are all linked to a cash benchmark, STeFI or REPO plus, while one fund has no hurdle rate but takes a percentage of gains above a High Water Mark. One fund does not charge a performance fee, charging a flat 1.30% pa.

Two funds charge a performance fee of 10% of outperformance and the balance charge 20%. The average TIC came in at 3.80%.

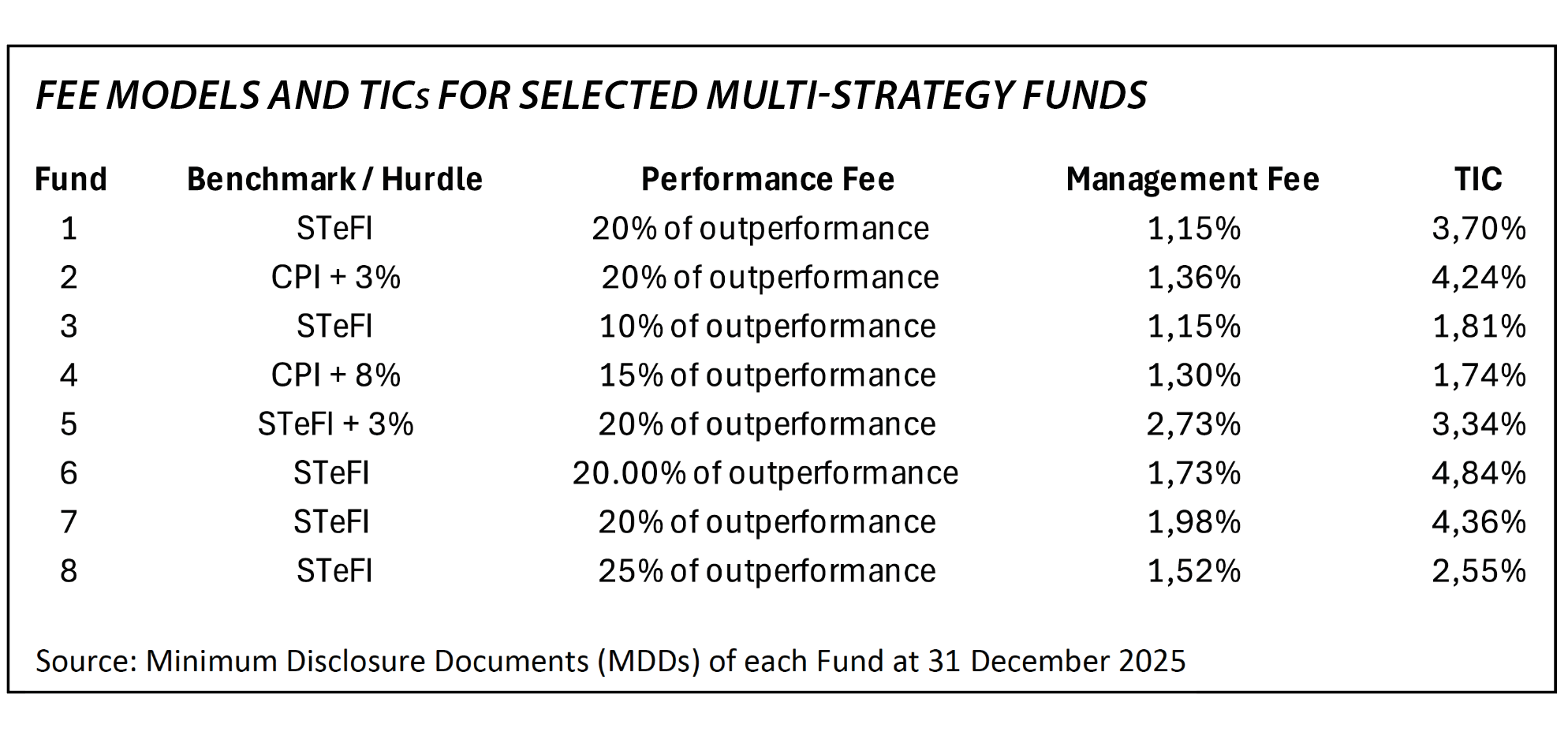

Single-Manager Multi-Strategy Funds

As can be seen from the table below, the annual management fee for Multi-Strategy funds ranges from 1% pa to 2.73% pa with the average annual management fee at 1.61% pa.

The most common performance benchmark is STeFI (six funds) while two funds have inflation plus hurdles, with six funds taking a 20% of outperformance fee and one taking 10% and another 15%. The TICs range from 1.74% to 4.84%, with the average TIC at 3.32%.

The impact of fees on performance can be clearly seen in this sector, where fund four with a TIC of 1.74% returned 13.93% pa whereas fund six, with a TIC of 4.84% pa, returned 13.64% for 2025.

Given that the performance is reported after fees, fund six outperformed fund four by 3%, yet investors in fund four ended up slightly better off than those in fund six based on lower fees.

Also, what is interesting to note is that fund four has a significantly higher performance hurdle, CPI +8%, than all the other funds in the sector.

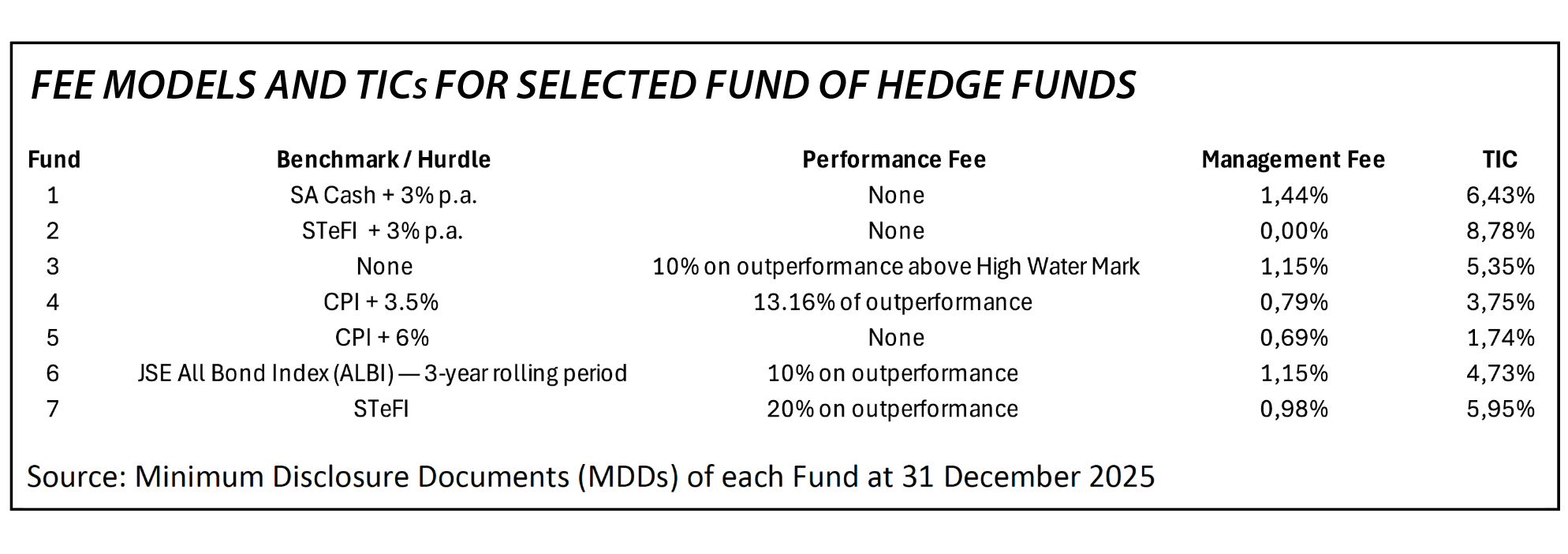

Fund of Hedge Funds

Two interesting features of the Fund of Hedge Funds shown in the table below is that on the one hand there are relatively more funds than other sectors that don’t charge a performance fee (three out of seven), but the range of TICs is significantly higher than the other sectors, from 1.74% to 8.78%, with an average TIC of 5.25% which is over 1% higher than the next highest sector.

Despite the relative lack of performance fees, the higher TICs are explained by the two tiers of fees that investors must pay. At the fund level, there is a management fee that ranges from 0.69% to 1.25% pa with one fund charging no annual fee or performance fee, yet this fund (fund two) has the highest TIC at 8.78%.

It also has relatively poor performance, returning 12.19% in a year when the top three funds in the sector returned around 45% and the average fund returned 18.05%. Again, it can be seen how fees can severely disadvantage investors.

Performance fees don’t need to be complicated to be effective

This analysis reinforces the theme that not all hedge funds are made equal, particularly when it comes to fees.

The analysis shows the variety of approaches to charging fees even within a standard model of an annual management fee plus a performance fee. It is worth noting that simply having an annual management fee linked to a percentage of the NAV of a fund is a performance fee.When the fund NAV rises, through positive performance, the manager’s management fee automatically rises, as does the value of the investor’s investment.

Similarly, the manager’s fee declines in periods of negative performance, as does the value of the investor’s investment. In essence the annual management fee aligns the interests of investors and managers perfectly. This begs the question, why hedge funds have such an emphasis on performance fees, because arguably the primary beneficiary of this structure is the manager, not the investor. The argument in favour of performance fees is that it ensures that the best fund manager talent is suitably incentivised to manage money for investors.

Management fees can be slightly more complicated elsewhere in the world

To ensure that this talent is available and incentivised, the international hedge fund market, particularly among large multi-strategy firms such as Citadel, often employs a “pass-through” fee model.

This structure differs significantly from the fixed management fee used in South Africa. In a pass-through model, the fund does not charge a set percentage for management. Instead, it “passes through” all operational expenses of the firm directly to the investors.

These expenses include:

- Compensation for portfolio managers and research analysts.

- Technology and data infrastructure costs.

- The costs associated with office space and global operations.

- Legal and compliance expenses.

Under this model, the total operational cost can be significantly higher than a standard 1% or 2% management fee. When combined with performance fees, the total cost to the investor in a pass-through structure can exceed 10% of the NAV in certain years.

This model is used by large international firms to attract and retain top-tier investment talent by offering highly competitive compensation packages funded directly by the pool of assets.

The bottom line

Fortunately, in South Africa, the slightly more complicated international management fee model is not standard practice, and the regulatory emphasis remains on fixed, disclosed manage-ment fees to ensure cost predictability for the investor.

The question that financial planners and investors need to ask themselves when selecting a hedge fund, is whether the performance fee charged is reflective of the quality of the management of the fund in which they are investing.

After all, as Warren Buffett so succinctly put it, “Price is only an issue in the absence of value.”