A client’s income from a living annuity should be linked to his or her age. The Association for Savings and Investment South Africa (ASISA) has recommended income bands according to gender and age, but they are not always at hand and often difficult to remember.

At Glacier, our proven post-retirement approach draws on real client outcomes to help advisors guide better decisions and build retirement confidence.

A simple formula gives a client a projected escalating income into their mid-80s, assuming the following:

- A moderate risk portfolio (inflation plus 4%).

- Annual inflation adjustment on income.

- Platform and advice fee of 0.5% is included.

Average life expectancy for affluent clients is mid-80s (South African average is 63).

How the formula works

- Use the age of the youngest income receiver (if your calculation is for a couple).

- Change the age into a decimal (eg 65 becomes 6.5).

- Subtract a factor of one (1) and get an answer which becomes the starting income percentage, eg:

• Age 65 = 6.5 – 1 = 5.5%

• Age 52 = 5.2 – 1 = 4.2%

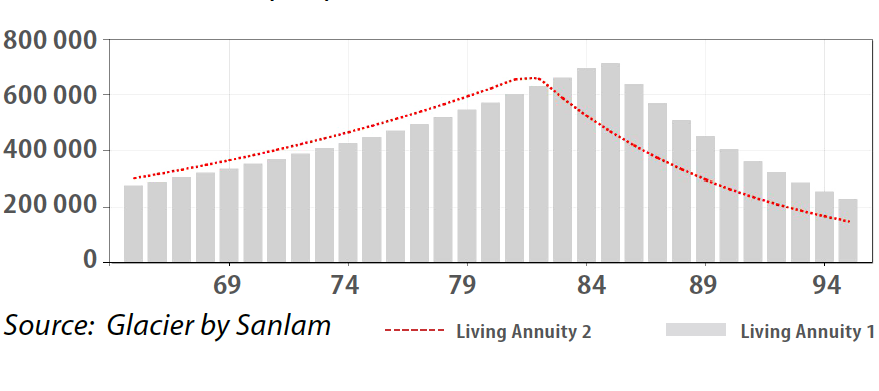

In the graph below, Client 1 sticks to the income determined by the formula (5.5%), compared to Client 2 who takes 0.5% more (6%). The grey bars show the projected income of Client 1, while the red line shows the income projection of Client 2. Observe where the income tarts to decrease rapidly for Client 1 and 2.

By sticking to the formula, a typical living annuity client increases his/her chances of having an escalating income to the average life expectancy age. A starting income with an extra 0.5% shortens this period with almost five years.

Should a guarantee be added in combination with a living annuity?

Although guaranteed rates have come down during the third quarter of 2024, it is imperative to determine whether it would still benefit a client to combine a guarantee with a living annuity.

The rule of thumb is that whenever the guaranteed rate is higher than the answer in the living annuity formula, it makes sense to include a guaranteed life annuity.

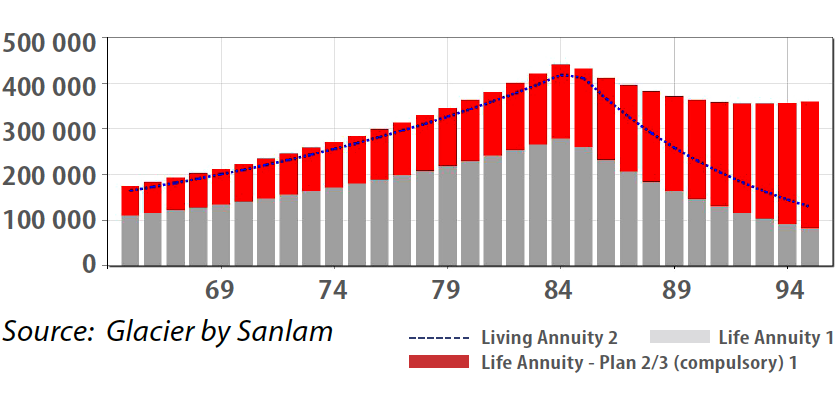

The graph below shows the same client, aged 65, using a living annuity income of 5.5% escalating at 5%, which is the assumed inflation illustrated by the blue line. This is compared to combination with one-third in a life annuity (red bars) and two-thirds in a living annuity (grey bars), also with a 5% inflationary adjustment.

Assumptions

- The guaranteed rate was 6.4% (it is a joint life with 20-year guaranteed period until week ending 20 September 2024).

- The annual income escalation in all cases is 5%.

Conclusion

Combining a guaranteed life annuity with a living annuity can help smooth out income in later years, especially when the living annuity reaches the maximum allowed drawdown of 17.5%. While this improves long‑term income certainty, it does mean giving up some flexibility compared to using a living annuity alone. Keeping part of the investment in a living annuity, even when guaranteed rates look attractive, gives clients important options.

Income can be increased to cover unexpected costs, such as medical expenses, which is not possible with a guaranteed product. The living annuity can also be converted into a life annuity later if rates improve. Any remaining capital may still be passed on to beneficiaries after the guaranteed period ends.

What should the split between the living and life annuity be?

Here are some helpful guidelines:

- If the client favours the stability of the life annuity and guarantees, place one third in the living annuity.

- If the client favours the flexibility of a living annuity, place two thirds in the living annuity.

- If a client wants the best of both worlds, split evenly.

All calculations are for illustrative purposes and should not be construed as advice. Glacier Financial Solutions (Pty) Ltd is a licensed financial services provider. Sanlam Life Insurance Ltd is a licensed life insurer, financial services and registered credit provider (NCRCP43).