Every quarter, the Schroders Economics team updates its in-house forecast for global growth.

The latest update shows global growth will slow from 2.8% in 2022 to 2.4% in 2023. The previous estimate was for growth to slow to 2%, so we’ve become more positive on the prospects for growth in 2023. This is mainly because the US economy is doing better than we anticipated.

But looking forward to 2024, we now think growth will slow even further than we did last time. Previously we forecast 2024 growth slowing to 2.2% but now we have that figure at 1.9%. This is largely because we think the US economy is going to hit recession towards the end of 2023.

US: recession delayed

Things have been going better than we expected in the US economy. A strong labour market means many people are employed so they can afford to spend, which in turn drives economic growth. And this has been stronger than we previously anticipated. We now think the US economy will expand at a rate of 1.5% in 2023.

However, interest rates have been rising and are currently 5.25%. Higher interest rates make it more expensive for people to borrow and as things like mortgages and other loans now attract bigger interest payments, people will have less money left over to spend in the economy. This will curtail spending and therefore economic growth. We think there will be such a decline in spending and growth that the US economy will start contracting and slip into a mild recession at the end of 2023.

But we think inflation is going to come down to such an extent that the Federal Reserve will be able to cut interest rates by 25bps before the end of the year, and lower them to 3.50% in 2024.This should help the US economy come out of recession but will leave GDP growth flat in 2024.

Europe: higher inflation than expected

Although energy prices have fallen further, relieving some pressure on inflation, higher food and services inflation means we think overall inflation is going to be higher than we previously anticipated. We now forecast it to average 5.6% in 2023 and 2.4% in 2024. As a result, the European Central Bank (ECB) is likely to raise interest rates to 4.25%.

While higher interest rates will weigh on economic growth, as we described above, the eurozone economy is performing better than we expected and so this will offset the drag from higher rates. As such, we forecast the economy to expand by 0.6% in 2023 and by 0.9% in 2024. And given our expectation that inflation will fall below 3% early next year, we think ECB will cut rates to 2.5% by the end of 2024.

UK: recession avoided, but vulnerabilities remain

The UK economy is now forecast to avoid a technical recession (when an economy contracts for two or more consecutive quarters), but we still think it’s going to stagnate for most of this year before improving to a 0.9% expansion in 2024.

Meanwhile, food price inflation has lasted longer than expected, so we think consumer price index (CPI) inflation will stay relatively high at an average of 7.6% in 2023 before easing to 3.6% in 2024. In response, the Bank of England (BoE) is likely to raise rates by a further 50bps this year, taking them to a peak of 5%. But as inflation falls back towards the 2% target in 2024, we expect the monetary policy committee will cut rates to 3.25% over the course of next year.

Emerging markets: China’s lopsided recovery set to fade

China’s economy has performed better than most people expected at the start of 2023. We think it will continue to deliver good growth late into the year.

By contrast, we anticipate that most other major emerging market (EM) economies are facing a period of slower growth as aggressive interest rate hikes over the past year take their toll on activity. So we forecast that EM growth will slow from 4.4% in 2023 to 3.9% in 2024.

Still, EM inflation has begun to ease and should fall sharply into year-end. This means central banks should start cutting rates, potentially in the second half of 2023, improving the outlook for growth in 2024.

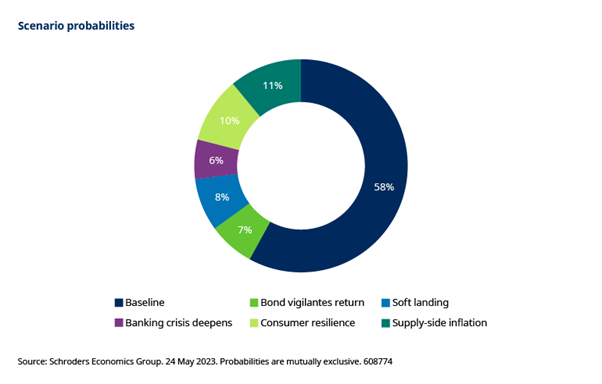

Risk scenarios to watch: banking crisis added

For some time, we have judged that stagflation (when inflation rises while growth slows) poses the greatest threat to the global economy. But recently the risks to both growth and inflation have become more balanced.

We have five scenarios that present a risk to our base case (we have described our base case above). The scenario most likely to play out is ‘supply-side inflation’. In this scenario, the labour market stays strong – which means that many people remain employed – which causes wage inflation to stay high, pushing up costs for companies who in turn hike their prices, contributing to greater inflation in the economy. This ‘stagflationary’ scenario requires even more aggressive interest rate rises to reverse inflation pressure.

The next most likely scenario is the ‘consumer resilience’ scenario. This scenario sees households spending more of their pandemic-induced savings which drives up inflation, and also has a positive effect on growth.

Then we have a scenario that anticipates a ‘soft landing’ for global growth. In other words, growth slows but not by a problematic amount, and workers return to the labour market. With greater supply of workers, wage inflation doesn’t stay as high as in the ‘supply-side inflation’, but economic productivity is boosted, which in turn supports better growth.

There are two scenarios which result in deflation (i.e. falling prices). The first is ‘bond vigilantes return’ in which bond buyers effectively ‘strike’ in various bond markets around the world and don’t buy any government bonds. This would cause huge volatility in global financial markets. Governments may be forced to retrench workers, and emerging markets that rely on capital flows would be negatively affected. Global growth would slow, although weaker demand would at least bring inflation down.

Our final scenario is called ‘banking crisis deepens’. This scenario has been added in response to the events at regional US banks in recent months. This scenario assumes more regional banks face bank runs and fail. As they do, the rest of the banking system stops lending and economic demand slows. This spreads to other countries and, we think, would result in the Fed cutting interest rates to stem the crisis.

The above risks to our base case could derail our forecasts so we’ll be monitoring them closely.

Important Information

For professional investors and advisers only. The material is not suitable for retail clients. We define “Professional Investors” as those who have the appropriate expertise and knowledge e.g. asset managers, distributors and financial intermediaries.

Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy.

Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of investments to fall as well as rise.

The views and opinions contained herein are those of the individuals to whom they are attributed and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy.

Issued in June 2023 by Schroders Investment Management Ltd registration number: 01893220 (Incorporated in England and Wales) which is authorised and regulated in the UK by the Financial Conduct Authority and an authorised financial services provider in South Africa FSP No: 48998