When considering offshore investing, the starting point is not the fund – it’s the investor. What are you trying to achieve? Whether it’s long-term capital growth, funding future goals, or creating offshore diversification, the objective should guide the decision-making. Different needs require different solutions, and this should shape how a portfolio is built from the outset.

Once this objective is clear, the next challenge is navigating the offshore universe. The range of available funds is vast – over 143 858 regulated funds globally, according to the 2025 Investment Company Fact Book. While not all are accessible to South African investors, the number of options remains significant. The difficulty, therefore, is not finding funds but choosing the right ones.

That choice is not always straightforward. Selecting a fund requires more than looking at past performance. It involves understanding how a manager invests, how consistent their process is, and whether they are well-positioned to deliver over time. With so many options available, this can quickly become overwhelming.

Finding true diversification

But selecting individual funds is only part of the process. The next step is understanding how those funds work together in a portfolio. This is where diversification becomes important.

Diversification is not about holding more funds or simply choosing different managers. Portfolios can look well diversified on paper but still be exposed to the same underlying drivers. When that happens, they tend to behave in the same way – rising together and falling together.

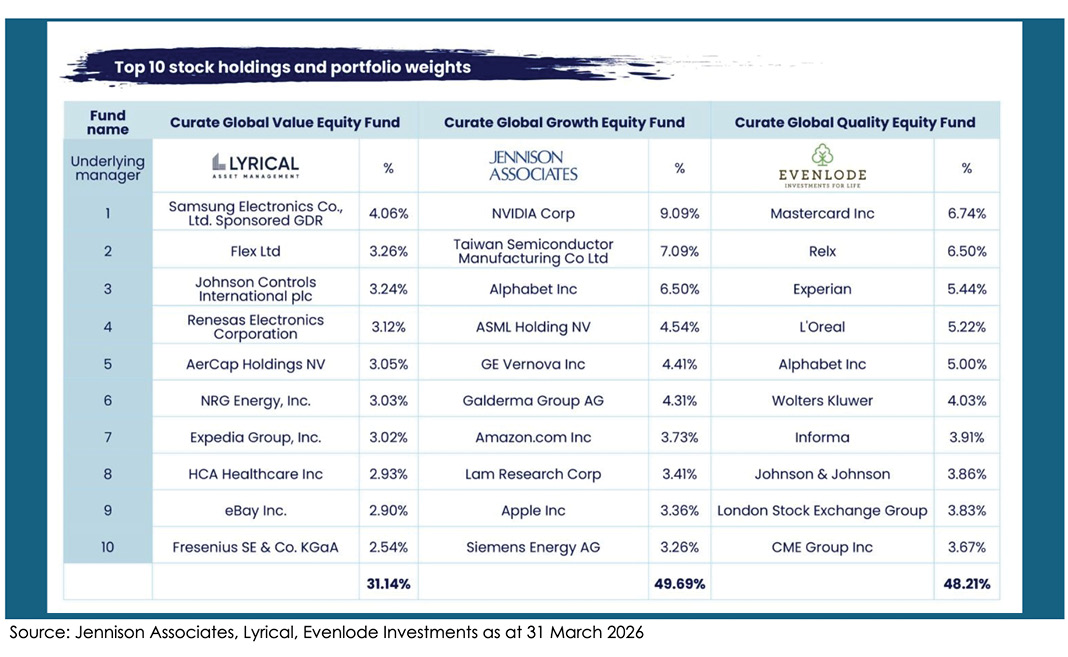

True diversification comes from combining different investment approaches. This is clearly illustrated by looking at Curate’s global equity managers – Lyrical Asset Management, Jennison Associates, and Evenlode Investment, for example. While our value (Lyrical), growth (Jennison), and quality (Evenlode) strategies all invest in the same global universe, their portfolios look fundamentally different, with minimal overlap in their top 10 holdings, as reflected in the table below.

This differentiation extends across the full portfolios. There are only five shared positions between the Curate Global Growth Equity Fund and the Curate Global Quality Equity Fund, with Nintendo Co Ltd the only stock common across all three strategies, highlighting how each manager is identifying opportunities in very different parts of the market.

These differences are driven by distinct investment approaches: Lyrical focuses on attractively valued companies that may be overlooked, Jennison targets businesses benefiting from long-term structural growth trends, while Evenlode prioritises high-quality companies with durable earnings. The result is exposure to different sectors, regions, and drivers of return, demonstrating how diversification works beneath the surface – not just across funds, but within the underlying investments themselves.

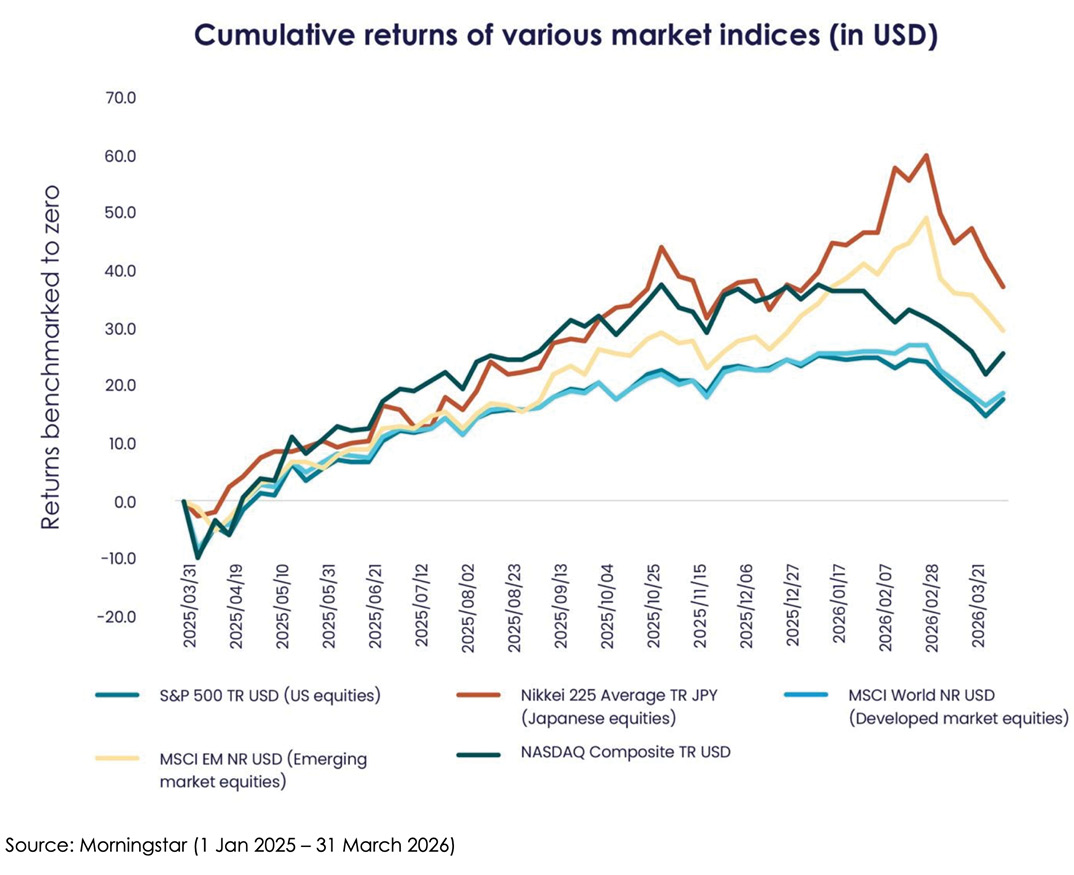

The same thinking applies at a regional level. Market leadership does not stay the same. While the U.S. dominated returns for a long period, more recently, there has been a shift, with other regions starting to perform more strongly, as illustrated below. This highlights the importance of not relying too heavily on a single market.

The question then becomes how to access these opportunities. Many global equity funds include some exposure to emerging markets, but this is often relatively small. As a result, investors may believe they have sufficient exposure when, in reality, it is not meaningful. Including a dedicated emerging market fund can help address this by providing access to different growth drivers, evolving economies, and sectors that are not always available in developed markets.

At the same time, diversifying beyond the U.S. does not mean excluding it. The U.S. remains a large and diverse market, and beyond the well-known companies, there are still many opportunities that are less crowded and more attractively valued. A balanced approach allows investors to benefit from a broader opportunity set while still capturing these opportunities.

A more considered approach to offshore investing

But bringing all these ideas together is not easy. With so many options available, the real challenge is not just selecting good funds, but ensuring they work well together in a portfolio. Without a clear framework, it is easy to end up with a collection of funds that do not deliver a balanced outcome.

This is where Curate Investments aims to add value. By doing the research upfront and filtering a broad universe into a focused set of specialist global managers, the complexity of fund selection is reduced. The emphasis is not on offering more choice, but on offering the right combination of ideas, ensuring that each strategy plays a clear and complementary role within a portfolio.

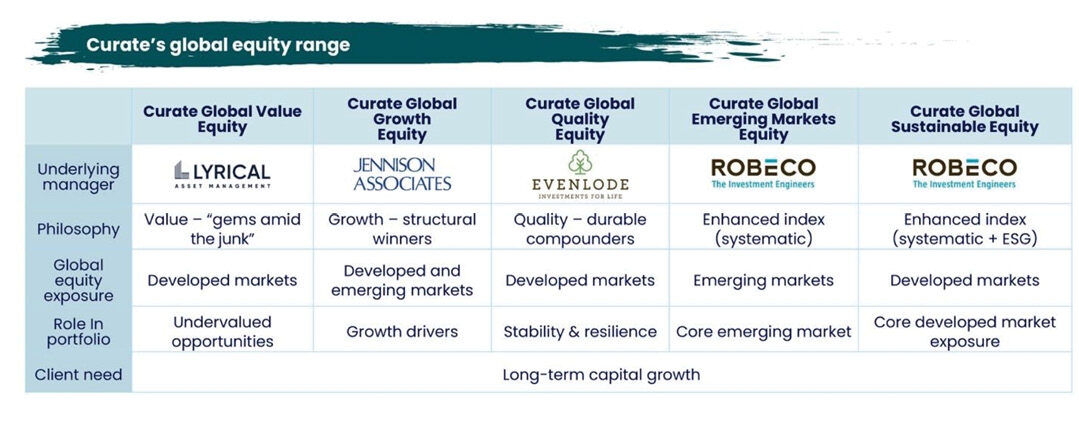

For investors seeking long-term capital growth, this is reflected in Curate’s global equity range. These strategies bring together different regions, styles, and approaches from enhanced index exposure through to high-conviction active managers, allowing for diversification at an underlying level rather than just across fund names. The result is a more considered approach to offshore investing – one that remains aligned to client needs, simplifies decision-making, and ensures diversification where it matters most.

For more information about Curate and our fund range, visit our website here: https://www.curateinvestments.com/sa/our-funds

![]()

Disclaimer

This document has been prepared by Curate Investments (Pty) Ltd (Curate). Curate is an authorised financial services provider (FSP No. 53549) under the Financial Advisory and Intermediary Services Act, 37 of 2002 (FAIS). This is a marketing communication. Collective investments are generally medium to long-term investments. The value of units may go down as well as up and past performance is not necessarily a guide to the future. Collective investments are traded at ruling prices. Commission and incentives may be paid and, if so, would be included in the overall costs. All performance is calculated on a total return basis, after deduction of all fees and commissions and in US dollar terms. Higher risk investments include, but are not limited to, investments in smaller companies, even in developed markets, investments in emerging markets or single country debt or equity funds and investments in high yield or non-investment grade debt. Foreign securities may have additional material risks, depending on the specific risks affecting that country, such as: potential constraints on liquidity and the repatriation of funds; macroeconomic risks; political risks; foreign exchange risks; tax risks; settlement risks; and potential limitations on the availability of market information. Investment in the Fund may not be suitable for all investors. Investors should obtain advice from their financial adviser before proceeding with an investment. This document should be read in conjunction with the prospectus of MGF, in which all the current fees additional disclosures, risk of investment and fund facts are disclosed. This document should not be construed as an investment advertisement, or investment advice or guidance or proposal or recommendation in any form whatsoever, whether relating to the Fund or its underlying investments. It is for information purposes only and has been prepared and is made available for the benefit of the investors. While all care has been taken by the Investment Manager in the preparation of the information contained in this document, neither the Manager nor Investment Manager make any representations or give any warranties as to the correctness, accuracy or completeness of the information, nor does either the Manager or Investment Manager assume liability or responsibility for any losses arising from errors or omissions in the information.

This Fund is a sub-fund of the MGF SICAV, which is domiciled in Luxembourg and regulated by the Commission de Surveillance du Secteur Financier. The Fund conforms to the requirements of the European UCITS Directive. FundRock Management Company S.A., incorporated in Luxembourg, is the Management Company with its registered office at 33, Rue de Gasperich, L-5826 Hesperange, Luxembourg. Telephone +352 271 111. JP Morgan Bank Luxembourg SA, incorporated in Luxembourg, is the Administrator and Depositary with its registered office at European Bank & Business Centre, 6, route de Trèves, L-2633 Senningerberg, Luxembourg. Telephone +352 462 6851.

This document is issued by Momentum Global Investment Management Limited (MGIM). MGIM is the Investment Manager, Promoter and Distributor for the MGF SICAV. MGIM is registered in England and Wales No. 03733094. Registered Office: The Rex Building, 62 Queen Street, London EC4R 1EB. Telephone +44 (0)20 7489 7223 Email DistributionServices@momentum.co.uk. MGIM is authorised and regulated by the Financial Conduct Authority No. 232357, and is exempt from the requirements of section 7(1) of the Financial Advisory and Intermediary Services Act 37 of 2002 (FAIS) in South Africa, in terms of the FSCA FAIS Notice 141 of 2021 (published 15 December 2021). Either MGIM or FundRock Management Company SA, the management company, may terminate arrangements for marketing under the denotification process in the new Cross-border Distribution Directive (Directive EU) 2019/1160.