The main purpose of investing is to take advantage of differences between market participants’ expectations and underlying economic activity. Traditional approaches to asset management have evolved very little, still using the same methods, be it single-period metrics like price to earnings ratios or multi-period valuations such as discounted cash flows to arrive at price targets.

We see the following issues with the traditional approach to asset management:

- Single-point estimates lead to overconfidence and assumed precision. In reality, we cannot predict the future.

- There is a bias to overweight short-term news flow and as a result, analyst earnings revisions tend to follow reported earnings in an incremental fashion.

- Discounted cash-flow valuations suffer from a large sensitivity to arbitrary assumptions.

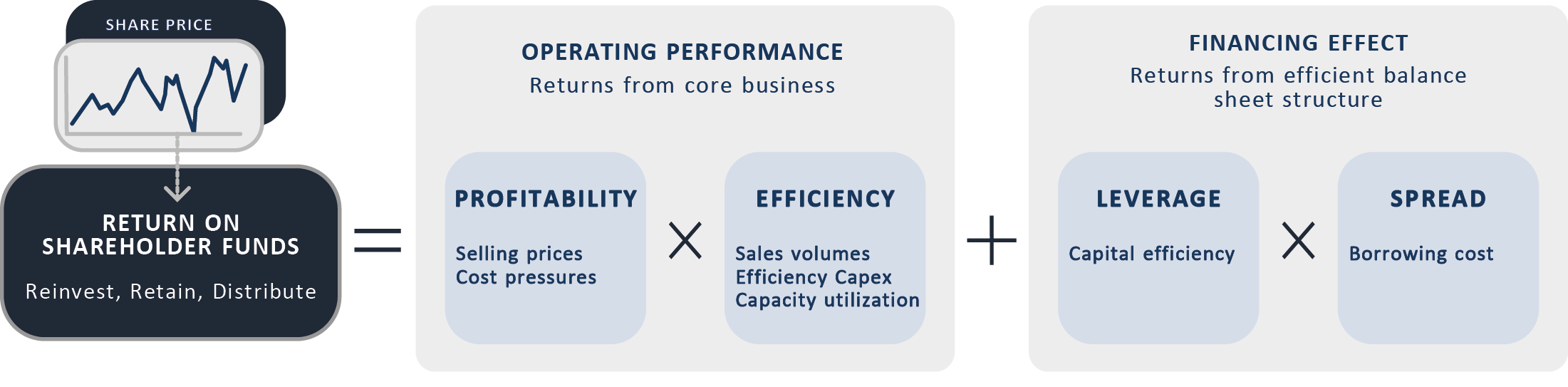

- Traditional financial statements do a poor job of separating operating activities from financing activities, thereby muddying the waters when trying to determine what long-term sustainable returns could be.

Annie Duke, ex World Series of Poker champion, points out in her book, Thinking in Bets: Making Smarter Decisions When You Don’t Have All the Facts that the better you are with numbers, the better you are at spinning those numbers to conform to and support your beliefs. In our view, this typifies some of the issues with traditional approaches to investing where biases can easily get in the way of providing clean investment signals.

“Wall Street, even to this day, is replete with lots of rules of thumb and sort of old wives’ tales and shorthands for how to do things. And some of these things, when I would sit there and listen to them and try to cobble it all together, just didn’t make sense.” – Michael Mauboussin

We believe that investors need a different approach to fundamental research, one that acknowledges that we cannot tell the future. Successful investing is more about managing uncertainties as well as understanding “skews” in outcomes and ranges of possible distributions of stock returns rather than black box valuation models which produce a single answer to a complex problem.

We infer what expectations are built into share prices by using our valuation framework. This process illustrates what needs to happen with a company’s key value drivers to justify where the share price is trading. Our fundamental research then concentrates on industry dynamics and developing an understanding of the likely scenarios of how that key value driver could evolve going forward.

Using private hospital operator Netcare as an example, the key value driver we identify for the stock is utilisation of its asset base, best tracked by paid patient days (PPDs). The stock price of Netcare is still trading at 25% below where it was trading prior to Covid while the JSE Shareholder Weighted Index (SWIX) is 15% above its pre-Covid levels.

Our reading of the expectations embedded in the share price is that PPDs need to continue falling into perpetuity to justify the current share price. In our view, the market has extrapolated the weakness in margins which Covid created as volumes and case mix deteriorated in what is essentially a fixed-cost business. However, volumes have been improving, despite a second dip as Omicron hit and we see continued declines as highly unlikely.

Avoiding the forecasting trap by looking for asymmetry in likely return outcomes, we look for “skews” in likely return distributions. Using our analysis framework with scenarios can help when faced with unforecastable variables. Understanding range of likely distributions has significantly more value that just a single price target.

Range of ROE outcomes vs price implied ROE

In addition to our differentiated approach to fundamental analysis we also believe in a strong process to help against behavioural biases where we screen to identify for strong earnings momentum and valuation to look for opportunities.

We use earnings momentum to build further conviction in our investment case. Valuation is obviously an important part of security analysis; however, as we have highlighted above it is susceptible to numerous sources of inaccuracy. We believe that a robust investment process is well served by an additional overlay to tilt the odds in our favour.

Business cycles tend to grow in strength, autocorrelation effect of forecast revisions provide more support for the investment through time as markets struggle to forecast the full impact of cycles on day one as market participants tend to only make changes in views in small incremental moves.

Our process uses a disciplined approach to screening to help us direct our research efforts to where likely opportunities are in the market, as opposed to working on stocks only when they report.

Our philosophy in embracing the uncertainty in markets is also echoed further by a view Duke shares in Thinking in Bets where she argues, “We are discouraged from saying ‘I don’t know’ or ‘I’m not sure’.

“We regard those expressions as vague, unhelpful and even evasive. But getting comfortable with ‘I’m not sure’ is a vital step to being a better decision-maker. We have to make peace with not knowing.”