The challenge that financial planners and investors face is selecting the “right” hedge fund. But this selection risk can be mitigated to a certain extent if one incorporates hedge funds into long-only portfolios, providing the opportunity to benefit from the return and risk benefits that hedge funds offer.

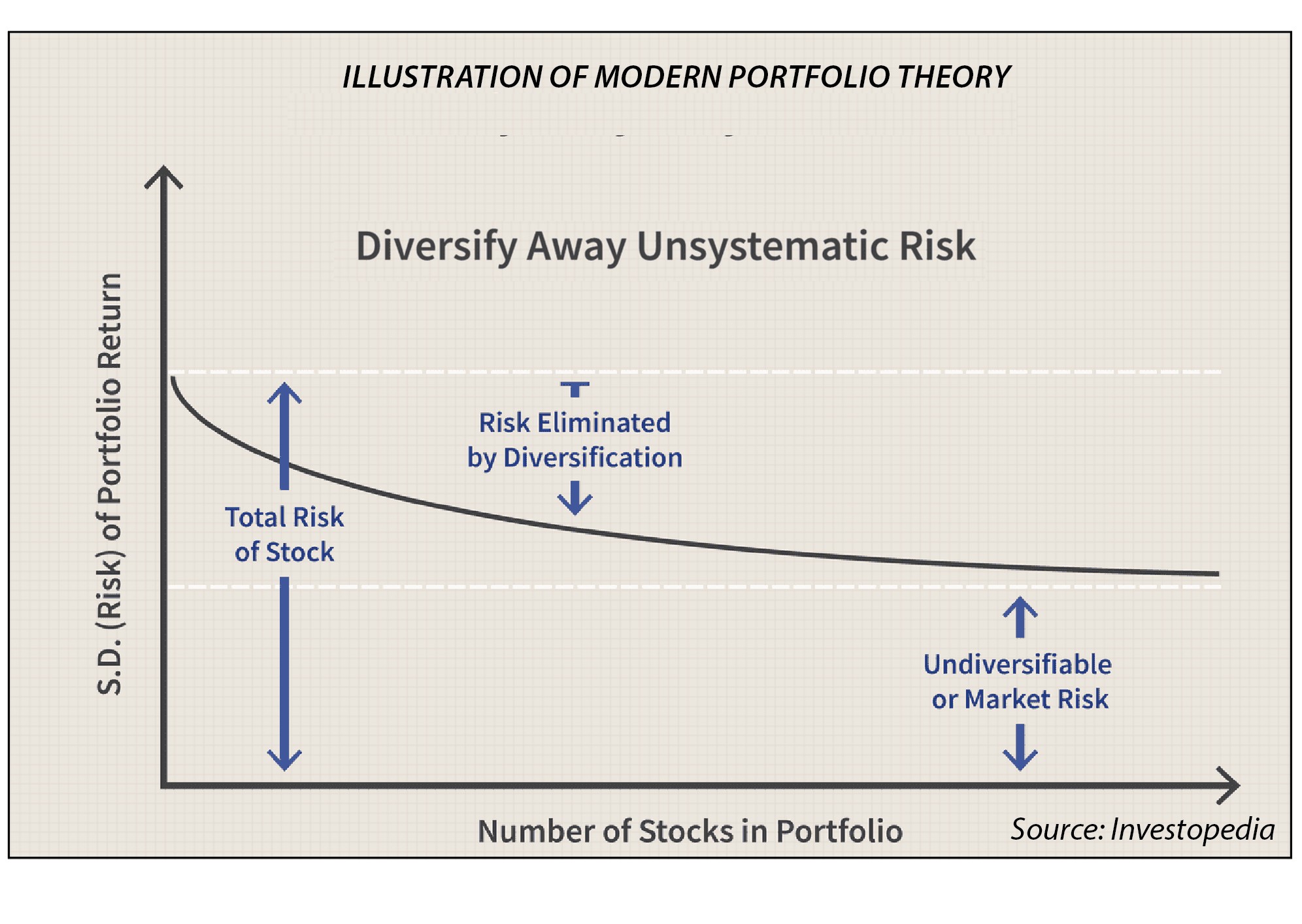

Diversification is the only “free lunch” in investing

Harry Markowitz, the Nobel laureate and founder of Modern Portfolio Theory, popularised the saying that the only “free lunch” in investing is diversification. Markowitz mathematically proved that by adding uncorrelated assets to a portfolio, one can reduce the risk of the portfolio, without giving up expected returns. In a traditional long-only portfolio of equity and fixed-income funds, hedge funds can offer a valuable source of uncorrelated returns, thereby reducing risk for the investor.

The graph below illustrates the benefits of diversification with uncorrelated assets. The theory shows that as you increase the diversification of the portfolio by adding uncorrelated assets, the variance (risk) of the portfolio decreases as unsystematic risk is diversified away. However, some systematic or market risk is inherent in engaging in the financial markets. This risk cannot be diversified away.

The difference between the total risk of a single asset and a portfolio’s risk from diversification is the risk that can be eliminated through diversification.

The difference in risk reduction between adding correlated and uncorrelated assets is substantial. For example, if you apply Modern Portfolio Theory, combining 25 uncorrelated assets (15% correlation) reduces the standard deviation of portfolio returns by an impressive 58%, while doing the same with 25 highly correlated assets (90% correlation) results in only a 5% risk reduction.

Hedge funds turn this theory into practice by employing derivatives, short-selling and arbitrage strategies, which, for an equity-based portfolio, can result in relatively low correlation to equity indices, provide downside protection during market drawdowns and offer the potential to generate strong, alpha-driven returns.

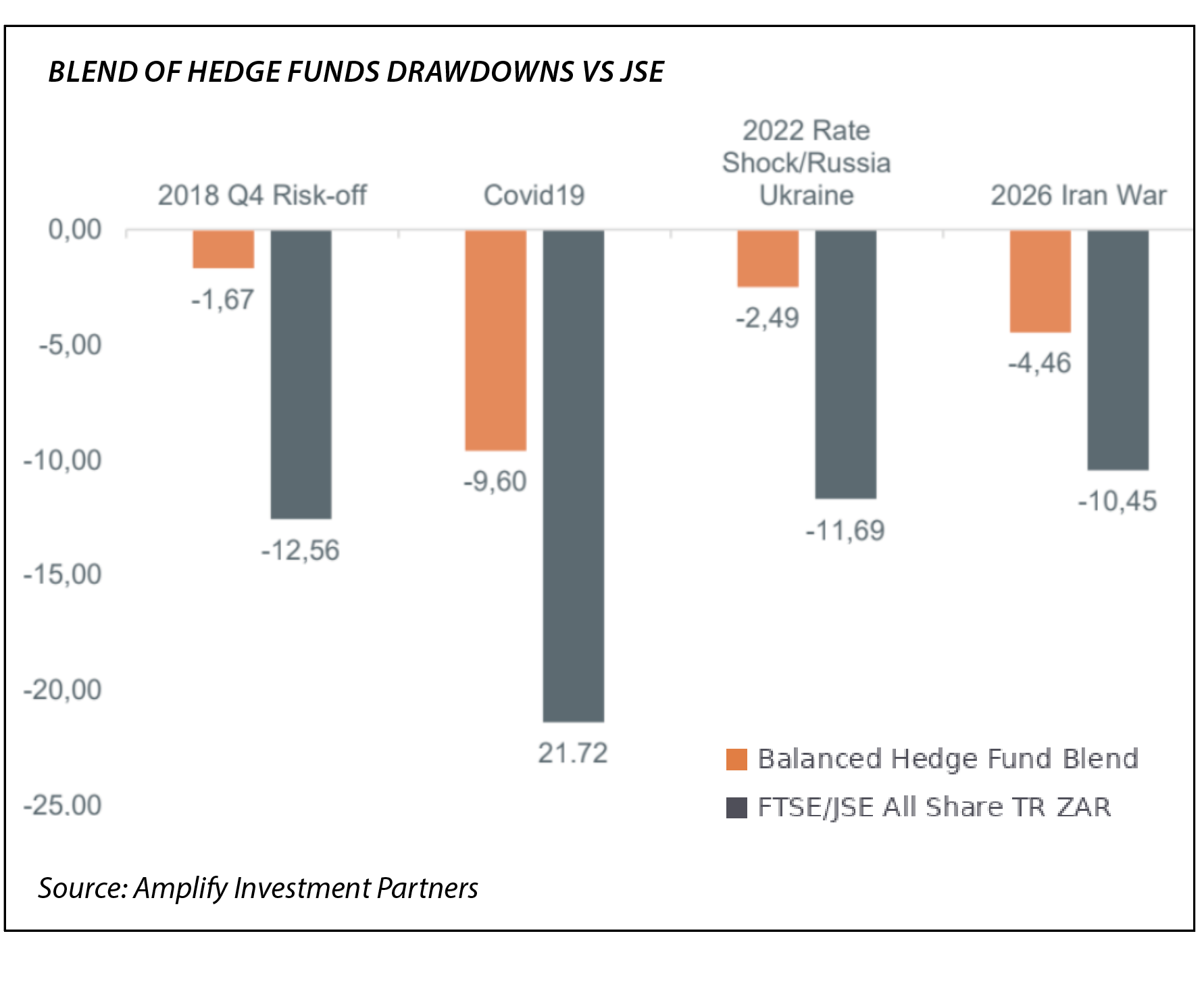

Market drawdowns are where hedge funds earn their keep

During market drawdowns, hedge funds tend to significantly outperform long-only funds and the market. This is illustrated through the graph on the right, which illustrates the drawdown protection, a blend of hedge funds offers during times of crisis. During large market shocks, such as the recent Iran war, the hedge funds’ short positions and derivatives provided protection to the portfolio, as reflected in the orange bars versus the equity market drawdowns reflected in the grey bars. This drawdown protection provides investors not only with financial benefits, but also with psychological benefits. Investors with hedge funds in their portfolio will have a “smoother ride”, which helps manage the emotional toll of market volatility.

The reputation that hedge funds have developed for being risky, highly leveraged vehicles is patently false in the South African context. While international hedge funds remain largely unregulated and can make use of unlimited leverage and risky strategies, regulated South African hedge funds are comparatively low risk and operate within strict regulatory and risk management frameworks designed to provide investors with capital protection, as can be seen from the lower drawdowns in the graph below.

Combining hedge and long-only funds offers a potentially smoother journey

By adding hedge funds to a traditional portfolio of long-only unit trusts, which may generate strong returns during bull markets but are often exposed to significant volatility and prolonged drawdowns during periods of market stress, the risk of the portfolio can be significantly reduced. This consistency can materially improve a portfolio’s Sharpe Ratio, which measures the return earned per unit of risk taken.

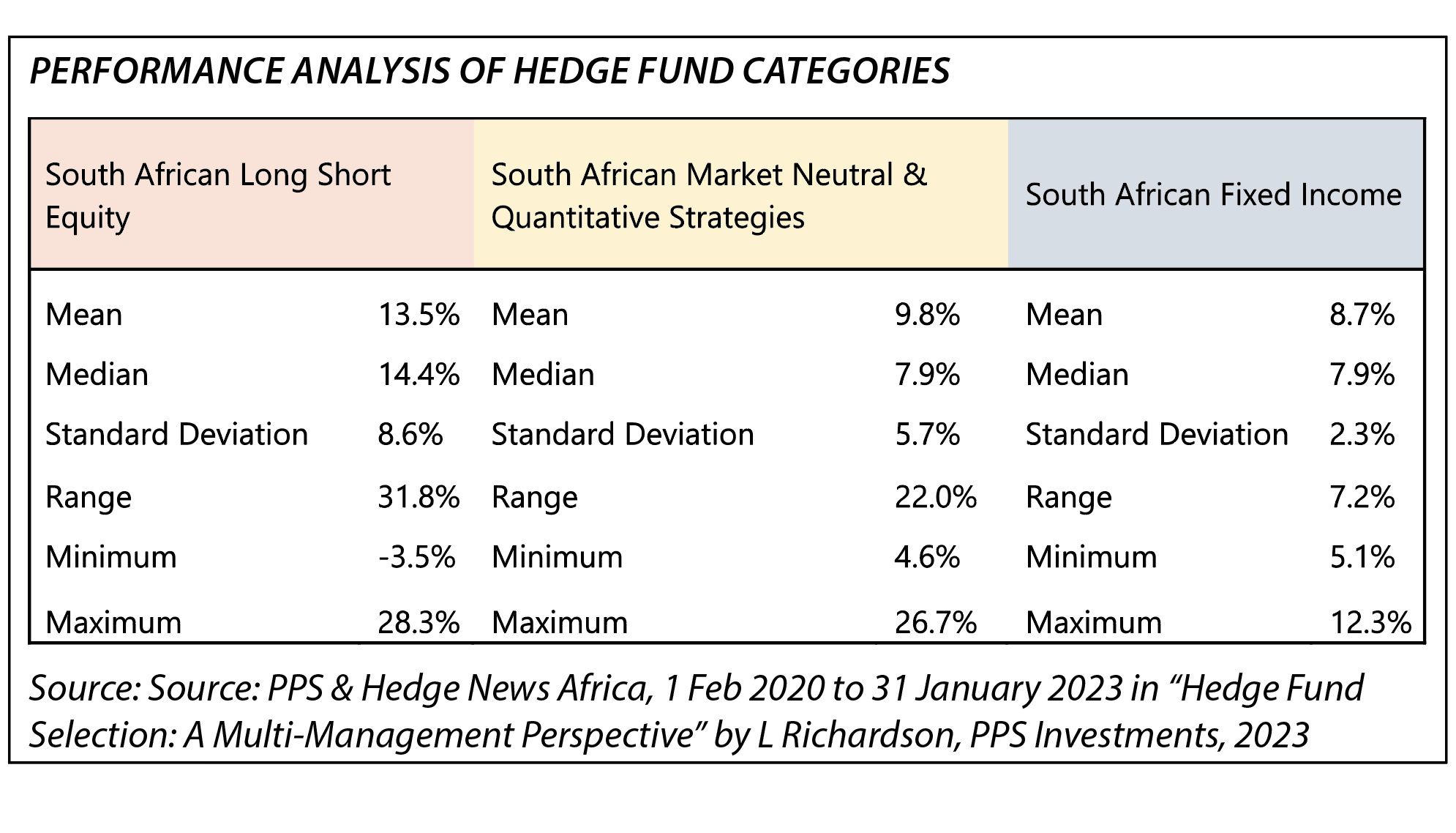

By incorporating hedge funds alongside traditional asset classes, investors can therefore potentially achieve superior long-term compounded returns while experiencing lower overall portfolio volatility and reduced capital losses during adverse market conditions. This is shown in the table on the right, which analyses the performance of the three main hedge fund categories in South Africa, which have very different return and risk profiles. The table shows the return and risk of each of these different categories over a three-year period from the beginning of February 2020 to the end of January 2023.

During the period studied, long-short equity had a mean (average) return of 13.5% while market neutral had a mean return of 9.8%. While market neutral’s mean return was 3.7% less than long-short equity, its standard deviation of returns was 2.9% lower.

Fixed-income funds offered the lowest return, but had significantly less risk, as measured by the standard deviation of returns, than both the long-short equity and market neutral funds. Clearly, the different hedge fund categories provide different solutions for investors, and financial planners can therefore select strategies that best align with their clients’ return objectives, risk tolerance and portfolio diversification needs.

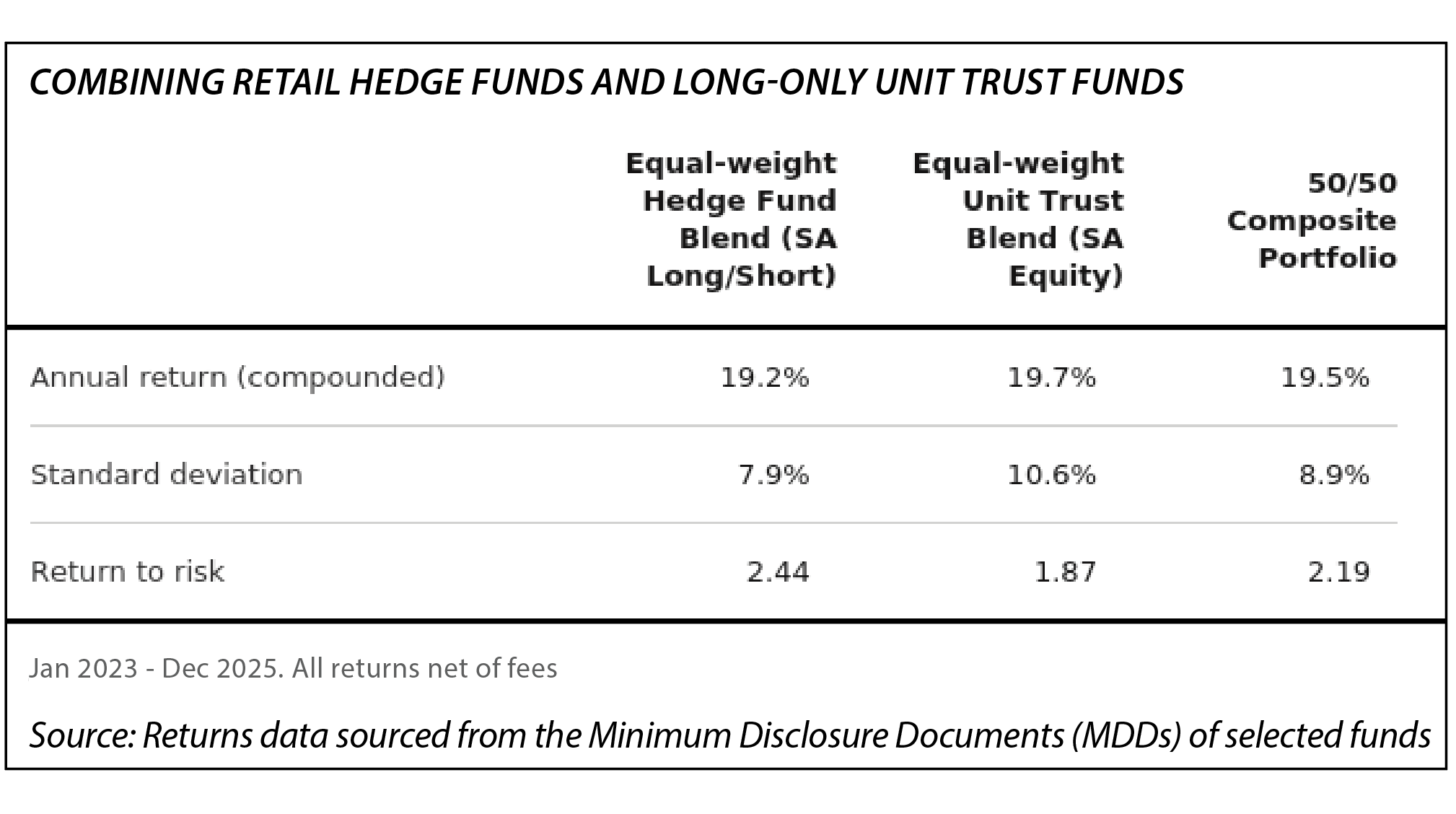

While financial planners and investors can choose different types of hedge funds to meet different return objectives and risk appetites, the real opportunity in South Africa now lies in enhancing long-only portfolios with the inclusion of hedge funds. The impact that this could have on a portfolio is demonstrated in the example outlined in the table on the opposite page, looking at a historical comparison and the effects of diversification with hedge funds in action.

The table shows returns, standard deviation and return-to-risk data for a blend of long-short hedge funds, a blend of long-only unit trust funds and a portfolio with a 50/50 weighting to the hedge fund blend and the unit trust blend.

The portfolio, which is diversified with hedge funds, generated a 1.7% lower standard deviation than the unit trust blend and had a 0.2% lower annualised return. Importantly, the return-to-risk ratio increased from 1.87 to 2.19. This improvement in the risk profile is a direct result of the low correlation between long-short equity hedge funds and the broader market – the hedge funds’ ability to hold short positions means they can dampen drawdowns during periods of market stress, reducing the overall volatility of the blended portfolio without sacrificing significant return.

The result is a meaningfully better return-to-risk ratio and a lower probability of losing money in any given year, illustrating the core diversification argument for allocating a portion of a portfolio to hedge funds.

The bottom line

While regulated and transparent hedge funds in South Africa are a relatively new investment opportunity for financial planners and their clients, there is no need for financial planners or investors to go “out on a limb” and invest only in hedge funds. There is a real opportunity, if they can select the “right” hedge fund or funds, for financial planners and investors to enhance their existing long-only portfolios with the inclusion of hedge funds.

For this shift in portfolio construction to be effective, though, it is critical that thorough research and detailed due diligence are conducted on any potential hedge funds that are being considered. The fund mandate, the manager’s skills and track record in delivering appropriate returns at acceptable levels of risk, and a clear understanding of the fees charged by the fund are all critical elements to be considered when deciding to include hedge funds in a long-only portfolio.

Regulatory reality check

Currently, the only way for hedge funds to be included in a long-only portfolio would be as a separate fund alongside the long-only funds, rather than the hedge fund being included in the long-only unit trust. This may change subject to the ongoing holistic review of Board Notice 90 of 2014, which currently governs the assets that may be included in a “CIS in Securities” (traditional long-only unit trusts).

BN90 has prohibited long-only portfolios from investing in hedge funds, even though South African hedge funds have been regulated as Collective Investment Schemes (under Board Notice 52) since 2015.

FSCA previously published a draft amendment to BN90 intended to allow CIS managers to include hedge funds in their portfolios – specifically those hedge funds already compliant with Regulation 28 of the Pension Funds Act.

The current status is that while the industry (via ASISA) has expressed optimism that FSCA will finalise this review, the broad inclusion of hedge funds into standard long-only unit trusts is still pending the finalisation of these amendments.

A potential move to align BN90 with Regulation 28 is a possible path for general long-only unit trust funds. Since many unit trusts are marketed to retirement funds, enabling them to hold hedge funds up to the Regulation 28 limit (currently 10% for a single hedge fund and 15% in aggregate) within a CIS structure is seen as the potential solution to integrate hedge funds into long-only funds.

While waiting for a full BN90 overhaul, FSCA issued CIS Notice 2 of 2024, which provides an exemption to Board Notice 52. This lifted the 75% investment cap for retail hedge funds that act as “feeder funds” and allows a South African retail hedge fund to invest 100% of its assets into a single offshore hedge fund. This effectively enables a “unit trust-like” structure (the feeder) to provide retail investors with pure exposure to offshore hedge fund strategies.

* As published in the Blue Chip 2026 Hedge Fund guide.