The 2025 Hedge Fund Guide aimed to provide foundational insights into hedge funds, from the basics of what a hedge fund is, to the history of hedge funds, the different types of hedge funds, how they are structured, regulated and how one should approach selecting a hedge fund.

This 2026 Hedge Fund Guide aims to deepen those insights by looking at investors’ lived experiences of hedge funds, be those flows, performance, fees, how a hedge fund can add value to a portfolio and how hedge funds offer behavioural benefits to investors. Hedge funds are becoming more popular, particularly for retail investors

According to annual statistics released by the Association of Investments and Savings (ASISA), the South African hedge fund industry has grown significantly, with total assets under management rising to R216-billion at the end of 2025 (excl Fund of Funds), representing a 17% increase from R185-billion at the end of 2024.

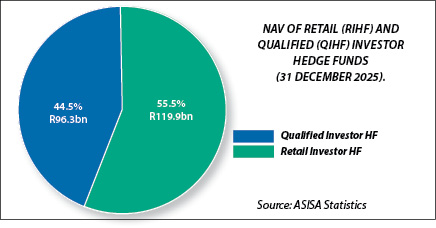

A key trend within this growth is that by the end of 2025, the South African Retail Investor Hedge Funds (RIHFs) officially became the larger segment of the South African market, surpassing the previously bigger segment, the South African Qualified Investor Hedge Funds (QIHFs).

According to ASISA statistics, 55.5% of hedge fund assets are now held in Retail Investor Hedge Funds (excluding Fund of Funds) at the end of December 2025 with a total AUM of R119.9-billion. The balance of the assets, R96.3-billion, is held in QIHFs, even though there are still slightly more QIHFs (111) than RIHFs (108) available to investors.

The shift in appetite between these two types of funds is demonstrated by the character of inflows in 2025, where Retail Investor Hedge Funds recorded R9.1-billion in net inflows, while Qualified Investor Hedge Funds had net outflows of R4.3-billion.

When hedge funds in South Africa were regulated in 2015, the distinction was made between SA Retail Investor Hedge Funds (RIHFs) and SA Qualified Investor Hedge Funds (QIHFs). QIHFs are structured in a way that harks back to the original target market of hedge funds: wealthier, more “sophisticated” investors who meet specific income or net worth requirements. Hence QIHFs require a minimum investment of R1-million in contrast to RIHFs which are accessible for a minimum lump sum of R50 000 and a monthly debit order investment of as little as R1 000 to R5 000. RIHFs are more tightly regulated than QIHFs, with stricter risk controls and daily liquidity requirements whereas QIHFs have less defined risk controls and may offer liquidity only on a quarterly basis.

Attempts to “democratise” hedge funds seem to be working

In introducing RIHFs, FSCA aimed to strike a balance between allowing the benefits of hedge fund strategies to be experienced through broader market participation but protecting the public with explicit limits on factors such as leverage and concentration. This approach has clearly worked, with the appetite for hedge funds among potentially less sophisticated investors growing.

Additionally, it appears that financial planners and discretionary fund managers are becoming more comfortable with recommending hedge funds as an investment vehicle to their clients, and particularly Retail Investor Hedge Funds with their stricter regulatory limits. FSCA intended for these funds to be aimed at clients who are familiar with long-only traditional unit trusts.

Qualified investors, on the other hand, not only need at least R1-million to invest in a hedge fund, but either they must have demonstrable knowledge and experience in financial and business matters which enables them to assess the merits and risks of a hedge fund investment, or they must have appointed a suitable FSP who has the knowledge and experience to advise them on the merits and risks of a hedge fund investment.

The opportunity that the shift in flows to retail funds presents for financial planners is that they can now, with confidence, include hedge funds in a client’s portfolio in the accumulation phase of the client’s financial journey, not just when they have a lump sum of money at retirement or another stage of their life when they already have accumulated wealth.

Financial planners can recommend RIHFs to their clients with the reassurance that the regulator has set these up with a “safety-first” architecture that includes very sound guardrails. The leverage limits for RIHFs mean that they are capped at 200% gross exposure (R2 exposure for every R1 of capital) whereas for qualified investors, the QIHFs can effectively set their own limits if they disclose them. Similarly, concentration limits mean an RIHF cannot hold more than 10% of its capital in a single entity ensuring that there is a minimum level of diversification of risk in the portfolio.

The historical risk (and criticism) of hedge funds, that they are “black-box” investments because the strategies and holdings are often so opaque, have been addressed with South Africa’s pioneering regulation. This has mitigated the risk that a single “bet” could sink a fund, as we have seen with some of the major blow-ups in traditional hedge funds globally, the Long-Term Capital Management (LTCM) collapse in 1998 being probably the highest profile of these.

LTCM was a hedge fund founded by Nobel laureates Myron Scholes and Robert Merton along with John Meriwether. They used opaque, complex mathematical models and high levels of leverage which led to the collapse of the fund during the Russian financial crisis in 1998. Investors in RIHFs in South Africa can be reassured that they are protected against this type of disaster. But the differences between RIHFs and QIHFs are not just limited to regulatory variances.

Geographical exposure differs depending on the type of hedge fund

The ASISA Hedge Fund Classification standard classifies hedge funds in four tiers. The first tier is the distinction between RIHFs and QIHFs, which is premised on the regulatory differences already discussed. The second tier of classification is according to where funds invest geographically. According to ASISA statistics, at the end of December 2025, there were distinct geographical distinctions between RIHFs and QIHFs.

Qualified Investor Hedge Funds had 81 funds (73%) invested in South African portfolios. This type of fund must invest at least 60% of their total exposure in South African investment markets. They may invest a maximum of 30% of their assets outside of South Africa plus an additional 10% of their assets in Africa excluding South Africa. Twenty-seven funds (24%) are classified as worldwide portfolios which invest in both South African and foreign markets. There are no limits set for either domestic or foreign assets. Global and regional portfolios (3%) make up the balance of geographical exposure.

Two funds are classified as global portfolios which invest at least 80% of the total exposure in assets outside South Africa, with no restriction to assets of a specific geographical country (eg the USA) or geographical region (eg Africa). One fund is classified as a regional portfolio, investing at least 80% of the total exposure in assets in a specific country or region outside South Africa. If one combines the worldwide and global portfolios, effectively one quarter of QIHFs have a material offshore allocation.

The number of RIHFs that have an offshore allocation is lower than the QIHFs with 86 funds (80%) classified as South African portfolios, 20 funds (18.5%) as worldwide portfolios, one fund as global and one fund as regional (1.5% combined).

These statistics suggest that as of December 2025, worldwide exposure is materially more prevalent in QIHFs (24%) versus RIHFs (18.5%), while 80% of Retail Investor Hedge Funds remain South African-focused compared with 74% of Qualified Investor Hedge Funds. This divergence in geographical exposure underscores the fact that the distinction between RIHFs and QIHFs is not just limited to their separate regulatory obligations.

In addition to the growing shift to retail hedge funds, another feature of the industry worth noting is the concentration of assets among a few hedge fund managers. According to HedgeNews Africa, at the end of 2025 the industry’s top five single-manager hedge fund companies in South Africa managed just under 60% of total South African single-manager assets while the top 10 managers accounted for just under 75% of total assets.

In terms of strategy, multi-strategy hedge funds attracted the strongest retail inflows, drawing R7.5-billion. This reflects a broader appetite for funds that can adapt to changing market conditions using a multi-pronged strategy, rather than relying on a single approach. Fixed-income hedge funds also attracted meaningful retail interest, with R3.3-billion in net inflows. Long-short equity funds, historically the dominant local strategy, experienced net outflows across both categories. It nevertheless remains the dominant strategy with respect to number of funds and total assets under management.

The availability of hedge funds on LISP platforms that previously housed long-only unit trust funds has helped with the broader distribution of retail hedge funds. Where financial planners and investors previously had to get direct access to hedge fund managers, they can now get access using the platforms which house their existing unit trusts.

The bottom line

In their effort to “democratise” hedge funds, FSCA has ensured that investors can have the comfort that a hedge fund need not be the clichéd “black-box” investment, but can be something more familiar and transparent, which means it can be used as an important element of a diversified portfolio which has the potential to reduce volatility and provide uncorrelated returns with traditional equity and bond markets.

* As published in the Blue Chip 2026 Hedge Fund guide.